.png)

FY24-25 has been a tough year for India’s chemical sector

FY24-25 period saw significant deceleration in both revenue and EBITDA CAGR across several sub-sectors of chemicals when compared to the golden period of FY21-23; during FY23-25 the revenue CAGR was just 1% in commodity chemicals/ -12% in specialty chemicals and 3% in agrochemicals segment while EBITDA CAGR was 2%/-5% and -6% in respective sub-segments. EBITDA margin contraction was ~500bps across 3 sub-segments to average of 14% vs 19% in FY23. The sector did exceptionally well during the golden era of FY21-23 as revenue CAGR was 27% in commodity chemicals/ 57% in specialty chemicals and 24% in agro segment. The worst sub-sectors during FY23-25 were Amines which reported revenue/EBITDA CAGR of -14%/-26% vs the golden era CAGR of 26%/9%, Alkali chemicals -10%/-32% revenue and EBITDA CAGR over FY23-25 vs 36%/64% CAGR over FY21-23 and oleochemicals 39%/47% vs -7%/-16% CAGR.

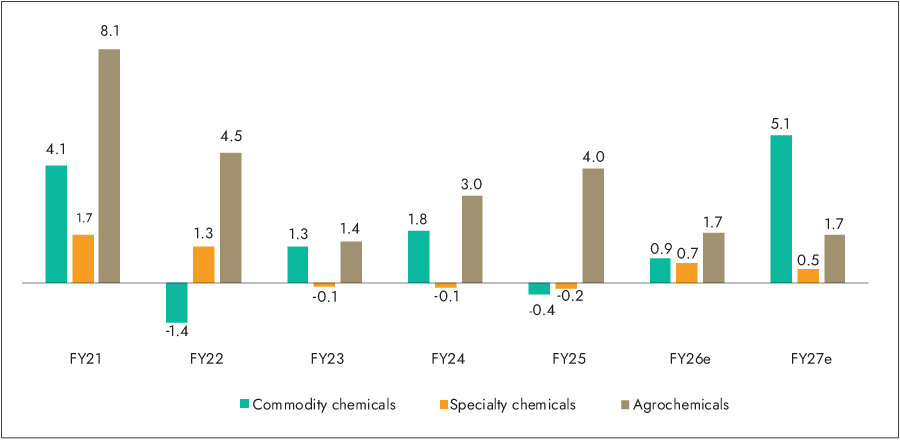

Exhibit 1: Revenue growth in bull and bear run over FY21-25 across sectors

1752151737463.jpg)

Source: Company, Bloomberg, Ambit Asset Management

Exhibit 2: EBITDA growth in bull and bear run over FY21-25 across sectors

1752151746715.jpg)

Source: Company, Bloomberg, Ambit Asset Management

Exhibit 3: Profit growth in bull and bear run over FY21-25 across sectors

1752151752424.jpg)

Source: Company, Bloomberg, Ambit Asset Management

Exhibit 4: EBITDA margin in bull and bear run over FY21-25 across sectors

1752151758522.jpg)

Source: Company, Bloomberg, Ambit Asset Management

Exhibit 5: Valuation also saw significant de-rating with P/E and EV/EBITDA multiples correcting by ~13% to ~10% across sub-sectors, majorly in spechem

1752151765053.jpg)

Source: Company, Bloomberg, Ambit Asset Management

Exhibit 6: FII ownership declined during this period (~35 companies)

1752151771346.jpg)

Source: Company, Bloomberg, Ambit Asset Management

Why FY20-22 was a golden period for Indian chemical companies?

Covid period allowed the chemical companies to make record margins led by supply chain constraints from China which led to significant jump in pricing and resultant margins. Globally chemical companies started stocking excess inventories to ensure there is no production disruption given China which is the largest exporter of chemicals was seeing supply chain constraints.

