.png)

However, there is enough dry powder in terms of time of cut, since currently RBI is optimistic about growth and there are no hard or soft landing fears immediately domestically. Everyone loves flexibility for higher optimisation, and kudos to RBI for their steering the policy through the years in such a way that they have space, flexibility, and choice rather than being forced into “action” for optimising their actions. Readers can refer to our previous outlook notes here, where we were positive in our investment actions and overall rate action. However, we had opined that there are no rate cuts likely immediately in the October policy and RBI would prefer to wait and watch. So while there has not been cut, the stance has been changed from “withdrawal of accommodation” to “neutral”.

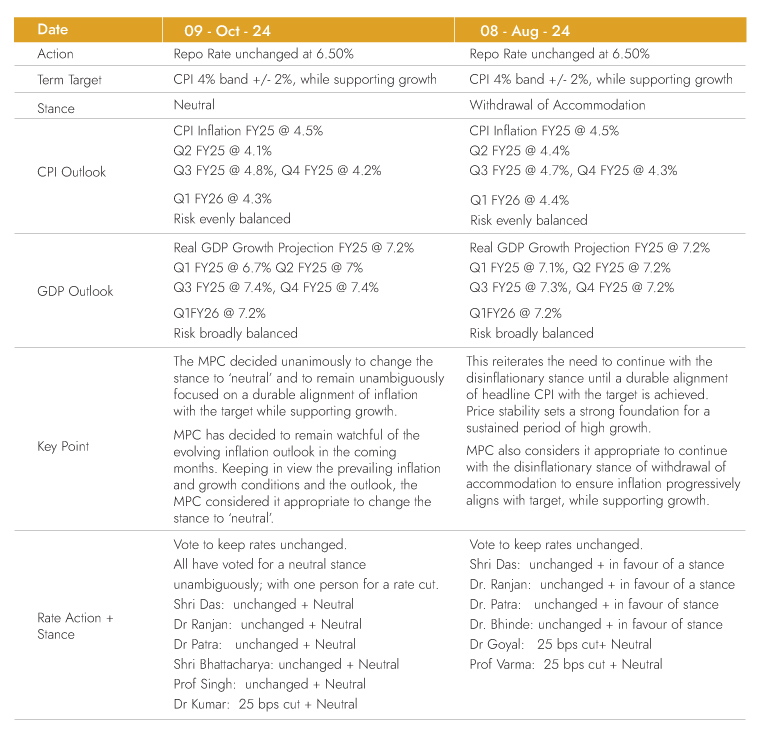

Below is a brief snapshot of the policy for reference.

Policy Snapshot:

RBI governor on inflation:

Source: RBI database

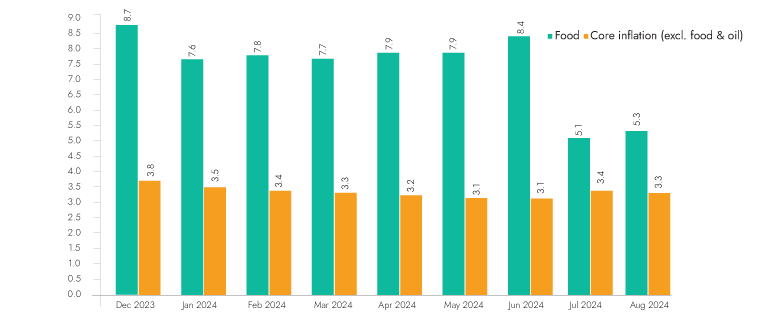

Headline CPI inflation softened significantly in July and August 29, with base effect playing a major role in July. Food inflation experienced a certain degree of correction during these two months. Considerable divergence, however, was observed within the food sub-groups. Deflation in the fuel group deepened on softening electricity and LPG prices. Core inflation, on the other hand, edged up in July and August.

