In this newsletter, we explore:

- What is ergodicity? A foundational look at what the term means and why it matters.

- Key learnings for long-term investors: Practical takeaways from the book that can help investors build resilience into portfolios

- Managing non-ergodicity: Understanding ergodicity as a non-binary concept, and why managing irreversible downside is critical.

- The ludic fallacy in investing - How to spot—and avoid—oversimplified models of risk that ignore real-world uncertainty.

1. What does ergodicity mean?

Luca Dellanna defines ergodicity as follows: “A system is ergodic if, for all its components, the lifetime outcome corresponds to the population outcome. Otherwise, it is non-ergodic.” In simple terms, a system is ergodic when the average outcome across the population is the same as the average outcome over time for an individual. If this equivalence does not hold, the system is non-ergodic. While ergodicity may seem abstract, it has very real consequences—especially for investors. Dellanna emphasizes that ergodicity is a binary property: either the individual and population outcomes align, or they don’t. There’s no middle ground. In non-ergodic systems, irreversible consequences—such as ruin, death, or financial blow-up—alter the future path of an individual in ways that the population average fails to capture. A simple test to assess ergodicity is this: “Are there irreversible consequences?” If yes, the system is non-ergodic.

In ergodic systems, population-level outcomes can be used to make optimal decisions. For example, in casino games with fair odds and unlimited tries, the law of large numbers helps guide strategy.

However, in non-ergodic systems—such as investing, entrepreneurship, or life itself—irreversible losses distort the picture. You don’t get unlimited retries, and a single negative event (e.g., bankruptcy) can end your participation in the system altogether. This insight has significant implications for capital allocation. It explains why risk management isn’t just prudent—it’s essential. In non-ergodic environments, survival is the precondition for success. Optimizing for returns without accounting for irreversible downside is not just risky—it’s flawed.

Exhibit 1: Examples of Ergodic and Non-Ergodic systems

Source: Book Ergodicity by Luca Dellanna, Ambit Asset Management

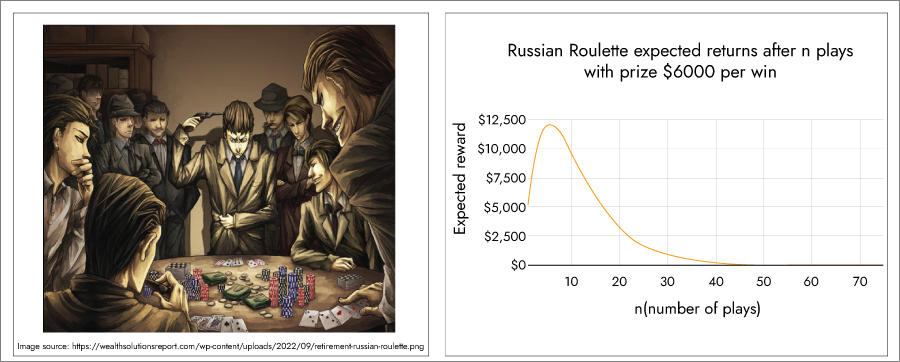

Russian roulette - Example of non-ergodicity

Russian roulette is a game of extreme risk involving a revolver with multiple chambers. Non-ergodic systems, like Russian roulette, behave differently. Luca underscores that Russian roulette is the archetype of non-ergodic scenarios: while group-level statistics may look promising, an individual’s repeated exposure reveals a starkly different—and far more dangerous—outcome.

How It Works: a) A revolver typically has six chambers in its cylinder; b) One bullet is placed into one of the chambers; c) The cylinder is spun, so the location of the bullet is random and unknown; d) The player places the gun to their head and pulls the trigger. The probability of firing a bullet is one-sixth and the probability of survival on a single pull is five-sixths. The danger grows dramatically with repeated plays because each round is independent, but a single failure ends the game permanently (death) for the individual. This is where non-ergodicity comes in — the key idea that group averages and individual experiences diverge. Hence, if one keeps playing the game because one fails to grasp its non-ergodicity and mistakenly believes that the lifetime outcomes equal the population one, one will end up dead instead of rich. One should aim to help avoid irreversible mistakes whose importance is apparent only after the fact.

From the house’s perspective (aggregate view): If 1,000 players each play Russian roulette once, on average, 1/6 will die per round, but the rest will survive. The aggregate data may suggest that the “system” is mostly fine.

From an individual’s perspective (time view): If one person plays repeatedly, it’s mathematically certain they will eventually die — their personal time-average outcome is catastrophic.

The Divergence: House/Gambler Difference: The house wins by looking at the ensemble — total profits across all players. The player lives or dies by their own time series — and even a single fatal event ends their game forever. This mirrors how many real-world systems work: what looks stable or profitable at a societal or corporate level may be lethal for individuals.

Exhibit 2: Russian roulette - odds of winning keep declining the more you play

Source: Book Ergodicity by Luca Dellanna, Ambit Asset Management

Application to Investing: In investing, the house is often money managers, hedge funds, brokers or the market as a whole. During a bull market, the house benefits immensely from people adopting risky strategies (options, leverage, meme stocks, speculative tech bets). Can even promote high-risk behaviour because it generates more fees and volume. They benefit from trading volume, management fees, and aggregate returns. Even if some clients lose everything, the house continues operating.