Exhibit 7: Covid and De-stocking saw global inventory rising to record levels as manufacturers' inventories to shipment ratio peaked in 2020

1752151777976.jpg)

Source: U.S. Census Bureau via FRED, Ambit Asset Management

Exhibit 8: Freight rates peaked led by supply chain disruptions

1752151787368.jpg)

Source: Bloomberg, Ambit Asset Management

Street community got exited on the back of chemical companies reporting good results and this led to several upgrades to the sector. Street started extrapolating the record margins to FY22-25 period as well and resultantly the sector saw ~73% buys and outperformer ratings; coverage for chemical companies also started rising significantly.

Exhibit 9: EBITDA margin improved ~200-500bps over FY19-23 across sectors

1752151795579.jpg)

Source: Bloomberg, Ambit Asset Management

Exhibit 10: …as they started extrapolating record margins of FY22 to FY22-25 period

1752151803296.jpg)

Source: Bloomberg, Ambit Asset Management

Exhibit 11: ....resultantly the sector saw ~73% buys and outperformer ratings

1752151810193.jpg)

Source: Bloomberg, Ambit Asset Management

Post FY22 the downfall started

With channel inventory at historic high levels in FY22 and easing supply chain disruptions from China the demand exuberance started waning and resultantly the downfall in pricing for Indian chemical companies started. The capex announced during FY21-22 further compounded the sector’s woes as rising debt (to fund the capex) strained profitability further.

Exhibit 12: Starting CY23 prices for chemicals started correcting as supply chain disruptions eased out from China

1752152235128.jpg)

Source: Sector Data, Bloomberg, Ambit Asset Management

Exhibit 13: Actual margin performance was weaker than analyst expansions for FY23-35

1752152249874.jpg)

Source: Bloomberg, Ambit Asset Management

Exhibit 14: Rising balance sheet debt on the back of chemical companies announcing capex post record profits in FY22 further impacted profitability

1752152257559.jpg)

Source: Bloomberg, Ambit Asset Management

Why we remain bullish on the sector for FY25-27?

There are three main reasons why we are bullish on the sector: (a) global inventory is at par to decadal levels; (b) finished goods prices have started bottoming out across several products and (c) capex cycle is behind us implying strong FCF generation if revenue growth starts improving.

Exhibit 15: Inventory to shipment ratio declining which would result in volume growth

1752152266125.jpg)

Source: U.S. Census Bureau via FRED, Ambit Asset Management

Exhibit 16: Chemicals output across the market is expected to grow after being weak over 2022-24, largely supported by Asia pacific region

1752152277916.jpg)

Source: ACC situation & Outlook (Dec’24), Ambit Asset Management

- Pricing bottoming out across several products with sector tailwinds: The sector’s realization growth indicates higher dependence on crude oil prices as petrochemicals are the primary raw material for the industry. Crude prices were at average ~$99/bbl which supported strong realization growth in 2022 vs declining crude prices at US$82/bbl in 2024 putting realization pressure on the industry. In the recent pricing data, it is clear that realization looks bottomed out and expected to remain at this level or improve from here on. Asia-Pacific region is projected to lead global growth, driven by strong domestic demand, infrastructure investments, and government support. Countries like India are experiencing significant expansion in chemical production due to a growing industrial base, robust manufacturing capabilities, and increased consumer demand. (Refer exhibit 12)

- FCF to see significant growth over FY25-27 despite some pick-up in capex over FY26-28 on import substitution, CDMO and export opportunities: Companies have consistently added new product capabilities to maintain their growth aspirations. The capex of Rs89bn in FY21 over 36 companies rose to Rs133bn in FY22 and Rs167bn in FY23. The capex intensity subsequently declined to Rs142bn in FY24 and Rs148bn in FY25 due to uncertain demand and pricing environment. We expect capex to revive again from FY26 with focus on rising export and import substitution opportunities. The new products are forward-integrated into the existing product portfolio, such as fluoropolymers for SRF, phenol/acetone downstream for Deepak Nitrite, chloro-toluene value chain for Aarti Industries antioxidants for Vinati, etc. Companies like PI and SRF are also building on their capabilities to venture into new categories like pharma CRDMO, API and intermediates. We expect these companies to continue to build on their capabilities given: a) customer relations, b) global footprint, and c) operational track record supported by sound balance sheets. They will continue to leverage their learning of the last two decades and increase their wallet share in export markets. They will continue to attract new business given their operational delivery and process capabilities supported by R&D.

