Dear Patron,

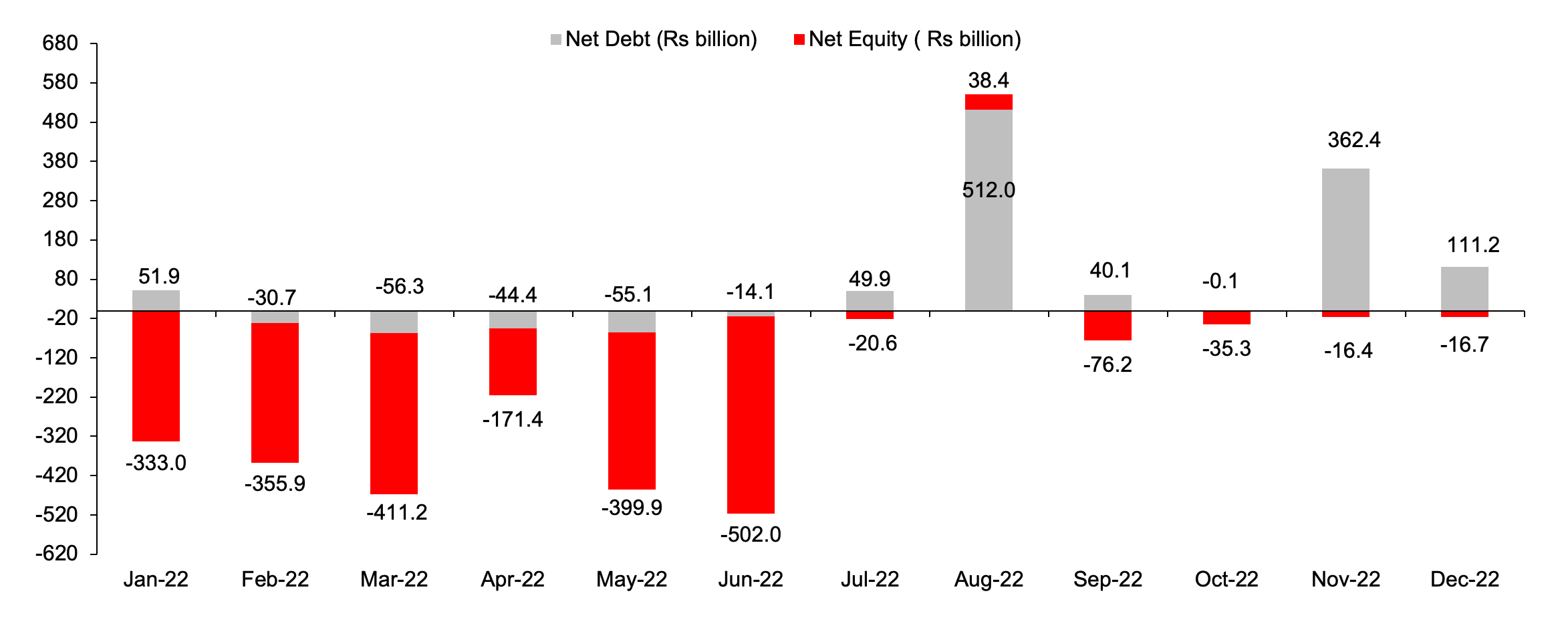

With each passing day, global economy is in a higher risk of sliding into a recession. The ongoing war has disrupted the supply chains, which were already reeling from covid disruptions. Record high inflation globally is resulting in lower spending power of customers. To combat inflation, central banks are tightening rates, at a time when demand is weak. While the global economy is struggling, with the on-going war, record high inflation and tepid demand, India’s economic indicators are showing no signs of weakness. CPI inflation eased to 6.7% YoY in July and is expected to further ease in the coming months as food inflation softens. Most of the sectors have bounced back and the demand outlook continues to remain robust. This has resulted in the trend reversal – FIIs have become net buyers in July after 9 months of continued outflow of Rs2.5 lakh cr. The trend continued in August as well with FIIs investing ~Rs50,000Cr for the month. In our June newsletter, we had highlighted that the market correction should be taken as a good entry point. Since then, Nifty 50/ Nifty Micdap 100 index are up 7/11%.