The individual investor is like the gambler: They live or die based on their personal portfolio performance over time. A single ruinous event (e.g., a margin call, total wipeout) ends their ability to stay in the game. This is more so in a bull market.

Implications for Investors

To avoid being the gambler, individuals must:

-

- Prioritize survival over maximizing returns. Focus on risk-adjusted returns, not just upside. Avoid strategies with a small probability of ruin (e.g., excessive leverage).

- Think in time-series terms. Ask: “If I repeat this strategy for 10 years, what’s the chance I go broke?”

- Adopt asymmetric bets with capped downside.

- Ignore herd behaviour in bull markets. Just because everyone seems to be winning doesn’t mean it’s sustainable.

2. Key learnings for long-term investors from “ergodicity”:

i. Irreversibility absorbs future gains – avoid game overs

- One source of non-ergodicity is irrecoverable situations, also known as “game overs.” For example, bankruptcy, death, social ostracization and permanent injuries. It is natural, then, that the first of the three strategies to manage non-ergodicity is to reduce exposure to game overs. The simplest and surest way is to not participate in activities that have such risks.

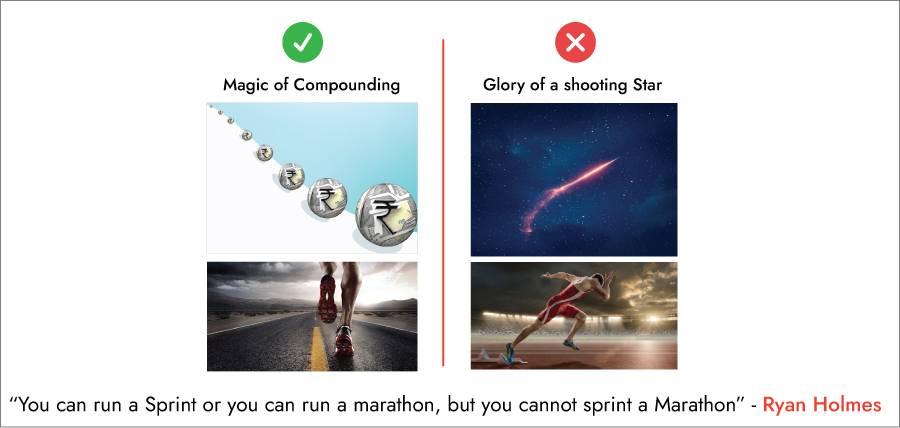

- History is full of examples where companies and investors, driven by the lure of fast success and unsustainable profits — “the glory of a shooting star” — end up taking game-over risks by engaging in reckless risks, shortcuts, and sharp practices. While these paths might offer short-term gains, they often lead to long-term disasters like loss of reputation, bankruptcies, regulatory crackdowns, etc., such as Enron (2001), Lehman (2008), Theranos (2016), Archegos Capital (2021), Wirecard (2020), FTX (2022), etc. Any form of “game over” nullifies future gains, bringing the average down.

- Any endeavour in which success depends on one accumulating some resource (money, skill, connections, trust etc.), one is better off not attempting to maximize growth at the cost of survival. Instead, one should try to grow in a manner that maximizes survival.

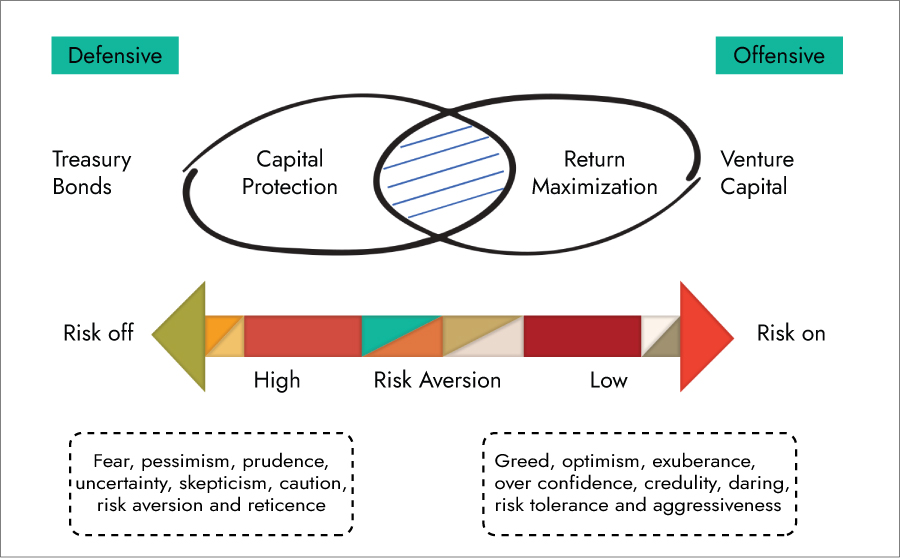

Exhibit 3: What risk tolerance spectrum an investor choses depends on the investor’s goal

Source: Ambit Asset Management

Examples of Irreversible losses:

- Investing: Losing your capital means not only losing the original amount invested but also forfeiting all the future returns that capital could have generated. This is a permanent setback in wealth creation.

- Sales and Business Reputation: A salesperson focused solely on maximizing quarterly sales might resort to aggressive or unethical tactics that damage the firm’s long-term brand and reputation. A good salesperson understands that short-term gains are never worth the irreversible loss of customer trust and brand equity.

