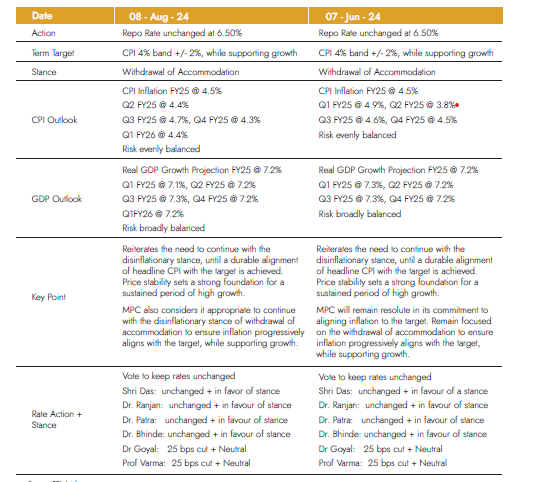

It’s an indicator of how tightly knit the markets are despite being on different/opposite trajectories. While the US has still not cut ECB, BOC and SWISS already have cut, and BOJ is hiking. RBI has however been handling various pulls and pushes well, and has come out on top, despite the heightened clamour for rate action from an increasing number of stakeholders.

Below is a brief snapshot of the policy for reference.

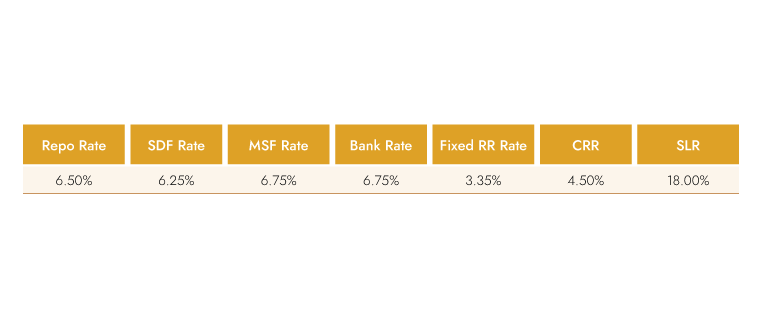

Benchmark Rates:

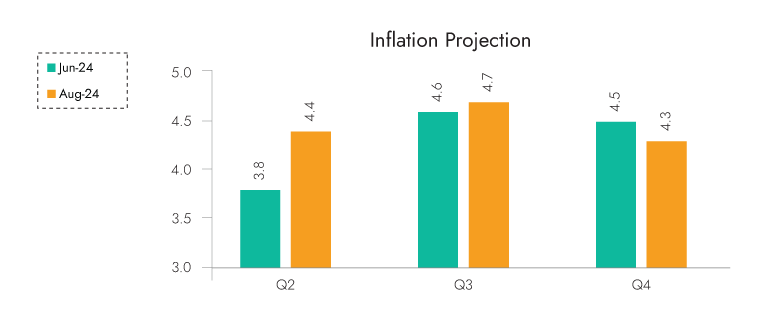

RBI Governor on inflation:

Source: RBI database

Headline CPI inflation edged up to 5.1 percent in June 2024 due to higher-than-expected food inflation. Fuel remained in deflation for the tenth consecutive month. Core inflation moderated to a historic low in May and June.

Food inflation, with a weight of around 46 percent in the CPI basket, contributed to more than 75 percent of headline inflation in May and June. Vegetable prices increased sharply and contributed about 35 percent to inflation in June. High inflation pressures persisted across other major food items also. On the other hand, the softening in core inflation continues to be broad-based, with core services inflation touching a new low in the current CPI series during May- June 2024.

The high food price momentum is likely to have continued in July. Large favourable base effects may, however, push headline inflation downwards in July. The impact of the revision in milk prices and mobile tariffs needs to be watched.

A degree of relief in food inflation is expected from the pick-up in the southwest monsoon and healthy progress in sowing. Buffer stocks of cereals continue to be above the norms. Global food prices showed signs of easing in July, after registering increases since March 2024. Assuming a normal monsoon, and taking into account the 4.9 percent inflation print in Q1, CPI inflation for 2024-25 is projected at 4.5 percent, with Q2 at 4.4 percent; Q3 at 4.7 percent; and Q4 at 4.3 percent. CPI inflation for Q1:2025-26 is projected at 4.4 percent. The risks are evenly balanced.