Q1FY23: Strong Recovery across sectors

Consumption engine firing on all cylinders: Q1FY23 was the first completely normalised quarter since covid disruptions. Consumer companies in the discretionary space delivered robust revenue growth. Metro/Tier1 focused companies operating in the mid-premium/premium segment have performed well due to better pricing power ability. FMCG companies delivered decent revenue growth, which was largely led by price hikes. Credit growth picked up materially to 14%yoy in June, with Pvt Banks leading the pack. This was coupled with declining non-performing and restructured assets.

Headwinds in export heavy sectors: CC Revenue growth of IT companies was largely in-line with expectations but reported performance was dragged by cross currency headwinds. Tier-1 IT companies reported multi-year low margins owing to supply side challenges, wage hike and return of discretionary spend. Similar trend was visible in Pharma companies where Raw Material inflation, high power and freight cost and normalized discretionary spend led to median EBITDA Margin contraction of ~350bps YoY.

Exhibit1: All our portfolios performed better than the indices across parameters

Source: Company, Ambit Asset Management

We will discuss the performance of different sectors during the last quarter

1. FMCG

Volume growth was a mixed bag across companies – on one hand while Nestle/Dabur reported 7%/10% volume growth on 3 yrs CAGR, on the other hand Marico/Uniliver reported 0%/2% on similar 3CAGR. Therefore revenue growth was largely led by price hikes. As covid led market restrictions are behind, most of the companies are looking to ramp up their new product launch pipeline and increase advertisement spends.

Nestle - Consistent delivery; forays into new categories

Nestle’s 2QCY22 revenue grew by 16% yoy and ~10% on 3 yrs CAGR. Growth was led by 6.4% YoY volume growth (~6% CAGR on 3 yrs. basis vs 2% for HUL). Foray into pet care business (Purina brand) and introduction of Gerber brand from global portfolio reflects Nestle’s quest to tap into parent’s portfolio. Going ahead, distribution expansion and portfolio diversification will aid Nestle in maintaining ~10-11% revenue growth.

ITC - Well-rounded quarter

Overall, ITC delivered a good performance across segments (1) Cigarette revenues grew 29% YoY led by 25% volume growth and EBIT grew 30% yoy (3-yr CAGR of 2.9%), (2) FMCG business grew 20% YoY partly aided by bounce back of stationery segment. EBIT margin at 4.6% was down 10 bps yoy owing to inflationary pressure, (3) Hotels and Paperboards recorded all-time high EBIT.

Across companies, outlook on demand recovery from rural markets was not very encouraging but managements remain hopeful that with better monsoon and government initiatives, 2HFY23 should be better for rural economy than 1HFY23. Also with moderation in RM prices, outlook on sequential gross margin expansion remain intact.

2. Consumer Discretionary

Strong comeback – Companies across categories have delivered strong results despite steep price hikes. Titan delivered strong performance due to pent-up demand (last quarter was marred by Omicron) and strong wedding season. Metro and Page delivered lifetime high revenues and profit. Safari not only delivered good growth after two consecutive washout during peak season, but also posted significant margin expansion due to operating leverage. PVR also delivered a robust performance due to strong content and absence of any covid-restrictions.

Demand for paints continues to remain resilient on the back of booming housing sector. Tier-1/2 cities continued to outperform Tier-3/4 cities with increasing share of premium range (premiumization). Economy segment also performed well (downtrading post 24% price hike) while the mid-premium segment contracted. Asian paints’ B2B business (contributes 15-20%) has grown significantly faster than B2C.

Exhibit: 2 Strong Revenue Growth across categories

Source: Company, Ambit Asset Management

Few Setbacks – Low consumer involvement categories such as fans/slippers suffered during the quarter as customers migrated to unorganised players for cheaper alternatives. Both Orient and Relaxo had taken large price hikes which led to decline in volumes. Demand continues to remain weak and management expects it to pick up in H2FY23.

We believe that FY23 will be the best year for most consumer discretionary companies. Orient and Relaxo are also expected to recover in the coming quarters. PVR is expected to deliver weak quarter due to lack of good content. However, we are bullish on the franchise as the strong merged entity will be in a formidable position to decimate the struggling competitors (both organised and unorganised).