- Yoga and Physical Health: In yoga, the goal is not to push the body to its maximum stretch in a single session. Instead, practitioners aim to grow gradually without risking injury. A serious injury can set one back for months or years — or worse, become permanent — representing an irreversible loss to physical ability. Hence, seeking short-term glory can come at the expense of a lifetime’s injury.

- Career and Personal Well-being: Working excessively hard in a way that compromises one’s health, relationships, or mental well-being is a dangerous trade-off. Burnout, chronic illness, or broken relationships can have lasting consequences that no professional success can undo. A company can replace key positions and move on; however, an individual must live with the consequences.

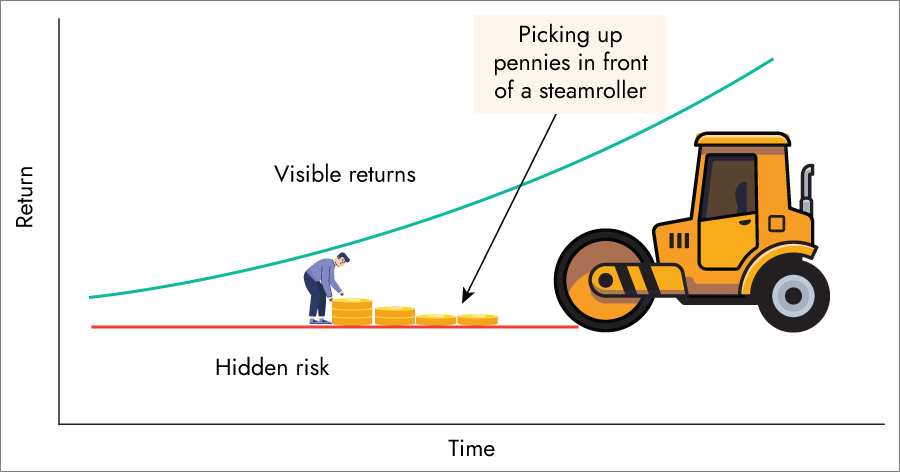

ii. Performance is subordinate to survival - The cost of short-term optimization

- Time horizons are the basis of our decisions and our regrets. The easiest way to increase short-term performance is to do so at the cost of long-term performance. When assessing short-term performance, it is essential to account for the cost of the risks taken to optimize outcomes—regardless of whether those risks have materialized yet. A single negative event can render short-term maximization irrelevant. Fortune favours the “living” brave.

- According to various Morningstar studies, the long-term survivorship rate for mutual funds can be extremely low. Over 20–25 years, survival alone (regardless of performance) drops closer to 3–10%, depending on the asset class. We can only observe the long-term outside of the short term. Over the short-term consequences that apply beyond the short term does not matter. Over the long term, they do.

- All decisions are underpinned by an implicit assumption of a time horizon for which to optimize. The presence of irreversibility does not imply that you should not take any risk (after all, it is risky not to take risks). Instead, it means that you should acknowledge the non-ergodicity of the context in hand and take risks in a way that does not seriously impair your future if things go wrong. Prudence, when done right, is not just a way to minimize downside but also to enable upsides.

Exhibit 4: Cost of short-term optimization

Source: Book Ergodicity by Luca Dellanna, Ambit Asset Management

iii. Sustainability is a larger obstacle to optimizing short-term performance than talent

- Avoiding the risk of ruin is how you get ahead in the long run. It is not the best who succeed but the best of those who “survive” that succeed. Hence, sustainability is often a larger obstacle to optimizing short-term performance than talent. Few are willing to sacrifice their health, their reputation, their marriage, their capital, or anything that, once lost, is hard or impossible to get back. As a result, they make conservative choices. Are they really sacrificing returns by making these conservative choices, though? Or are they maximizing them?

As Morgan Housel wrote, “If your investment returns are in the 50th percentile every year, you will probably end up in the Top 5-10% over a 20-year period.” That is because most cannot sustain performance.

Exhibit 5: Long-term performance requires one always to be prepared for Black Swan events

Source: Ambit Asset Management

iv. The law of large numbers

- If you flip a coin, it will come out heads half of the time and tails the other half of the time. This is true if you flip it an infinite number of times. However, if you flip it ten times, the result may be six heads and four tails. The fewer the flips, the higher the chances that the tally differs from the expected 50%. However, the more coins flipped are tallied, the more the average of observed results converges to the expected value. This is called the law of large numbers.

- We assume the law of large numbers to be always relevant. It seldom is for individuals. It requires many trials. And in most real-life situations, we only have a limited number of them. For example, one cannot keep picking risky stocks until one gets lucky or rich – a few bad results in a row, and one could be broken.

- Whenever an activity cannot be assumed to be repeatable at infinity, we should be wary of expecting to achieve its average outcome. You can only rely on expected outcomes if you are guaranteed many repetitions. Otherwise, they are misleading. When permanent game overs are possible, do not rely on averages.

