1766033653347.jpg)

Understanding the Indian pharma value chain

The key players in the pharma supply chain are the Manufacturers, C&F agents, Distributors and Retailers. These players collectively form a complex and interconnected network that serves the pharmaceutical supply chain form manufacturing to the last-mile connectivity:

1. Manufacturer – The process starts with manufacturer that produces finished products at their facilities and faces the challenge of dealing with multiple subscale distributors and limited visibility of secondary data.

2. Carry Forward (C&F) Agents – Next, carry forward (C&F) agents step in, providing storage, handling supply orders, and managing receivables from distributors as finished product consignments arrive.

3. Distributors – Distributors then act as the key link, covering large geographical regions, one or more states or cities; responsible for supplying healthcare products to retail pharmacies and hospital customers.

4. Retailers/ Hospitals/Physicians – Retailers, including large national chains and traditional local pharmacies, represent the final point of supply, with retail pharmacies accounting for the majority of demand (80-85%), followed by hospitals (12-15%) and physicians (3-5%). Pharma value chain in India unlike in developed markets is highly fragmented given (a) ~5,000 C&F agents, (b) ~65,000 distributors and (c) ~900,000 retailers. This over the next decade is likely to go through significant consolidation as witnessed in sectors like airlines, telecom, cement, banking and healthcare.

Exhibit 1: Pharmaceutical supply chain in India is highly fragmented

1766033950998.jpg)

Source: Company, Ambit Asset Management

1763792132350.jpg)

Exhibit 2: ~48% of Keimed’s revenue comes from Apollo Hospitals

1763792175697.jpg)

Source: Company, Ambit Asset Management

90-95% of the market, while in Germany, their share is even higher at 95-97%. Due to the following reasons:

1. Tight regulations

2. Slow growth in the mature markets

3. Low margin nature of the business

4. Intense competition and well capitalized players

India is expected to follow a similar trajectory, with the share of large, organized distributors projected to grow to ~20-30% by FY28P

1763792397239.jpg)

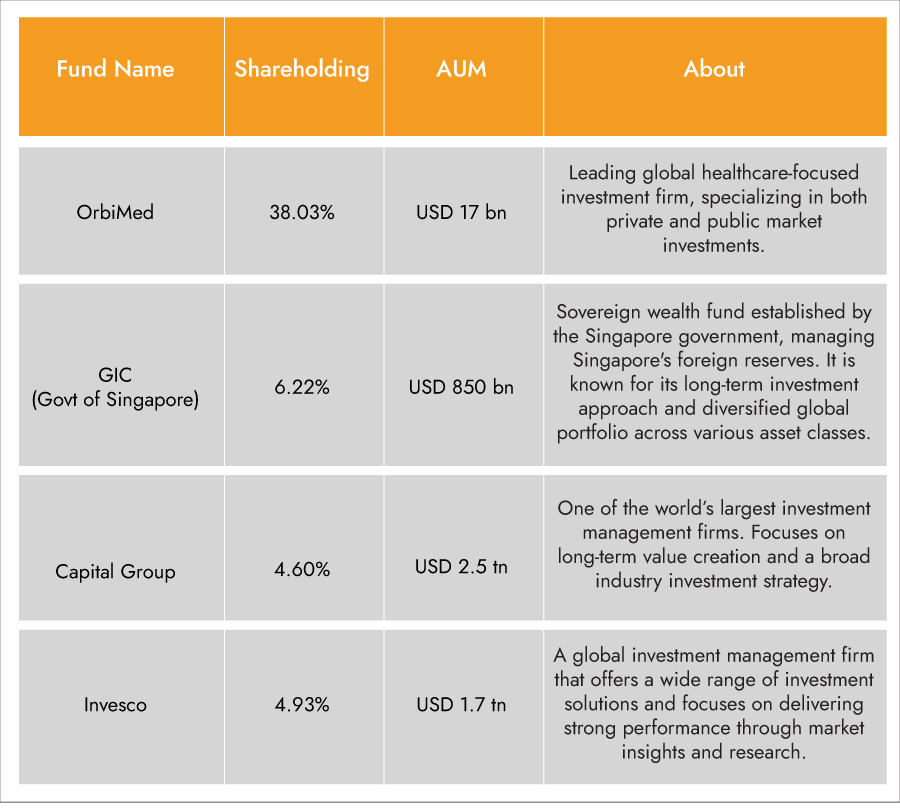

Founded in 2018, Entero has swiftly established itself as one of India’s top three healthcare distributors. The company was founded by industry veterans Mr. Prabhat Agrawal (formerly of Alkem Labs) and Mr Prem Sethi (formerly of IQVIA), with a leadership team that includes a CFO with extensive experience from API Holdings (Pharmeasy) and the Apollo Group. Entero is backed by OrbiMed Asia, a global investment firm holding a 38% stake, known for its long-term investments in the healthcare sector. Driven by a clear vision to build an organized, technology-driven, and integrated healthcare distribution platform, Entero aims to add value across the entire healthcare ecosystem. Operating on a B2B model, the company distributes healthcare products to a wide range of customers, including retail pharmacies, hospitals, and clinics across India.