3. Automobiles

Overall 2W volumes during FY22 rose by 54% YoY on Covid impacted base of last fiscal. Bajaj Auto lost market share to Hero Moto, HMSI, Yamaha and RE mainly owing to supply chain challenges. TVS’ market share was steady at ~15% QoQ.

Exhibit: 3 TVS market share has been steady amid Bajaj Auto losing M.S. to other 2W OEMs

Source: SIAM, Ambit Asset Management

Amidst the inflationary environment, TVS/RE/HMCL maintained steady margin QoQ, while Bajaj Auto declined 60bps QoQ. TVS is looking to raise Rs50bn for its EV subsidiary (similar to Tata Motors) which would help it unlock value.

Exhibit: 4 TVS continues to outperformed peers on all parameters

|

1QFY23 (YOY%) |

TVS Motors |

Bajaj Auto |

HMCL |

|

Volume |

38% |

-7% |

36% |

|

Revenue |

53% |

8% |

53% |

|

EBITDA |

119% |

16% |

83% |

|

PAT |

318% |

11% |

71% |

Source: Company, Ambit Asset Management

Domestic PV market share: Industry volumes rose by 40% YoY in Q1FY23 owing to easing supply constraints and on Covid impacted base of last fiscal. Maruti Suzuki lost 200bps QoQ in Q1FY23 to 41% whereas Tata Motors gained 200bps to 14%.

Exhibit: 5 Maruti has been losing market share while Tata Motors continues to outperform

Source: SIAM, Ambit Asset Management * Ford has exited the domestic market and hence the data is not available in 1Q

4. Banking

A. Advance and deposit growth:

- Loan growth further improved sequentially, largely led by retail loans. Within retail, credit card & PL continue to drive higher growth.

- While PSU banks grew at 15.6% yoy, Private banks grew at 19%. Housing finance companies continue showing healthy signs of AUM & disbursement growth.

- Deposits growth lagged advance growth by a wide margin. If this trend continues, banks will need to borrow, which may further deteriorate their margin profile.

Exhibit: 6 Loan growth far outpaced deposit growth

Source: RBI, Ambit Asset Management

B. Operating Performance and Profitability:

- Operating performance was weak due to treasury losses & higher opex leading to -9%YoY decline in operating profit for the sector. Opex was elevated for most of the banks, mainly on account of higher loan disbursement QoQ & higher spending on digital & branch expansion.

- Loans have been repriced & the impact shall be visible from Q2FY23 onwards on account of rise in external benchmarks i.e. Repo rate. Overall bank NIMs are stable to rising.

- Banking sector reported PAT of Rs 44,145cr up 37.2% YoY & down -9.5% QoQ driven by lower credit cost.

Exhibit: 7 Banks reported strong profit on the back of stable NIM and lower credit cost

Source: Company, Ambit Asset Management

C. Asset Quality:

- Asset quality continued to improve, but slippages grew by 7.3% QoQ on account of RBI’s strict daily NPA tagging & higher agri slippages seasonally.

- Recoveries, however, were higher leading to Gross NPA declining by -24bps QoQ to 5.94%. After 27 quarters, Net NPA ratio of PSU banks was <2%. Total restructured advances for the sector stands at 2% vs. 2.2% in Q4FY22.

Exhibit: 8 Banking system is operating with much lower stressed assets

Source: Company, Ambit Asset Management

5. Information Technology

Mixed revenue trends across companies: Overall revenue growth performance was strong in Constant Currency terms, but was impacted by strong cross-currency headwinds, especially Euro/USD. Reported performance vis-à-vis consensus expectation varied across companies. Companies with high exposure to geography such as Europe or verticals like Mortgage BPO / Capital Markets (Mphasis), Retail (Mindtree) or UK Government (Mastek) saw higher headwinds.

Contrasting margin performance between Tier1 and 2: 90-240bps/240-410bps QoQ/YoY EBIT Margin decline for Tier-1 was due to (1) Return of discretionary spend (2) Increased subcontracting cost (3) High attrition and supply challenges. Tier-2 Margin was relatively better in comparison.