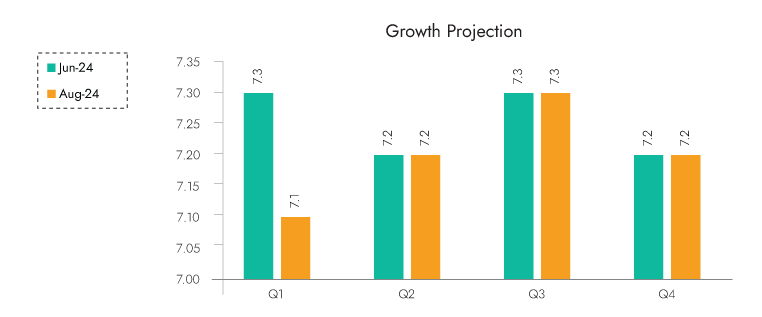

RBI governor on growth:

Source: RBI database

Domestic economic activity continues to be resilient. On the supply side, steady progress in southwest monsoon, higher cumulative kharif sowing, and improving reservoir levels9 augur well for the Kharif output. The likelihood of La Niña conditions developing during the second half of the monsoon season is likely to have a bearing on agricultural production in 2024-25

Manufacturing activity continues to gain ground on the back of improving domestic demand. The index of industrial production (IIP) growth accelerated in May 2024. Purchasing managers’ index (PMI) for manufacturing at 58.1 in July remained elevated. The services sector maintained buoyancy as evidenced by the available high-frequency indicators. PMI services stood strong at 60.3 in July 2024, and is above 60 for seven consecutive months, indicating robust expansion.

On the demand side, household consumption is supported by a turnaround in rural demand and steady discretionary spending in urban areas. Fixed investment activity remained buoyant, amid the government’s continued thrust on capex and other policy support. Private corporate investment is gaining steam on the back of expansion in bank credit. Merchandise exports expanded in June, although at a slower pace. Expansion in non-oil-non-gold imports accelerated reflecting resilience of domestic demand. Services exports recorded double-digit growth in May 2024 before moderating in June.

Looking ahead, improved agricultural activity brightens the prospects of rural consumption, while sustained buoyancy in services activity would support urban consumption. The healthy balance sheets of banks and corporates; thrust on capex by the government; and visible signs of pick up in private investment would drive fixed investment activity. Improving prospects of global trade are expected to aid external demand. The spillovers from protracted geopolitical tensions, volatility in international financial markets, and geoeconomic fragmentation, however, pose risks on the downside. Taking all these factors into consideration, real GDP growth for 2024-25 is projected at 7.2 percent, with Q1 at 7.1 percent; Q2 at 7.2 percent; Q3 at 7.3 percent; and Q4 at 7.2 percent. Real GDP growth for Q1:2025-26 is projected at 7.2 percent. The risks are evenly balanced. It may be seen that we have slightly moderated the growth projection for Q1 of the current year about the June 2024 projection. This is primarily due to updated information on certain high-frequency indicators which show lower than anticipated corporate profitability, general government expenditure, and core industries output.

Understanding:

Despite it seeming to be otherwise, RBI has made it clear that its actions are not solely a function of US FED. While RBI will consider the impact of US/other DMs policy change, their rate decision is majorly influenced by domestic growth and inflation dynamics, with inflation consideration taking priority currently.

Rural demand is likely to improve based on normal monsoon expectations and good kharif sowing. Coupled with a revival in private consumption based on momentum in manufacturing and services activity, overall growth looks to be stable domestically. However global geopolitical tensions, volatile energy prices, and US economy recession fears led global slowdown would act as headwinds. Food inflation in addition to increasing (from 36% in May 2023 to 76% in June 2024 is the share of food inflation to overall CP) is stubborn. With 46% weightage in the inflation basket, it calls for a watchful vigil. The core is softening, but food inflation spilling over to generalised inflation is a risk that RBI cannot afford to take. So while we are consistently within the tolerance band of inflation, RBI is preferring to watch for a durable and high conviction view on it being sustainably lower than the 4% target.