Exhibit 17: Capex cycle to continue to bake growing opportunities rising in import substitution, CDMO and exports

1752152285915.jpg)

Source: Bloomberg, Ambit Asset Management

Despite, some surge in capex, we model significant growth in FCF as seen in the chart below led by strong earnings growth and improvement in working capital cycle. We have seen that industry was generating ~Rs104bn FCF in FY21 which declined to Rs27bn/76bn/31bn over FY22-24. As the company’s performance expected to improve on the back of demand, pricing and margin betterment coupled with operating efficiencies, FCF is expected to increase to Rs83bn/74bn and 108bn over FY25-27, despite ongoing capex across import substitution, CDMO and export opportunities.

Exhibit 18: FCF to remain healthy despite ongoing capex cycle

1752152292936.jpg)

Source: Bloomberg, Ambit Asset Management

Foreign Institutional Investors (FIIs) have been quietly increasing exposure to the chemical sector since the last 9 months given their knowledge of the global chemical cycle. Similar behavior we saw from them in 2022 to 2024 when they did this in Auto and Capital Goods sectors from 2022 to 2024 giving them handsome rewards.

- Valuation has become favourable as sector trades at discount to long term average:

Valuations across chemical companies are now at discount compared to 5 year averages and FCF yields are promising. We believe this gives a lot of margin of safety for investors to make money if they are patient enough to ride the cycle.

Exhibit 19: Valuation looks reasonable considering industry tailwinds

1752152300774.jpg)

Source: Bloomberg, Ambit Asset Management

Exhibit 20: DIIs shareholding (%) in chemical sectors has been going up now for 6 quarters (Top 15 companies seeing this trend)

1752152310532.jpg)

Source: Bloomberg, Ambit Asset Management

Exhibit 21: FIIs shareholding (%) in chemical sectors has been going up now for 6 quarters (Top 15 companies seeing this trend)

1752152318458.jpg)

Source: Bloomberg, Ambit Asset Management

Exhibit 22: Similar behavior we saw from FIIs in auto and capital goods sector in 2022 to 2024 which gave them handsome rewards (% of inflows and outflow)

1752152787334.jpg)

Source: Bloomberg, Ambit Asset Management

Exhibit 23: FCF yield on FY27 looks promising …

Source: Bloomberg, Ambit Asset Management

We are bullish on chemicals across all our portfolio strategies and few of our portfolio picks are as given below:

Alkyl Amines

We anticipate Alkyl’s performance to strengthen from FY26 onward, supported by a:

- Positive outlook for its core end-user industries—pharmaceuticals and agrochemicals.

- Ministry of Finance has approved an anti-dumping duty of ~12–28% on acetonitrile imports from China, Russia, and Taiwan, which collectively account for a~90% of such imports which expected to alleviate pricing pressure starting FY26.

- Alkyl is also undertaking a capex of Rs1bn towards a specialty product, further reinforcing its growth trajectory.

- The company boasts a diversified product portfolio, disciplined capital allocation, and a robust balance sheet, all under the leadership of a technocrat promoter.

Neogen Chemicals

Neogen Chemicals is one of India’s leading manufacturers of Bromine –based and Lithium based specialty chemicals. The recent fire accident at Neogen’s Dahej SEZ plant coupled with timelines for ramping up the battery chemical business continue to be pushed out led by delays in commissioning of Lithium ion battery plants which hurt performance in recent times However, long term performance looks promising considering:

- Neogen is the best play in the battery chemical space considering available capacities with Japanese proven technology.

- Revival in agrochemical cycle.

- Rising opportunities in CDMO side which going to support growth in base business.