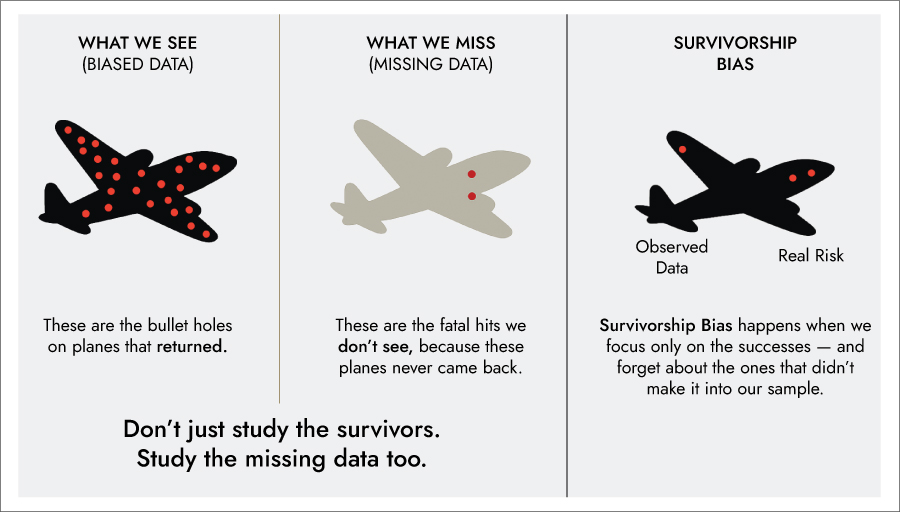

v. Survivorship Bias

- Too often when we look at a winner, we fail to see all his clones in the parallel universe in which he lost his bets. Any serious decision-making process cannot neglect them. Whenever we desire an outcome because we see those who have benefited from it, it is good to ask ourselves, do you want the outcome, or do you want the opportunity to take the gamble that produced the outcome? If you only want the former but not the latter, you might be unprepared for what is to come.

- Hence, it is pointless to envy someone with whom you would not trade places in a parallel universe. A quote on Elon Musk by Taleb – “Elon Musk illustrates the point made in Fooled by Randomness: solid financial success is largely the result of skills, hard work, and wisdom. But wild success is more likely to be the result of reckless betting, extreme luck, and the opposite of wisdom, folly.”

Exhibit 6: Example of Survivorship Bias

Source: Book Ergodicity by Luca Dellanna, Ambit Asset Management

3. Managing non-ergodicity – ergodicity as a non-binary concept

- Formally, ergodicity is a binary property. A system is either ergodic or not – nothing in between. The lifetime outcomes of its participants either coincide with its population outcome or they do not – nothing in between. In theory, this is a useful distinction. If you can choose between acting in an ergodic or non-ergodic context, choose the former. However, most practical contexts are non-ergodic. Work, sports, relationships, and real life are all non-ergodic. They all contain some degree of irreversibility.

- You cannot just refuse to engage in non-ergodic activities. It becomes then useful to expand the concept of ergodicity from black and white to a scale of shades. This way, we can access more practical considerations such as “how can I make my business more ergodic?”

- Ergodicity depends not only on the activity performed but also on your exposure to it. It means that if you limit your exposure to non-ergodicity, you can still participate in non-ergodic activities as if they were ergodic.

Examples:

- Instead of going all in on a single bet, take many independent bets.

- Do not trust advice about a non-ergodic context that assumes it is ergodic. While evaluating advice or next steps, always ask if it assumes ergodicity. If so, how would things change if we removed that assumption?

- Use protection for losses (insurance, equipment, options, etc.)

- Set aside some buffers and reserves.

Three strategies to manage non-ergodicity:

- The barbell strategy – avoid exposing all of yourself to a risk of ruin, no matter how small

- Skin in the game – ensure that the dangerous gets removed fast

- Redistribution – is good, even if one is above average (like buying insurance)

4. The Ludic Fallacy – spotting such cases in investing

Another important concept that the book discusses is the concept of “The Ludic Fallacy”. The Ludic Fallacy, as introduced by Nassim Taleb, is one of the most important ideas for understanding why investors, risk managers, and even entire financial systems repeatedly get blindsided by crises. It is essentially a misinterpretation of the world as a well-defined game — like chess or roulette — when, in reality, real-world systems are messy, complex, and full of hidden variables.

Nassim Taleb first introduced the concept of the ‘Ludic Fallacy.’ He made the following thought experiment: imagine that a coin falls ten times in a row on its ‘heads’ side. What is the chance of its falling ‘heads’ on the eleventh flip? Suppose one answers 50% because the flips are independent. In that case, one has committed the Ludic Fallacy – one has assumed that the rules describe the game correctly, failing to consider the possibility that the coin is biased or the flipper is a skilled swindler. The Ludic Fallacy occurs when we: Assume the rules of the game are fixed, complete, and known — when in reality, the game may be incomplete, manipulated, or fundamentally misunderstood. This is one more reason not to fixate on a binary interpretation of ergodicity.

Ludic Fallacy in Markets: Financial markets often appear to follow stable, mathematical rules — until they don’t. During bull markets or low-volatility regimes: i) Asset prices steadily rise; ii) Risk models (like Value at Risk) report low danger; iii) Strategies seem safe, consistent, and profitable. But this can be an illusion: i) Risks are not gone — they are hidden, dormant, or misclassified; ii) Everyone believes they are playing a predictable game, but the underlying rules are quietly changing; iii) When the regime shifts — like during 2008, March 2020, or the 2022 rate hikes — the “real game” reveals itself, and fragile strategies implode.