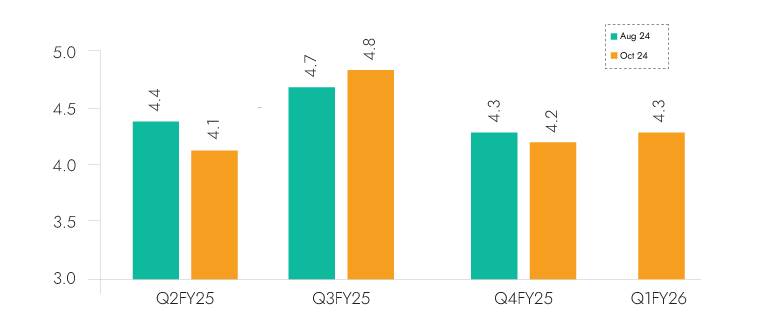

The CPI print for September is expected to see a big jump due to unfavourable base effects and a pick-up in food price momentum, caused by the lingering effects of a shortfall in the production of onion, potato, and chana dal (gram) in 2023-24, among other factors. The headline inflation trajectory, however, is projected to sequentially moderate in Q4 of this year due to a good Kharif harvest, ample buffer stocks of cereals, and a likely good crop in the ensuing rabi season. Unexpected weather events and the worsening of geopolitical conflicts constitute major upside risks to inflation. International crude oil prices have become volatile in October. The recent uptick in food and metal prices, as seen in the Food and Agricultural Organisation (FAO) and the World Bank price indices for September, if sustained, can add to the upside risks. Taking into account all these factors, CPI inflation for 2024-25 is projected at 4.5 percent, with Q2 at 4.1 percent; Q3 at 4.8 percent; and Q4 at 4.2 percent. CPI inflation for Q1:2025-26 is projected at 4.3 percent. The risks are evenly balanced.

RBI governor on growth:

Source: RBI database

Real gross domestic product (GDP) grew by 6.7 percent in Q1 2024-25, led by a revival in private consumption and improvement in investment. The share of investment in GDP reached its highest since 2012-13. Government expenditure, on the other hand, contracted during the quarter. On the supply side, gross value added (GVA) expanded by 6.8 percent surpassing GDP growth, aided by strong industrial and services sector activities.

High-frequency indicators available so far suggest that domestic economic activity continues to be steady. The main components from the supply side – agriculture, manufacturing, and services – remain resilient. Agricultural growth has been supported by above-normal southwest monsoon rainfall and better kharif sowing. Higher reservoir levels with good moisture conditions of soil augur well for the ensuing rabi crop. Manufacturing activity is gaining on the back of improving domestic demand, lower input costs, and a supportive policy environment. Eight core industries' output fell by 1.8 percent in August on a high base. Excess rainfall also dampened production in certain sectors such as electricity, coal, and cement in August. The purchasing managers’ index (PMI) for manufacturing at 56.5 for September remained elevated. The services sector continues to grow at a strong pace. PMI services at 57.7 in September indicate robust expansion.

On the demand side, rural demand is trending upwards while urban demand continues to hold firm. Government consumption is improving. Investment activity remains buoyant, with government capex rebounding from a contraction observed in the first quarter. Private investment continues to gain steam on the back of expansion in non-food bank credit, higher capacity utilisation, and rising investment intentions. On the external front, services exports are supporting overall growth.

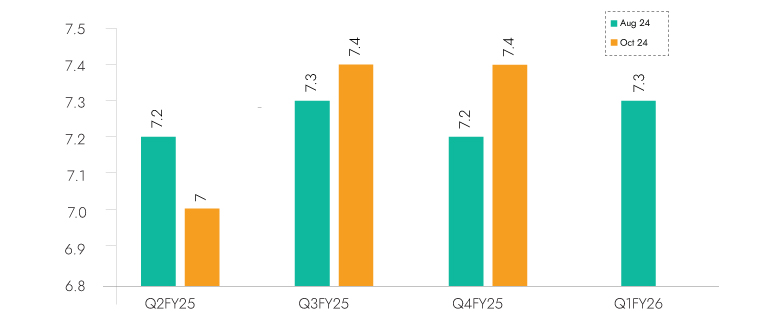

Looking ahead, India’s growth story remains intact as its fundamental drivers – consumption and investment demand – are gaining momentum. Prospects of private consumption, the mainstay of aggregate demand, look bright on the back of improved agricultural outlook and rural demand. Sustained buoyancy in services would also support urban demand. Government expenditures of the center and the states are expected to pick up pace in line with the Budget Estimates. Investment activity would benefit from consumer and business optimism, the government’s continued thrust on capex, and healthy balance sheets of banks and corporates. Taking all these factors into consideration, real GDP growth for 2024-25 is projected at 7.2 percent, with Q2 at 7.0 percent; Q3 at 7.4 percent; and Q4 at 7.4 percent. Real GDP growth for Q1:2025-26 is projected at 7.3 percent. The risks are evenly balanced.

Understanding:

Flexible Inflation Targeting introduced a little less than a decade ago has proved to be wonderful in terms of enabling adequate flexibility for authorities to fine-tune the policies without fear of counterproductive pressure on both sides of the inflation control and growth support equation.