PI Industries

Despite headwinds in the agrochemical industry during FY23–25, PI Industries delivered a strong performance, achieving a CAGR of 19% in revenue, 21% in EBITDA, and 21% in PAT with EBITDA margin of expanding by ~350bps to 27% in FY25. Looking ahead, we expect PI Industries to:

- Maintain its growth momentum, supported by global recovery in agrochemical demand.

- Robust cash reserve of ~Rs40bn, enabling potential inorganic growth opportunities.

- Continued scaling of its Pharma segment, driving further margin improvement and commercialization of its novel agrochemical molecule.

- Pioxaniliprole—a next-generation diamide insecticide. Notably, PI is the only Indian chemical company currently developing an agchem New Chemical Entity (NCE). Pioxaniliprole is in Phase III trials and is anticipated to be commercialized in the coming years, reinforcing the company’s leadership in innovation.

Insecticides India

Well positioned to capitalise on the thriving agrochemical sector:

- Company is focusing on its high margin Maharatna and Focus Maharatna products, which will drive profitability improvement.

- Senior hires undertaken of several GM level employees; discussions are ongoing with CXO level employees with strong incentive packages which will provide human capital boost.

- Production from Gujarat facility will commence in June 2025 - with a sales potential for INR 350-400cr over 3 years. The capex in Rajasthan, which will be completed by June 2026, has a similar revenue potential.

Exhibit 24: Price performance/charts

Source: Bloomberg, Ambit Asset Management

Summary

- Post-COVID Overconfidence: FY20–22 boom led to overcapacity and unrealistic growth expectations in the chemical sector.

- Reality Check: Peaking inventories, falling realizations, and high fixed costs triggered a prolonged downcycle.

- Capex Strain: Aggressive investments during the upcycle became burdensome as demand softened, impacting profitability and leverage.

- Stabilization Phase: Inventory levels are now leaner, and pricing pressures have largely bottomed out, creating a more balanced environment.

- Shift to Value Creation: Companies are moving from expansion to execution—focusing on complex, higher-margin segments like pharma intermediates, agro-specialties, CDMO, and advanced materials.

- India’s Advantage: Regional momentum, policy support, and global supply chain diversification are boosting India’s role in the chemical value chain.

- Outlook Turning Positive: With cash flows recovering, margins poised to expand, and balance sheets repairing, the sector is set for a potential rerating.

- Cycle Reset Completed: What seemed like a deep trough may mark the beginning of a more resilient and strategically sound growth phase.

- We believe Indian chemicals and particularly sub-segments like agrochemicals, contract manufacturing, import substitution, and supply diversification are poised for a structural recovery, and our portfolios are well placed to take advantage of the same.

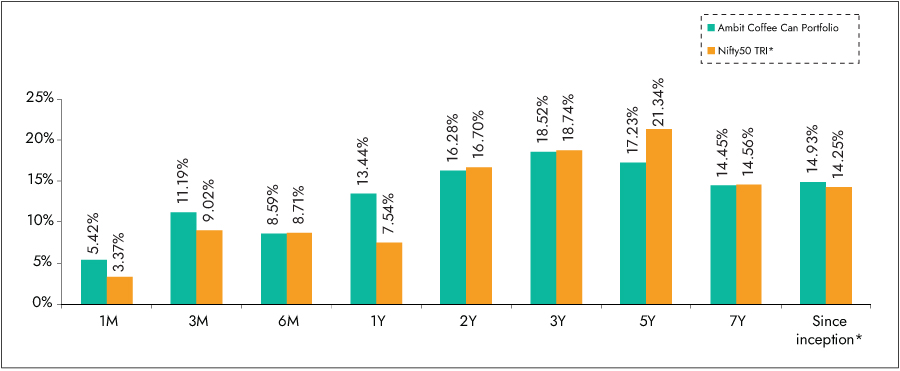

Ambit Coffee Can Portfolio

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and

consumption-oriented sectors. The Coffee Can philosophy has an unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced with disruptions at regular intervals. As the industry evolves or is faced with disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

Exhibit 25: Ambit Coffee Can Portfolio point-to-point performance

Source: Ambit Coffee Can Portfolio inception date is June 20, 2017;

**1M Return: 1st - 30th Jun'25; 3M Return: 1st Apr'25 – 30th Jun'25; 6M Return: 1st Jan'25 – 30th Jun'25; 1Y Return: 1st Jul'24 – 30th Jun'25

*Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The performance related information provided herein is not verified by SEBI.