Key Management commentary: (1) Healthy demand environment in the near term with good deal pipeline (2) Challenging but manageable macro environment; Sharper impact in Europe than US (3) Resilience of Tech spending to macro headwinds making it the last to be cut given mission critical nature in driving outcomes. Macro environment is challenging but navigable. (4) No challenge or change to CY22 client budget.

We expect companies to witness some impact of macro headwinds in H2FY23/H1FY24 beyond which we expect convergence with long term growth rates. Expect attrition to ease from H2FY23 with any near term demand blip further helping ease supply pressures (attrition).

Exhibit: 9 Attrition for IT companies at its peak, but the pace is reducing

Source: Company, Ambit Asset Management

6. Building Material

- In last quarter, Kajaria ceramics outperformed with flat PAT QoQ despite Q4 being strongest quarter as companies managed to maintain margins despite cost pressure.

- Plastic pipes segment reported 40 QoQ drop in EBITDA/PAT impacted by de stocking and inventory losses (PVC prices declined from Rs120 to Rs90). The impact was lower for Astral, owing to higher CPVC contribution.

- However we expect growth to continue as PVC prices normalise. We have seen in the past that channel restocking take place once prices normalise. The overall growth story remains intact with the category being significantly under penetrated.

- All companies logged working capital improvement (apart from slight increase in inventory) and are doing large capex led by strong cash generation.

7. Chemicals

The inflationary cost scenario continued to put pressure on the profitability of the sector in 1QFY23. However, we saw better QoQ performance on the gross margin side as the companies resumed pass-on of elevated raw material prices. The EBITDA margin of the industry was stable with a downward bias as power and freights costs remained elevated. These costs are sticky and difficult to pass-on.

Aarti Industries

- Revenue/EBITDA/PAT grew 50%/18%/15% YoY supported by ramp up of new capacities, contribution from long term contracts and favourable realizations.

- USFDA approved API facility at Tarapur commenced operations.

- Outlook was positive with Rs 30bn planned investments over next two years, utilization level of first two contracts targeted at 80% and investments (Rs 1.5-2bn) into backward integration of nitration facility commissioning by FY24 thereby improving asset turns and return ratios.

PI Industries

- Phenomenal growth in CSM business (42% YoY on a high base) led to 29% YoY growth in revenues and 155bps OPM improvement. Domestic business was muted with 4% YoY growth impacted by delayed monsoon.

- Outlook was positive with 20% (earlier guidance of 18-20%) revenue growth guidance, Rs 6-6.5bn capex guidance (significant step-up) and 7 new molecule commercializing in FY23.

Neogen Chemical

- Revenue grew 75% YoY led by inorganic chemicals which grew 241% YoY. Organic chemicals grew 32% YoY. Gross margin was largely stable (-20bps YoY) but EBITDA margin contracted 180bps YoY owing to higher operating costs.

- Planned capex of Rs 1.5bn in FY23 at Dahej for expansion in organic chemicals (+60Kl), doubling capacity of inorganic salts (+1,200MT) and new inorganic MPP (400MT) augurs well for future growth.

- Mgmt. gave revenue guidance of Rs 6bn with 18.5% OPM for FY23.

8. Pharma / Healthcare

Continuation of growth trends of past 3 quarters: India portfolio (ex-COVID) of leading companies grew 10-12% YoY. This was led by recovery in Chronic therapy and stabilizing Acute (ex- Anti-Infective). US price erosion continued in the range of 8-10% with no respite. Companies like Sun/Cipla bucked the trend on the back of speciality products contribution. CDMO business of companies like Laurus / Suven / Divi’s saw good growth on the back of COVID drug opportunity.

Margin headwinds galore: Consumption of expensive inventory led to Gross margin pressure which was accentuated by high power and freight expense and forex loss in some cases. Return of discretionary spend further added to EBITDAM pressure.

Outlook: Solvent prices are stabilizing at current levels which should lead to margin improvement from H2FY23 for API companies. US generics recovery hinges on price stabilization, new product approval and facility clearance. Despite all this, the competition is increasing with very different market dynamics as compared to 2015-16 peak. Expect companies with strong domestic portfolio to continue outperforming followed by CDMO and API companies. US generic growth will depend on product launches and speciality product pipeline.

