.jpg)

While RBI will consider the impact of the US and/other developed markets’ policy changes, their rate decision is majorly influenced by domestic growth and inflation dynamics. Domestically, within the MPC, there is increasing divergence, with one more member wanting to change stance and cut rates. Prof. Varma who has consistently voted for rate cuts in the past, this time was joined by Dr. Goyal in voting for a rate cut.

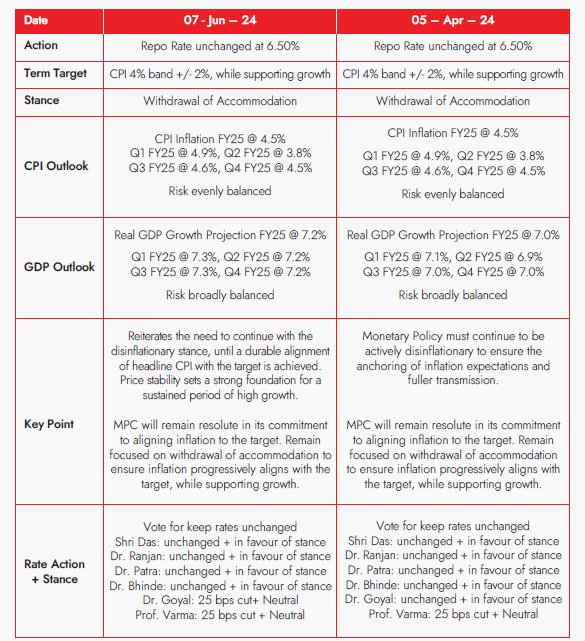

With one more pause this time, the MPC has continued with status-quo eight times in a row! Overall, RBI has nudged up the growth expectations for the year. The expectation of a normal monsoon is positive for agriculture and rural demand, while sustained momentum in manufacturing and services activity is likely to enable a revival in private consumption. Having said that, geopolitical tensions will be a factor to watch out for in global and consequently domestic growth. Inflation, while not spiking, continues to be an area of concern, with food inflation, volatility in crude prices, and firm non-energy commodity prices being speed bumps. Below is a brief snapshot of the policy for reference.

POLICY SNAPSHOT:

Source: RBI database

RBI GOVERNOR ON INFLATION:

Source: RBI database

CPI headline inflation softened further during March-April, though persisting food inflation pressures offset the gains of disinflation in core and deflation in the fuel groups. Despite some moderation, pulses and vegetables inflation remained firmly in double digits. Vegetable prices are experiencing a summer uptick following a shallow winter season correction. The deflationary trend in fuel was driven primarily by the LPG price cuts in early March. Core inflation softened for the 11th consecutive month since June 2023. Services inflation moderated to a historic low and goods inflation remained contained.

The exceptionally hot summer season and low reservoir levels may put stress on the summer crops of vegetables and fruits. The rabi arrivals of pulses and vegetables need to be carefully monitored. Global food prices have started inching up. Prices of industrial metals have registered double-digit growth in the current calendar year so far. These trends, if sustained, could accentuate the recent uptick in input cost conditions for firms.

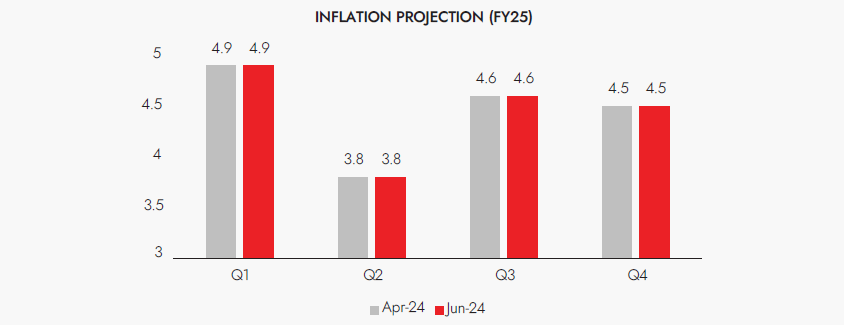

On the other hand, the forecast of above normal monsoon bodes well for the kharif season. Wheat procurement has surpassed last year’s level. The buffer stocks of wheat and rice are well above the norms. These developments could bring respite to food inflation pressures, particularly in cereals and pulses. The outlook on crude oil prices remains uncertain due to geo-political tensions. Assuming a normal monsoon, CPI inflation for 2024-25 is projected at 4.5 percent with Q1 at 4.9 percent; Q2 at 3.8 percent; Q3 at 4.6 percent; and Q4 at 4.5 percent. The risks are evenly balanced.

RBI GOVERNOR ON GROWTH:

Source: RBI database

National Statistical Office (NSO) placed India’s real gross domestic product (GDP) growth at 8.2 percent in 2023-24. During 2024-25 so far, domestic economic activity has maintained resilience. Manufacturing activity continues to gain ground on the back of strengthening domestic demand. The eight core industries posted healthy growth in April 2024. Purchasing managers’ index (PMI) in manufacturing continued to exhibit strength in May 2024 and is the highest globally. The services sector maintained buoyancy as evident from available high frequency indicators. PMI services stood strong at 60.2 in May 2024 indicating continued and robust expansion in activity.