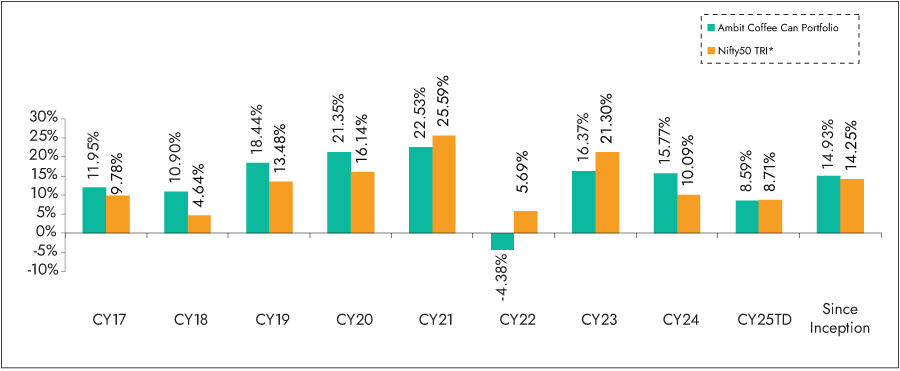

Exhibit 26: Ambit Coffee Can Portfolio calendar year performance

Source: Ambit Coffee Can Portfolio inception date is June 20, 2017;

*Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The performance related information provided herein is not verified by SEBI.

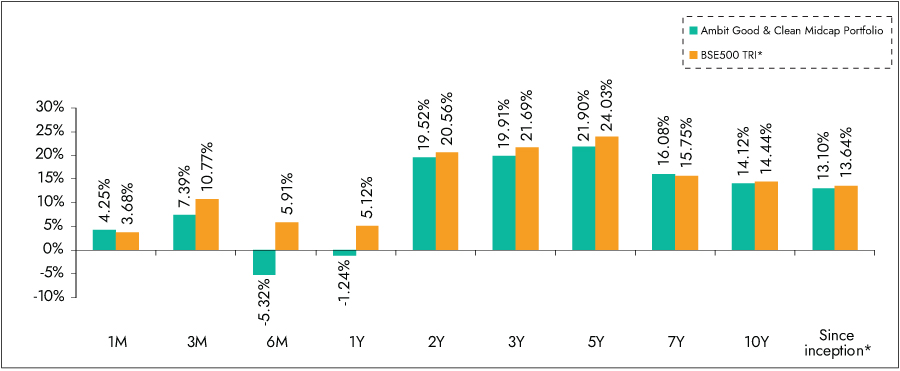

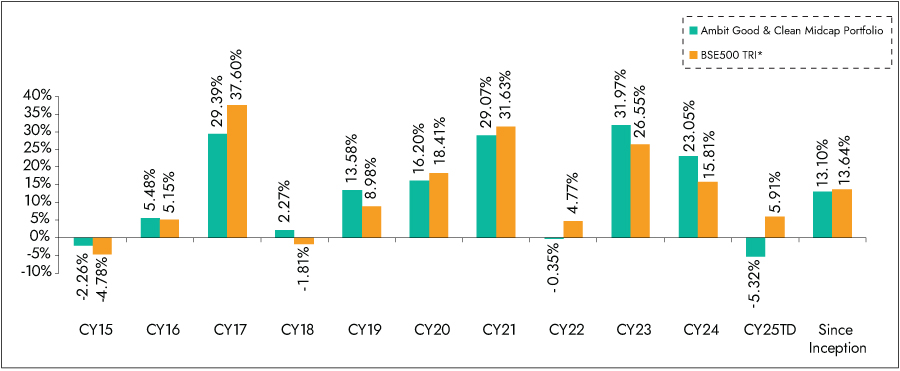

Ambit Good & Clean Midcap Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver superior

risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

1. Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

2. Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longerwith annual churn not exceeding20-25% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with these compounding earnings acting as the primary driver of investment returns over long periods.

3. Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

Exhibit 27: Ambit Good & Clean Midcap Portfolio point-to-point performance

Source: Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015;

**1M Return: 1st - 30th Jun'25; 3M Return: 1st Apr'25 – 30th Jun'25; 6M Return: 1st Jan'25 – 30th Jun'25; 1Y Return: 1st Jul'24 – 30th Jun'25

*BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Mid cap. The performance related information provided herein is not verified by SEBI.

Exhibit 28: Ambit Good & Clean Midcap Portfolio calendar year performance

Source:Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015;

*BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Mid cap. The performance related information provided herein is not verified by SEBI.

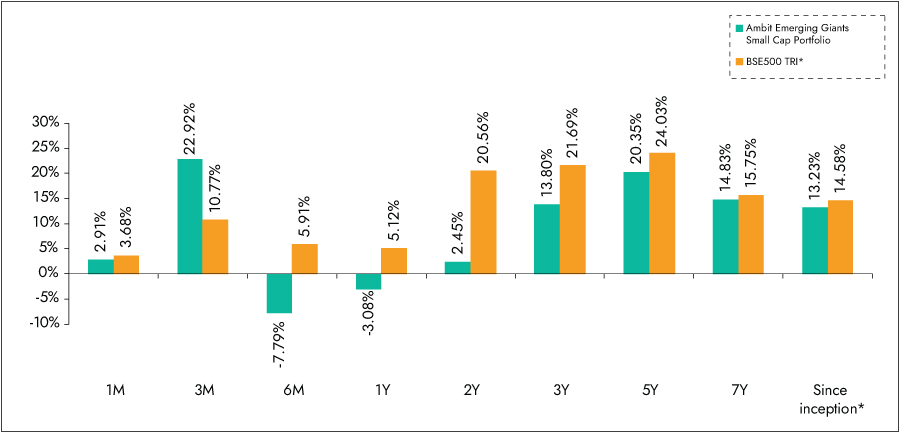

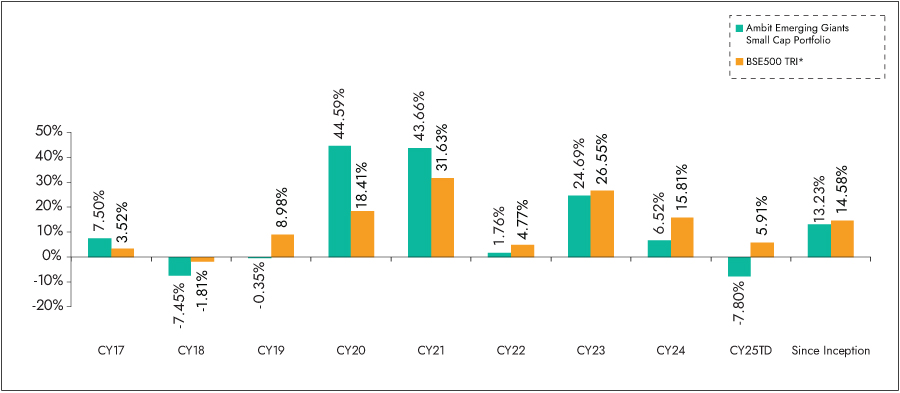

Ambit Emerging Giants Small Cap Portfolio

Small caps with secular growth, superior return ratios and no leverage – Ambit's Emerging Giants Small Cap portfolio aims to invest in small-cap companies with

market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than INR 10,000cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt), and the ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence led us to a

concentrated portfolio of 18-20 emerging giants.