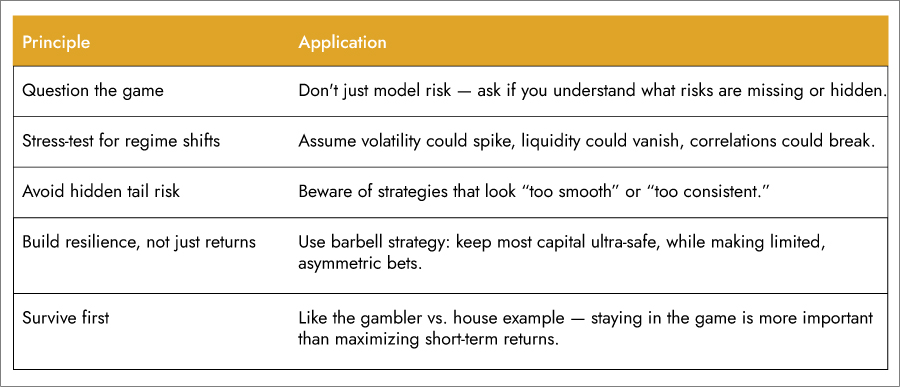

Exhibit 7: Practical investment lessons - to avoid falling victim to the Ludic Fallacy:

Source: Ambit Asset Management

Summary:

- Avoiding the risk of ruin is how you get ahead in the long term; hence, performance is subordinate to survival. Over the short term, consequences that extend beyond it do not matter. Over the long term, they do

- It is not the best who succeed, but rather the best of those who survive. Irreversibility absorbs future gains. Any form of game over nullifies future gains, bringing the average down.

- Formally, ergodicity is a binary property. A system is either ergodic or not – nothing in between. The lifetime outcomes of its participants either coincide with its population outcome or they do not – nothing in between. In theory, this is a useful distinction.

- One source of non-ergodicity is irrecoverable situations, also known as “game overs.” For example, bankruptcy, death, social ostracization and permanent injuries. It is natural, then, that the first of the three strategies to manage non-ergodicity is to reduce exposure to game overs. If you can choose between acting in an ergodic or non-ergodic context, choose the former.

- However, most practical contexts are non-ergodic. Work, sports, relationships, and real life are all non-ergodic. They all contain some degree of irreversibility.

- You cannot just refuse to engage in non-ergodic activities. It becomes then useful to expand the concept of ergodicity from black and white to a scale of shades. This way, we can access more practical considerations such as “how can I make my business more ergodic?”

- Ergodicity depends not only on the activity performed but also on your exposure to it. It means that if you limit your exposure to non-ergodicity, you can still participate in non-ergodic activities as if they were ergodic.

- The Ludic Fallacy may lead us to believe that some situations are ergodic when, in fact, they are not. This is one more reason not to fixate on a binary interpretation of ergodicity.

Ambit Coffee Can Portfolio

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and

consumption-oriented sectors. The Coffee Can philosophy has an unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced with disruptions at regular intervals. As the industry evolves or is faced with disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

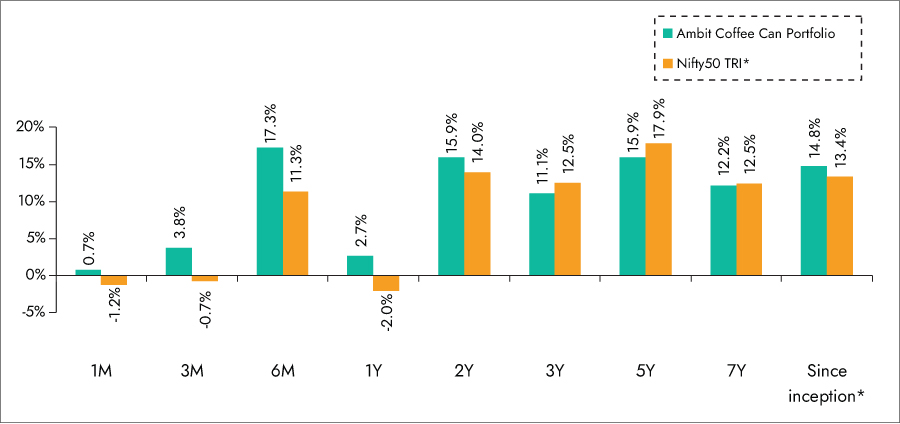

Exhibit 8: Ambit Coffee Can Portfolio point-to-point performance

Source: Ambit Coffee Can Portfolio inception date is Jun 20, 2017;

**1M Return: 1st - 31st Aug'25; 3M Return: 1st Jun'25 – 31st Aug'25; 6M Return: 1st Mar'25 – 31st Aug'25; 1Y Return: 1st Sept'24 – 31st Aug'25

*Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The performance related information provided herein is not verified by SEBI.