CONCLUSION:

- Strong performance to continue: We expects strong revenue and margins for consumer discretionary companies in the coming quarters. As highlighted earlier, formalisation is the biggest theme that is expected to play out in the coming years across categories. This theme has only got accentuated due to Covid, as unorganised players were on a weaker footing to bear the storm. Banks are also looking to grow at an aggressive pace after getting disrupted by the covid storm. Large banks have come out of the storm unscathed, with cleaner balance sheet and stronger liability franchise.

- India is relatively better positioned: Compared with other major economies, India stands tall in terms of economic indicators and growth prospects. India’s share in the global supply chain is expected to rise on the back of Government schemes such as PLI. As the growth picks up, utilization rate will increase, which is followed by private sector capex. Two major ingredients for private capex are (a) long-term visibility of high demand (b) Balance sheet strength to take on more debt. Most of our Investee companies such as Safari, Page Industries, Orient Electric, Aarti Industries are in the process of increasing their capacity. Going forward we believe that fundamentals of the Indian economy are on a strong footing and we shall remain the fastest growing economy in the world.

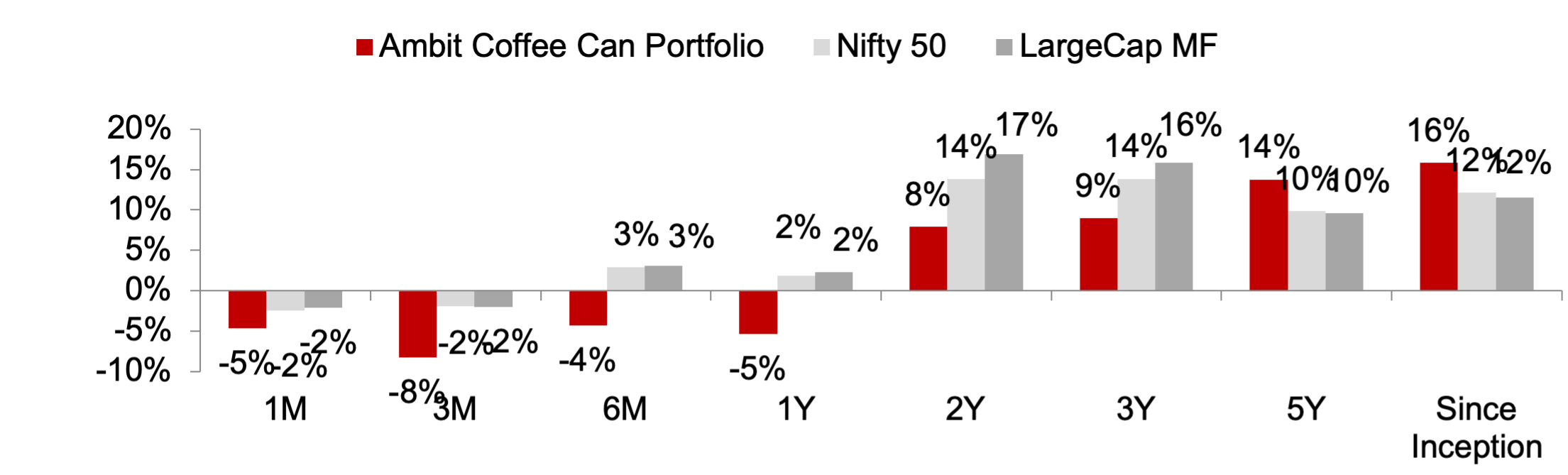

Ambit Coffee Can Portfolio

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced by disruptions at regular intervals. As the industry evolves or is faced by disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

Exhibit 11: Ambit’s Coffee Can Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of 31st Aug, 2022; All returns are post fees and expenses; Returns above 1-year are annualized; Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts.

Exhibit 12: Ambit’s Coffee Can Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of 31st Aug, 2022; All returns are post fees and expenses. Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts.