Exhibit 29: Ambit Emerging Giants Small Cap Portfolio point-to-point performance

Source: Ambit Emerging Giants Small cap Portfolio inception date is Dec 1, 2017;

**1M Return: 1st - 30th Jun'25; 3M Return: 1st Apr'25 – 30th Jun'25; 6M Return: 1st Jan'25 – 30th Jun'25; 1Y Return: 1st Jul'24 – 30th Jun'25

*BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants Small cap. The performance related information provided herein is not verified by SEBI.

Exhibit 30: Ambit Emerging Giants Small Cap Portfolio calendar year performance

Source: Ambit Emerging Giants Small cap Portfolio inception date is Dec 1, 2017;

*BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants Small cap. The performance related information provided herein is not verified by SEBI.

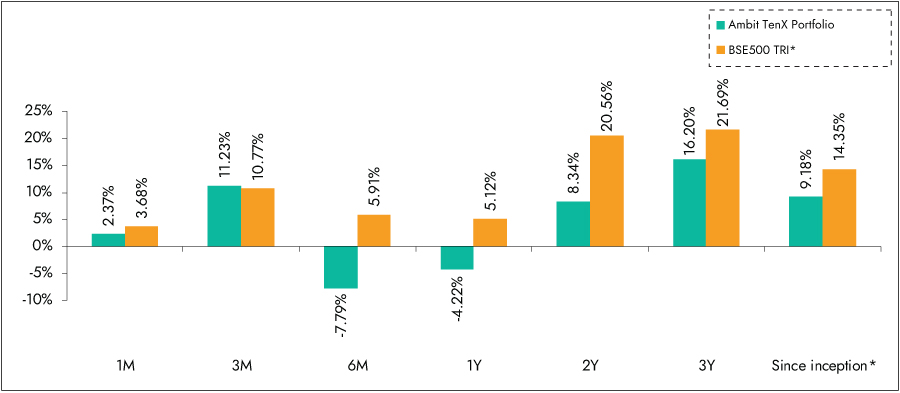

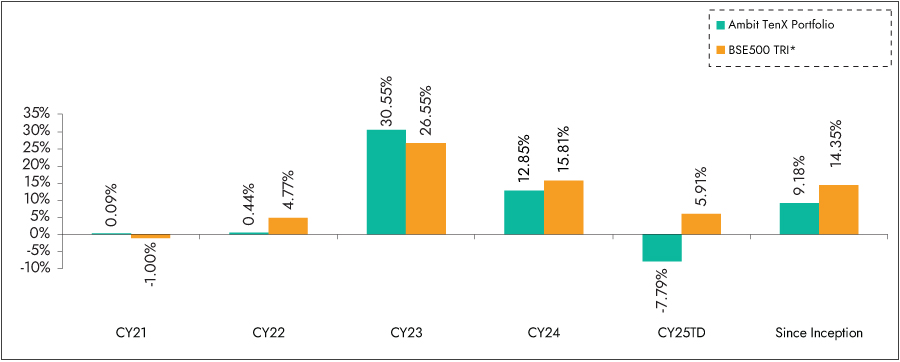

Ambit TenX Portfolio

Ambit TenX Portfolio gives investors an opportunity to participate in the India growth story as the Indian GDP heads towards a US$10tn mark over the next 12-15 years. Mid and Small corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that can grow their earnings 10x over the same period implying 18-21% CAGR. Key features of this portfolio

would be as follows: Key features of this portfolio would be as follows:

1. Longer-term approach with a concentrated portfolio: Ideal investment duration of >5 year with 15-20 stocks.

2. Key driving factors: Low penetration, strong leadership, light balance sheet.

3. Forward-looking approach: Relying less on historical performance and more on future potential while not deviating away from the Good & Clean philosophy.

Exhibit 31: Ambit TenX Portfolio point-to-point performance

Source: Ambit TenX Portfolio inception date is Dec 13, 2021;

**1M Return: 1st - 30th Jun'25; 3M Return: 1st Apr'25 – 30th Jun'25; 6M Return: 1st Jan'25 – 30th Jun'25; 1Y Return: 1st Jul'24 – 30th Jun'25

*BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio. The performance related information provided herein is not verified by SEBI.