A unanimous decision to change the stance indicates increasing MPC’A unanimous decision to change the stance indicates increasing MPC’s confidence in the future inflation trajectory and staying on a sustained basis in the comfort band. It has handled the high inflation “elephant” and now is confident that the controlled inflation “horse” will remain bolted in the stable ie within the tolerance band. We expect the next couple of prints to be higher, but that is likely to be the last higher prints. For more than a year, RBIs own estimates of 1 year forward core CPI and CPI ex-vegetable inflation have been below 4% for the last 9 month.

Exhibit 1: CPI and Core (ex food and fuel)

Source: CEIC, Ambit Asset Management

However, currently ongoing geopolitical tensions led to pressure on commodity prices is what RBI will want to keep an eye on. In case the firmness in prices persists then the rate cut could be delayed further. Baring that/domestic food prices witnessing disinflation, then RBI likely could start the rate cut cycle in December itself.

Also, investors should keep in mind that while growth momentum is strong, high-frequency indicators are suggesting weakness. Thus economy is growing, but there is some softness propping up viz weakness in PMIs, GST collection amongst others, and this weakness RBI would not want to let get entrenched.

Investment Outlook:

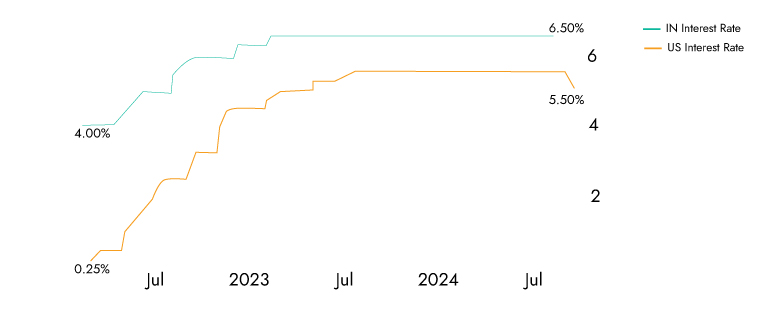

The run-up to this policy, while internationally being volatile – from April onwards USA benchmark 10-year yields have gone from 4.3 to 3.6 and back up to 4.1), domestically scenario has been quite positive. Indian 10-year is down to 6.80 from 7.05 for the same period.

Exhibit 2: Policy rates

Exhibit 3: Benchmark 10 years rates

1728651172075.jpg)

Source: tradingeconomics.com

Favourable domestic macros, increasing international bond indices inclusion, and a skewed demand-supply equation for bonds, augur very well from an overall perspective. So in addition to the rate cut journey fixed income is now also about more sets of international buyers emerging leading to sustained structural demand. After JP Morgan and Bloomberg, FTSE Russell was the third global index to include Indian bonds in its basket with flows starting 2025 onwards. It is precisely for this we have been saying that, since the direction is clear, investors should not worry about the precision of timing.

Currently, we are of the opinion that inflation and RBI will likely undershoot RBI’s projection for the year, with our projections being sub-7 % for growth and sub-4.5 % for inflation. Add to it favourable demand dynamics overall, basis that we are running elongated duration in our portfolios, with a dynamic barbell strategy. Long duration positions as tactical investments to take advantage of fall in interest rates led to amplified capital gains on one side, along with well-researched and well covenanted high yield short maturity instruments to earn constant high carry on the other side is our current strategy. This generates stable returns of high constant carry with the ability to capture capital appreciation. The focus is on dynamically building a stable all-season portfolio while minimising risks and optimally maximising returns. A point to note here is that, while the rate cycle will bring gains, currently we expect a shallow cycle of approximately 50-100 bps of cuts. RBI didn’t hike much unlike the 500 bps hike by the US, and RBI won't cut much. Currently, we expect a terminal rate to be 6.00-5.75 going ahead. Basis this we prefer duration as a tactical opportunity and we accordingly are poisoned.

With all fixed-income products now getting the same taxation treatment, vis a vis certain vehicles enjoying favourable tax treatment earlier, leading to forced misallocation and/or mispricing of risk, investors now have an advantage of picking and choosing the most appropriate strategy/portfolio. This customisation will help investors earn additional alpha based on respective risk reward appetite in a more holistic and scientific manner as compared to earlier tax arbitrage-biased investment decisions.

As always, we manage our investments dynamically, stay watchful of evolving situations, evaluate them, and fine-tune investment thesis and resultant investment actions.