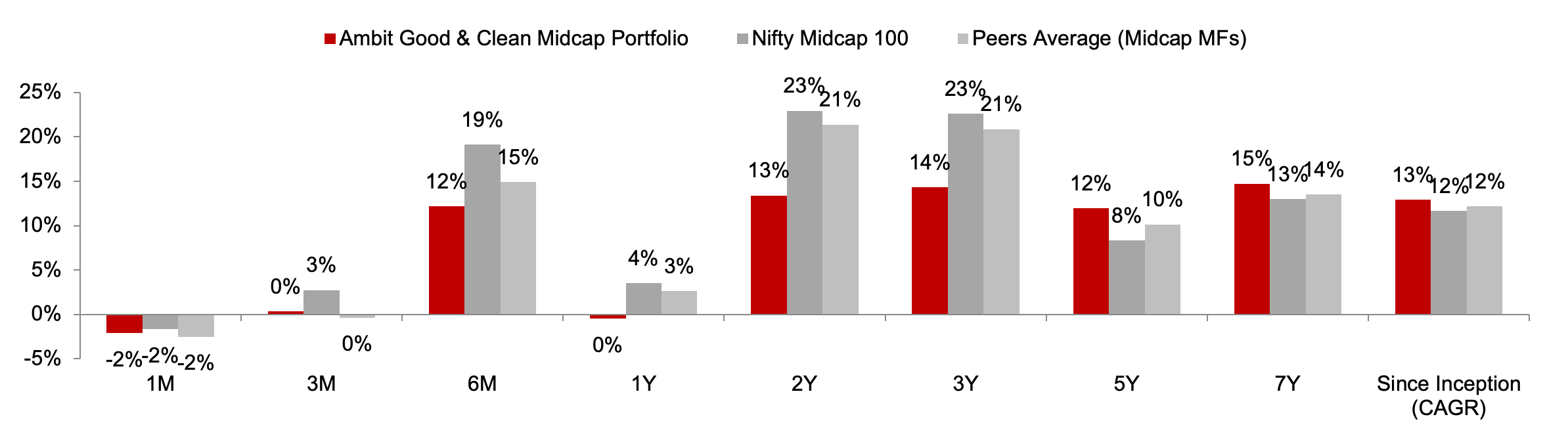

Ambit Good & Clean Midcap Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver superior risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

- Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

- Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longer with annual churn not exceeding 15-20% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with this compounding earnings acting as the primary driver of investment returns over long periods.

- Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

Exhibit 13: Ambit’s Good & Clean Midcap Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of 31st Aug, 2022; All returns above 1 year are annualized. Returns are net of all fees and expenses

Exhibit 14: Ambit’s Good & Clean Midcap Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of 31st Aug, 2022. Returns are net of all fees and expenses

Ambit Emerging Giants Portfolio

Smallcaps with secular growth, superior return ratios and no leverage –Ambit's Emerging Giants portfolio aims to invest in small-cap companies with market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than Rs4,000cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt) and ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence lead us to a concentrated portfolio of 15-16 emerging giants.

Exhibit 15: Ambit Emerging Giants Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of 31stAug, 2022; All returns above 1 year are annualized. Returns are net of all fees and expenses

Exhibit 16: Ambit Emerging Giants Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of 31stAug, 2022. Returns are net of all fees and expenses

Ambit TenX Portfolio

Ambit TenX Portfolio gives investors an opportunity to participate in the India growth story as the Indian GDP heads towards a US$10tn mark over the next 12-15 years. Mid and Small corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that can grow their earnings 10x over the same period implying 18-21% CAGR. Key features of this portfolio would be as follow:

- Longer-term approach with a concentrated portfolio: Ideal investment duration of >5 years with 15-20 stocks.

- Key driving factors: Low penetration, strong leadership, light balance sheet

- Forward-looking approach: Relying less on historical performance and more on future potential while not deviating away from the Good & Clean philosophy.

- No Key-man risk: Process is the Fund Manager

Exhibit 17: Ambit TenX Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of 31stAug, 2022; Returns are net of all fees and expenses

Exhibit 18: Ambit TenX Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of 31stAug, 2022. Returns are net of all fees and expenses

For any queries, please contact:

Umang Shah- Phone: +91 22 6623 3281, Email - [email protected]