Exhibit 32: Ambit TenX Portfolio calendar year performance

Source: Ambit TenX Portfolio inception date is Dec 13, 2021;

*BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio. The performance related information provided herein is not verified by SEBI.

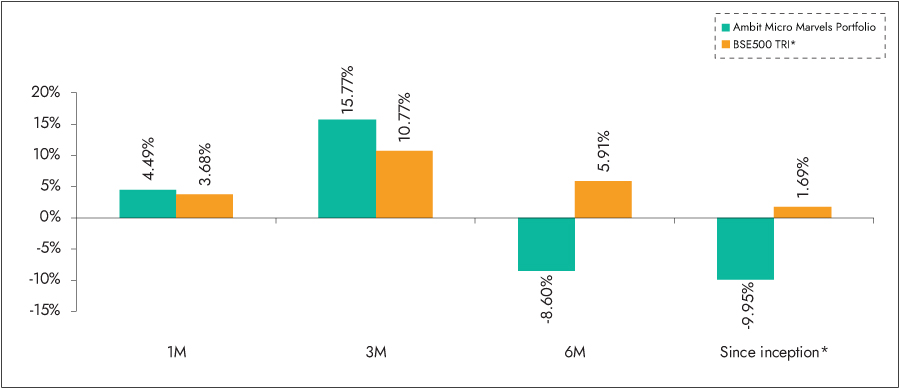

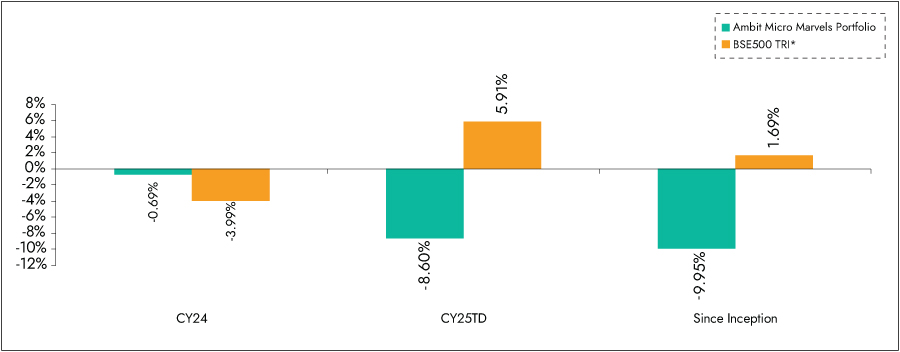

Ambit Micro Marvels Portfolio

We aim to create a portfolio that invests predominantly in micro-cap companies with the potential of delivering superior earnings growth and generating relatively better risk-adjusted performance over a long period of time.

Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts while our proprietary ‘greatness’ framework helps identify efficient capital allocators. The result is a concentrated portfolio of 20-25 stocks that draws down less than the market in corrections and has low churn.

Key Features of Portfolio Companies:

1. High earnings growth companies with low leverage,

2. Market leaders or challengers with strong moat around brand, distribution, technology, and innovation,

3. Strong corporate governance coupled with apt capital allocation.

Exhibit 33: Ambit Micro Marvels Portfolio point-to-point performance

Source: Ambit Micro Marvels Portfolio inception date is Jul 29, 2024;

**1M Return: 1st - 30th Jun'25; 3M Return: 1st Apr'25 – 30th Jun'25; 6M Return: 1st Jan'25 – 30th Jun'25; 1Y Return: 1st Jul'24 – 30th Jun'25

*BSE 500 TRI is the selected benchmark for the Ambit Micro Marvels Portfolio. The performance related information provided herein is not verified by SEBI.

Exhibit 34: Ambit Micro Marvels Portfolio calendar year performance

Source: Ambit Micro Marvels Portfolio inception date is Jul 29, 2024;

*BSE 500 TRI is the selected benchmark for the Ambit Micro Marvels Portfolio. The performance related information provided herein is not verified by SEBI.