Private consumption, the mainstay of aggregate demand, is recovering, with steady discretionary spending in urban areas. Revival in rural demand is getting a fillip from improving farm sector activity. Investment activity continues to gain traction, on the back of ongoing expansion in non-food bank credit. Merchandise exports expanded in April with improving global demand. Non-oil non-gold imports entered positive territory. Services exports and imports rebounded and posted a strong growth in April 2024.

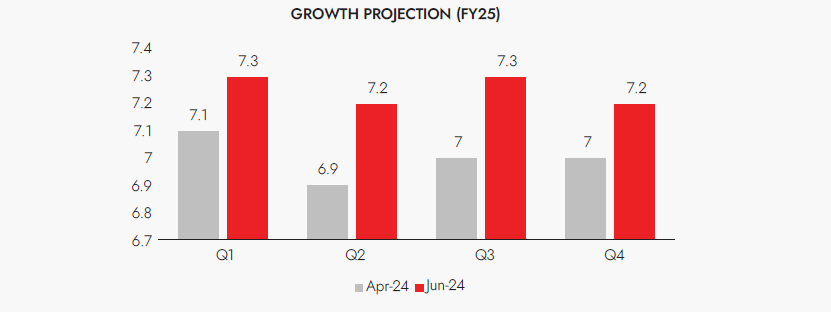

Looking ahead, the forecast of above normal southwest monsoon by the India Meteorological Department (IMD) is expected to boost kharif production and replenish the reservoir levels. Strengthening agricultural sector activity is expected to boost rural consumption. On the other hand, sustained buoyancy in service activity should continue to support urban consumption. The healthy balance sheets of banks and corporates; the government’s continued thrust on capex; high capacity utilisation; and business optimism augur well for investment activity. External demand should get a fillip from improving prospects of global trade. Taking all these factors into consideration, real GDP growth for 2024-25 is projected at 7.2 percent with Q1 at 7.3 percent; Q2 at 7.2 percent; Q3 at 7.3 percent; and Q4 at 7.2 percent. The risks are evenly balanced.

MARKET VIEW:

Readers will recollect our previous strategy note (link) wherein we highlighted the fact that ‘“Domestic cuts (policy action) will be driven by local macros’”. In this policy, the RBI governor has reiterated the same by saying, “I would like to unambiguously state that while we do keep a watch on whether clouds are building up or clearing out in the distant horizon, we play the game according to the local weather and pitch conditions. In other words, while we do consider the impact of monetary policy in advanced economies on Indian markets, our actions are primarily determined by domestic growth-inflation conditions and the outlook”.

Growth, while looking stronger, is prone to global and domestic vagaries. Having said that, one must take a much more nuanced view that growth has still not recovered from what was lost in COVID phase. So, while we might be growing and growing well, viewed from medium- term trajectory and where we should have been – ideally we should have been a bigger economy, growing more and rate action might be the additional boost for that. Though CPI is not at a four percent rate as desired by RBI, we are consistently within the tolerance band. However, with RBI having reiterated its inflation fighting focus, it will be looking for a clear glide path to four percent on a durable basis. The spike in food inflation, and consequent spillover to headline inflation, coupled with the behaviour of core components is what one has to be watchful of. Having said that expectations of normal monsoon and the government being proactive in alleviating pain if any with prompt supply side measures are positives in the food inflation equation.

Post elections, the continuation, and the mix of fiscal consolidation is what we will be looking at from the medium to long-term trajectory of the Indian market’s healthy and structural journey. While at an aggregate level, it has been fantastic, the continuation of the same is critical from an overall perspective to not wither away hard-fought gains. However, a few basis points of dilution in terms of higher revenue expenditure cannot be completely ruled out keeping in mind the various pulls and pushes the new dispensation might have to face.

From a global perspective, India's fixed-income market is very attractive in terms of its structural advantages, policy continuation, attractive inflation growth dynamics, and strong macros. While, USD 25 billion of bond index inflows might be the start, a higher inflow directly or indirectly will likely materialise over some time. Although the US markets offer attractive high yields, a strategic and disciplined asset allocation is crucial, particularly given that Indian bonds are underrepresented in global investment portfolios. Overall, the market has positive growth inflation dynamics locally, and coupled with favourable demand-supply dynamics on the market side, is likely to prevent any significant spike in interest rates on a sustained basis making the risk-reward equation attractive.

INVESTMENT OUTLOOK:

We run a dynamic strategy that takes advantage of the best opportunities across the maturity and rating curve.

In a currently non-directional market, with positive bias (fall in interest rates likely over some time), we are running a dynamic barbell strategy. Long duration positions as tactical investments to take advantage of fall in interest rates led to amplified capital gains on one side, along with well-researched, and well-covenanted high yield short maturity instruments to earn constant high carry on the other side, is our current strategy. The endeavour here is twin-pronged – stable earnings of high constant ability also capturinge capital appreciation. The focus is on building a stable portfolio that is well poised to capture the capital gains led by interest rate movement while earning constant high carry.

With all fixed -income products now getting the same taxation treatment, vis a vis certain vehicles enjoying favourable tax treatment earlier, leading to forced misallocation and/or mispricing of risk, investors now have an advantage of picking and choosing the most appropriate strategy/portfolio. This customisation will help investors earn additional alpha based on respective risk reward appetite more holistically and scientifically as compared to earlier tax arbitrage-biased investment decisions.

As always, we stay watchful of evolving situations, understand them fine-tune investment thesis, and resultant investment actions.

HAPPY INVESTING!

MALAY SHAH

Fund Manager, Fixed Income

Ambit Asset Management