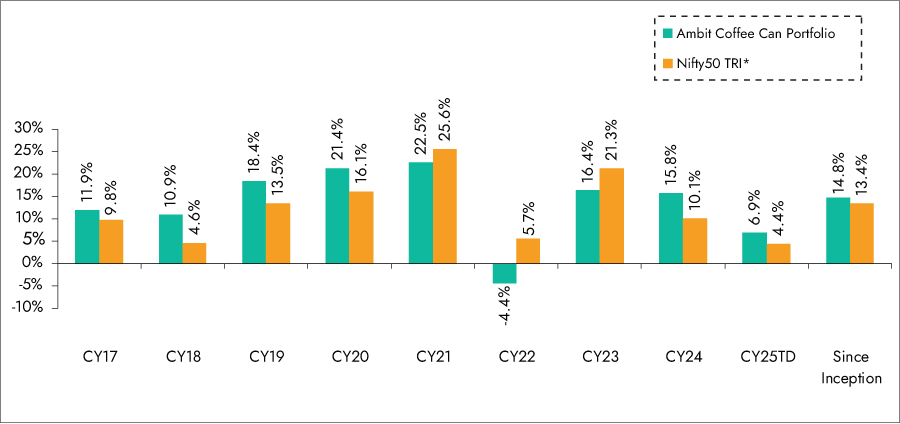

Exhibit 9: Ambit Coffee Can Portfolio calendar year performance

Source: Ambit Coffee Can Portfolio inception date is June 20, 2017;

*Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The performance related information provided herein is not verified by SEBI.

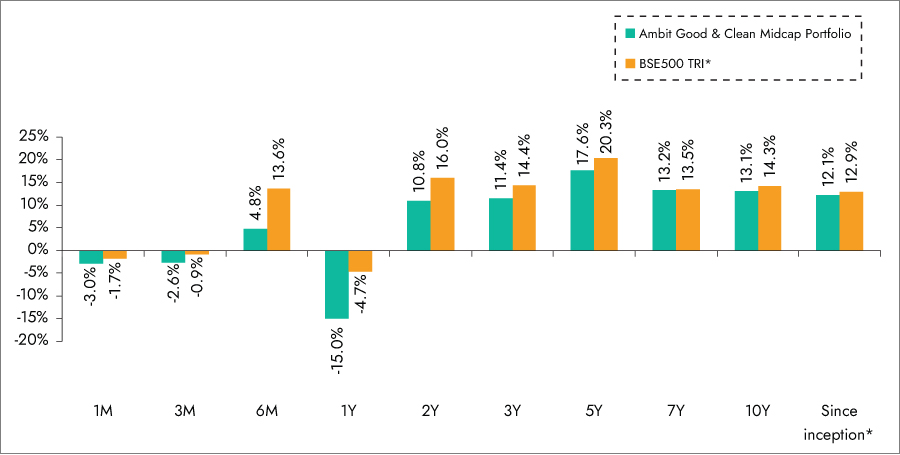

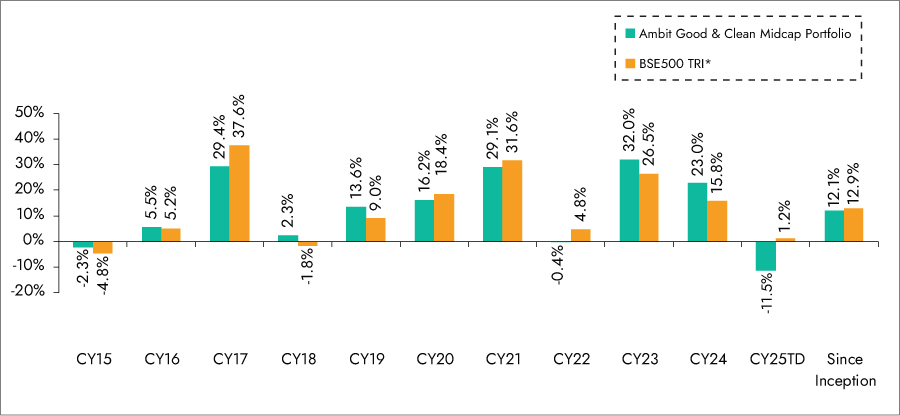

Ambit Good & Clean Midcap Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

1. Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

2. Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longerwith annual churn not exceeding20-25% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with these compounding earnings acting as the primary driver of investment returns over long periods.

3. Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

Exhibit 10: Ambit Good & Clean Midcap Portfolio point-to-point performance

Source: Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015;

**1M Return: 1st - 31st Aug'25; 3M Return: 1st Jun'25 – 31st Aug'25; 6M Return: 1st Mar'25 – 31st Aug'25; 1Y Return: 1st Sept'24 – 31st Aug'25

*BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Mid cap. The performance related information provided herein is not verified by SEBI.

Exhibit 11: Ambit Good & Clean Midcap Portfolio calendar year performance

Source:Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015;

*BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Mid cap. The performance related information provided herein is not verified by SEBI.