Ambit Investment Advisors Private Limited -

Ambit House, 449, Senapati Bapat Marg,

Lower Parel, Mumbai - 400 013

Risk Disclosure & Disclaimer

The performance of the Portfolio Manager has not been approved or recommended by SEBI nor SEBI certifies the accuracy or adequacy of the performance related information contained therein. Ambit Investment Advisors Private Limited (“Ambit”), is a registered Portfolio Manager with Securities and Exchange Board of India vide registration number INP000005059. This presentation / newsletter / report is strictly for information and illustrative purposes only and should not be considered to be an offer, or solicitation of an offer, to buy or sell any securities or to enter into any Portfolio Management agreements. This presentation / newsletter / report is prepared by Ambit strictly for the specified audience and is not intended for distribution to public and is not to be disseminated or circulated to any other party outside of the intended purpose. This presentation / newsletter / report may contain confidential or proprietary information and no part of this presentation / newsletter / report may be reproduced in any form without its prior written consent to Ambit. All opinions, figures, charts/graphs, estimates and data included in this presentation / newsletter / report is subject to change without notice. This document is not for public distribution and if you receive a copy of this presentation / newsletter / report and you are not the intended recipient, you should destroy this immediately. Any dissemination, copying or circulation of this communication in any form is strictly prohibited. This material should not be circulated in countries where restrictions exist on soliciting business from potential clients residing in such countries. Recipients of this material should inform themselves about and observe any such restrictions. Recipients shall be solely liable for any liability incurred by them in this regard and will indemnify Ambit for any liability it may incur in this respect.

Neither Ambit nor any of their respective affiliates or representatives make any express or implied representation or warranty as to the adequacy or accuracy of the statistical data or factual statement concerning India or its economy or make any representation as to the accuracy, completeness, reasonableness or sufficiency of any of the information contained in the presentation / newsletter / report herein, or in the case of projections, as to their attainability or the accuracy or completeness of the assumptions from which they are derived, and it is expected each prospective investor will pursue its own independent due diligence. In preparing this presentation / newsletter / report, Ambit has relied upon and assumed, without independent verification, the accuracy and completeness of information available from public sources. Accordingly, neither Ambit nor any of its affiliates, shareholders, directors, employees, agents or advisors shall be liable for any loss or damage (direct or indirect) suffered as a result of reliance upon any statements contained in, or any omission from this presentation / newsletter / report and any such liability is expressly disclaimed. Further, the information contained in this presentation / newsletter / report has not been verified by SEBI.

You are expected to take into consideration all the risk factors including financial conditions, risk-return profile, tax consequences, etc. You understand that the past performance or name of the portfolio or any similar product do not in any manner indicate surety of performance of such product or portfolio in future. You further understand that all such products are subject to various market risks, settlement risks, economical risks, political risks, business risks, and financial risks etc. and there is no assurance or guarantee that the objectives of any of the strategies of such product or portfolio will be achieved. You are expected to thoroughly go through the terms of the arrangements / agreements and understand in detail the risk-return profile of any security or product of Ambit or any other service provider before making any investment. You should also take professional / legal /tax advice before making any decision of investing or disinvesting. The investment relating to any products of Ambit may not be suited to all categories of investors. Ambit or Ambit associates may have financial or other business interests that may adversely affect the objectivity of the views contained in this presentation / newsletter / report.

Ambit does not guarantee the future performance or any level of performance relating to any products of Ambit or any other third party service provider. Investment in any product including mutual fund or in the product of third party service provider does not provide any assurance or guarantee that the objectives of the product are specifically achieved. Ambit shall not be liable for any losses that you may suffer on account of any investment or disinvestment decision based on the communication or information or recommendation received from Ambit on any product. Further Ambit shall not be liable for any loss which may have arisen by wrong or misleading instructions given by you whether orally or in writing. The name of the product does not in any manner indicate their prospects or return.

The product ‘Ambit Coffee Can Portfolio’ has been migrated from Ambit Capital Private Limited to Ambit Investments Advisors Private Limited. Hence some of the information in this presentation may belong to the period when this product was managed by Ambit Capital Private Limited. You may contact your Relationship Manager for any queries.

The performance data for coffee can product between 6th march 2017 - 19th June 2017 represents model portfolio returns. First client was onboarded on 20th June 2017. The performance data for G&C product between 1st June 2016 to 1st April 2018 also includes returns for funds managed for an advisory offshore client. Returns are calculated using TWRR method as prescribed under revised SEBI (Portfolio Managers) Regulations, 2020.