Additionally, eventually RBI will not want to go against the global direction of rate action. It will likely delay the cut at the most till US action and not further. Staying hawkish in a global dovish environment could create INR carry trade pressures, which RBI wouldn’t want to counter.

RBI didn’t hike a lot earlier, which is now showcasing the fantastic steering in troubled times. For comparison, RBI hiked by only 250 bps versus 525 bps hikes by the US. Thus for RBI achieving long-term neutral rates will be easier and sooner with less quantum of rate cuts as compared to the US. The advantage of this is minimal/zero chances of being “behind the rate curve”. This strengthens RBI’s flexibility of not being under undue pressure of cutting rates to support growth without inflation firmly under control. “Hand not being forced” is a strength that RBI is enjoying and overall augurs well despite murmurs from the rate cut needed section of investors. The elongated pause phase aids stability and prevents whipsaw movement either way. This makes risk-reward equation even more attractive from an overall perspective.

Investment Outlook:

The run-up to this policy has been internationally quite volatile. The likelihood of a recession has increased in the US, having a ripple effect globally. Weak job reports and resulting takeaways have increased the shrillness for immediate/off-market rate cuts in the US. The likelihood of a slowdown in the US has further gained weight due to Sahm Rule which many consider as a recession indicator. According to the Sahm Rule, the early stages of a recession are signaled when the three-month moving average of the U.S. unemployment rate is 0.50% or more above the lowest three-month moving average unemployment rate over the previous 12 months. The Sahm Rule has been widely recognized for its accuracy, simplicity, and ability to quickly reflect the onset of a recession. With US interest rates being on the higher end of their long-term neutral rates, cuts will have to be sooner / quantum of cuts will have to be higher. This increased the volatility further. As mentioned earlier, BoJ hiking rates to around 0.25% from 0 to 0.1% band sent the market into a tailspin, and in fact, BoJ had to step in with assurances of going slow with further hikes. Globally markets are pulling in different directions.

Amidst all this, India shines as a sweet spot. Readers would recollect our earlier discourse that from a global perspective, the Indian fixed income market is very attractive in terms of its structural advantages of a very favourable demand-supply equation for gsec and by second order effect on overall fixed income instruments. So while US markets, with their absolute high yield, remain attractive, a sensible spread of allocation will entail the flow of money to India over some time, especially with the fact that Indian bonds are under-owned by global allocation patterns. Stabilizing inflation, good growth, the cumulative impact of past reforms, the surge in digitalisation, good demographics, and continued fiscal discipline are among various factors that aid in its attractiveness. Coupled this with massive infrastructure spending and its multiplier long-term effects, portend good tidings. Currently, we think that inflation and RBI will likely undershoot RBI’s projection for the year, with our projections being sub-7 % for growth and sub-4.15 % for inflation.

We run a dynamic strategy with an aim to generate steady-state nonl-umpy returns. This is done by making a which takes advantage of the best opportunities across the maturity and rating curve.

We have a positive view of markets in terms of a fall in interest rates likely over some time. Basis that we run elongated duration in our portfolios, with a dynamic barbell strategy. Long duration positions as tactical investments to take advantage of fall in interest rates led to amplified capital gains on one side, along with well-researched and well covenanted high yield short maturity instruments to earn constant high carry on the other side is our current strategy. This generates stable returns of high constant carry with the ability to capture capital appreciation. The focus is on building a stable portfolio that is well poised to capture the capital gains led by interest rate movement while earning constant high carry.

With all fixed-income products now getting the same taxation treatment, vis a vis certain vehicles enjoying favourable tax treatment earlier, leading to forced misallocation and/or mispricing of risk, investors now have an advantage of picking and choosing the most appropriate strategy/portfolio. This customisation will help investors earn additional alpha based on respective risk reward appetite in a more holistic and scientific manner as compared to earlier tax arbitrage-biased investment decisions.

As always, we stay watchful of evolving situations, understand them fine fine-tune investment thesis and resultant investment actions.