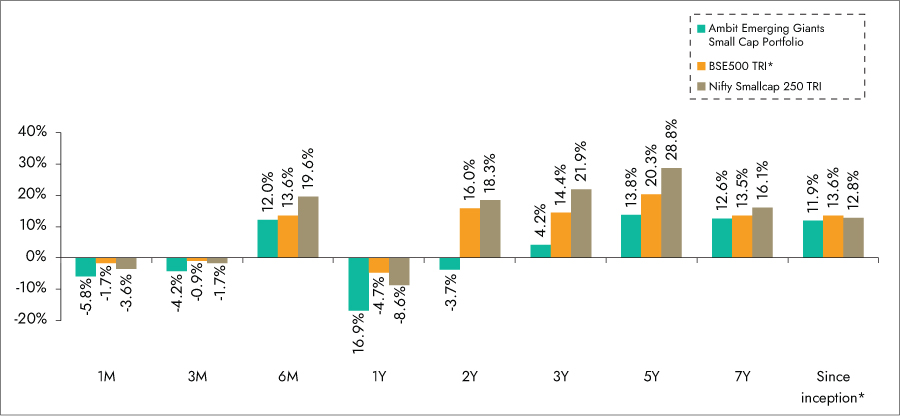

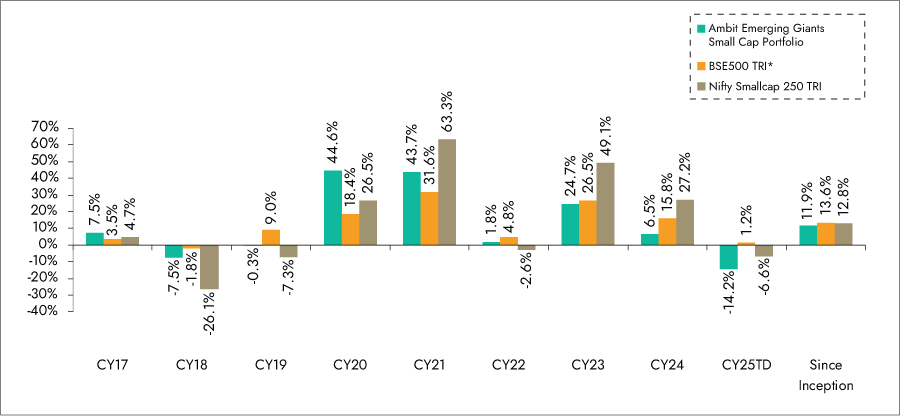

Ambit Emerging Giants Small Cap Portfolio

Small caps with secular growth, superior return ratios and no leverage – Ambit's Emerging Giants Small Cap portfolio aims to invest in small-cap companies with market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than INR 10,000cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt), and the ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence led us to a concentrated portfolio of 18-20 emerging giants.

Exhibit 12: Ambit Emerging Giants Small Cap Portfolio point-to-point performance

Source: Ambit Emerging Giants Small cap Portfolio inception date is Dec 1, 2017;

***1M Return: 1st - 31st Aug'25; 3M Return: 1st Jun'25 – 31st Aug'25; 6M Return: 1st Mar'25 – 31st Aug'25; 1Y Return: 1st Sept'24 – 31st Aug'25

**BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants Small cap. The performance related information provided herein is not verified bySEBI.

*Nifty Smallcap 250 TRI is the secondary benchmark, being provided solely for additional reference and comparison. For details refer disclaimer clause.

Exhibit 13: Ambit Emerging Giants Small Cap Portfolio calendar year performance

Source: Ambit Emerging Giants Small cap Portfolio inception date is Dec 1, 2017;

*BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants Small cap. The performance related information provided herein is not verified bySEBI.

**Nifty Smallcap 250 TRI is the secondary benchmark, being provided solely for additional reference and comparison. For details refer disclaimer clause.

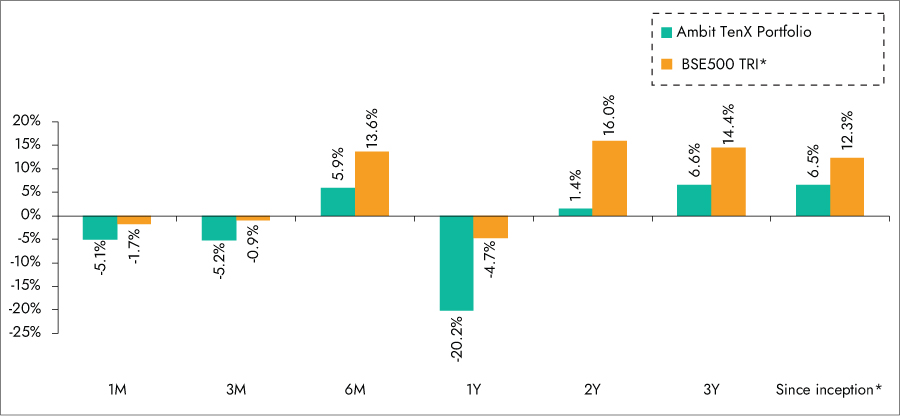

Ambit TenX Portfolio

Ambit TenX Portfolio gives investors an opportunity to participate in the India growth story as the Indian GDP heads towards a US$10tn mark over the next 12-15 years. Mid and Small corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that have the potential to multifold earnings.

Key features of this portfolio would be as follows:

1. Longer-term approach with a concentrated portfolio: Ideal investment duration of >5 year with 15-20 stocks.

2. Key driving factors: Low penetration, strong leadership, light balance sheet.

3. Forward-looking approach: Relying less on historical performance and more on future potential while not deviating away from the Good & Clean philosophy.

Exhibit 14: Ambit TenX Portfolio point-to-point performance

Source: Ambit TenX Portfolio inception date is Dec 13, 2021;

**1M Return: 1st - 31st Aug'25; 3M Return: 1st Jun'25 – 31st Aug'25; 6M Return: 1st Mar'25 – 31st Aug'25; 1Y Return: 1st Sept'24 – 31st Aug'25

*BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio. The performance related information provided herein is not verified by SEBI.

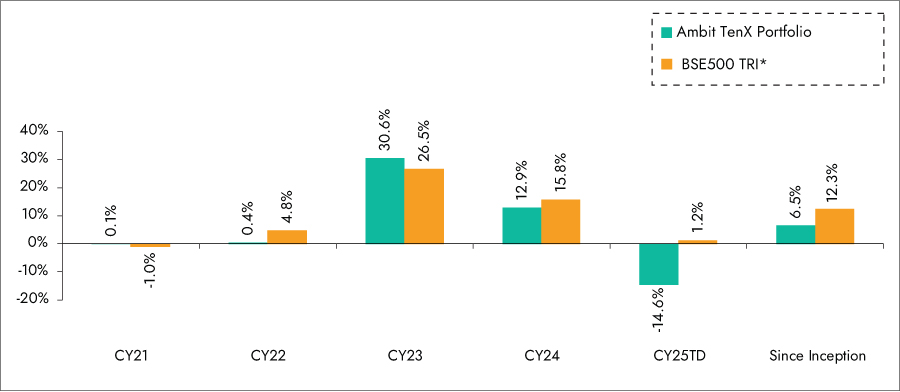

Exhibit 15: Ambit TenX Portfolio calendar year performance

Source: Ambit TenX Portfolio inception date is Dec 13, 2021;

*BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio. The performance related information provided herein is not verified by SEBI.

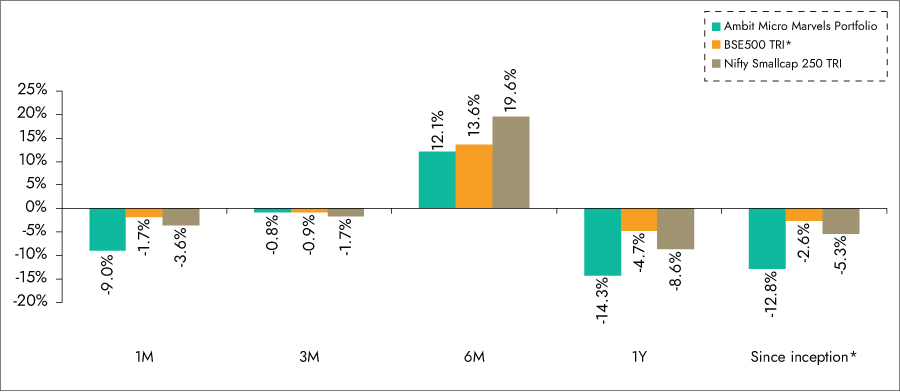

Ambit Micro Marvels Portfolio

We aim to create a portfolio that invests predominantly in micro-cap companies with the potential of delivering superior earnings growth and generating relatively better risk-adjusted performance over a long period of time.

Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts while our proprietary ‘greatness’ framework helps identify efficient capital allocators. The result is a concentrated portfolio of 20-25 stocks that draws down less than the market in corrections and has low churn.

Key Features of Portfolio Companies:

1. High earnings growth companies with low leverage,

2. Market leaders or challengers with strong moat around brand, distribution, technology, and innovation,

3. Strong corporate governance coupled with apt capital allocation.

Exhibit 16: Ambit Micro Marvels Portfolio point-to-point performance

Source: Ambit Micro Marvels Portfolio inception date is Jul 29, 2024;

***1M Return: 1st - 31st Aug'25; 3M Return: 1st Jun'25 – 31st Aug'25; 6M Return: 1st Mar'25 – 31st Aug'25; 1Y Return: 1st Sept'24 – 31st Aug'25

**BSE 500 TRI is the selected benchmark for the Ambit Micro Marvels Portfolio. The performance related information provided herein is not verified by SEBI.

*Nifty Smallcap 250 TRI is the secondary benchmark, being provided solely for additional reference and comparison. For details refer disclaimer clause.

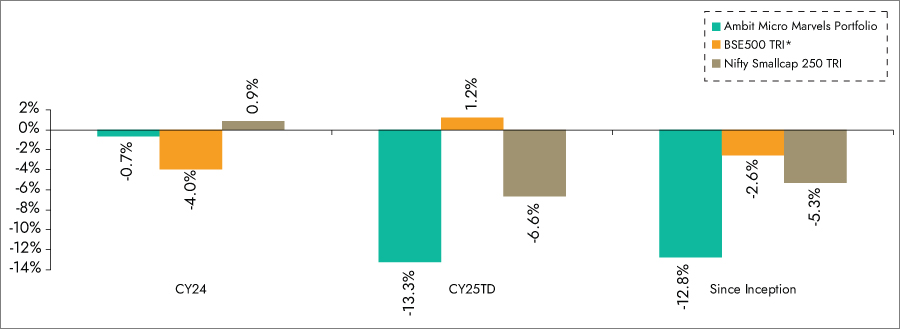

Exhibit 17: Ambit Micro Marvels Portfolio calendar year performance

Source: Ambit Micro Marvels Portfolio inception date is Jul 29, 2024;

**BSE 500 TRI is the selected benchmark for the Ambit Micro Marvels Portfolio. The performance related information provided herein is not verified by SEBI.

*Nifty Smallcap 250 TRI is the secondary benchmark, being provided solely for additional reference and comparison. For details refer disclaimer clause.