With a strong presence in South India, where over 60% of its revenue is generated, Entero operates a comprehensive infrastructure of 95+ warehouses, covering over 485 districts. The company serves more than 79,500 retailers and 3,100 hospitals, and works with over 2,300 healthcare product manufacturers, offering access to more than 71,000 SKUs. This vast network ensures superior fill rates and strengthens Entero’s position as a dominant force in India’s evolving healthcare distribution landscape.

1766036607910.jpg)

Limited competition given the oligopolistic market

Keimed and API Holdings are Entero’s main competitors in the Indian organized healthcare distribution space: Keimed Pvt Ltd is one of India’s largest pharmaceutical distributors, serving over 70,000 pharmacies nationwide since 2000. With a network of 300+ manufacturers and more than 45,000 products, Keimed operates 86 distribution centers across India. It is a key supplier to Apollo Hospitals and Apollo Pharmacy, fulfilling about 50% of their pharmaceutical needs.

Exhibit 2: ~48% of Keimed’s revenue comes from Apollo Hospitals

1763792649515.jpg)

Source: Company, Ambit Asset Management

API Holdings plays a pivotal role in India’s pharmaceutical distribution landscape through its subsidiaries, Aknamed and Ascent Wellness. Aknamed is India’s largest hospital-focused supply chain platform, ensuring the efficient delivery of healthcare products to hospitals nationwide. Ascent Wellness operates a full-stack distribution model that encompasses warehousing, logistics, supplies, and credit, seamlessly connecting leading pharmaceutical companies to over 25,000 pharmacies. With an annual GMV surpassing $300 million, Ascent has experienced robust growth, fueled by both organic expansion and strategic acquisitions. These subsidiaries significantly bolster API Holdings market position, enhancing its comprehensive service offerings and reinforcing its leadership in the pharmaceutical distribution sector.

1763792888384.jpg)

1766036828271.jpg)

An overview of Entero Healthcare Solutions Ltd

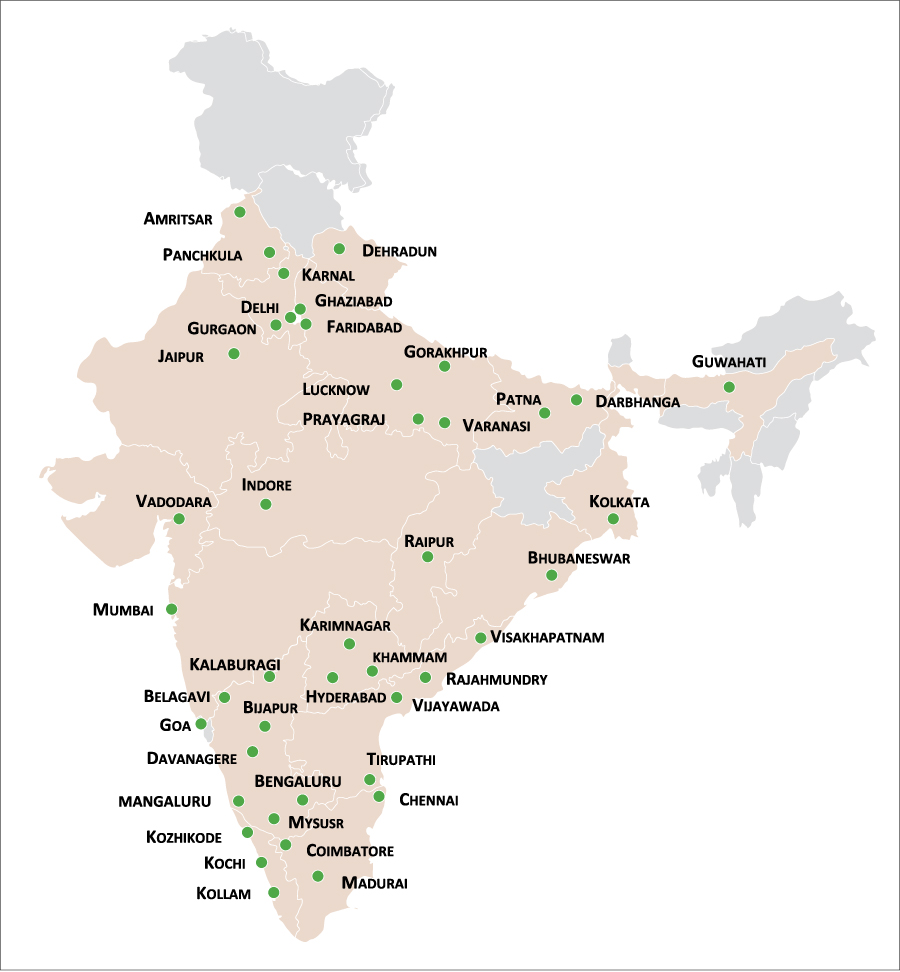

Exhibit 3A: Robust distribution network covering 43+ cities in 20+ states

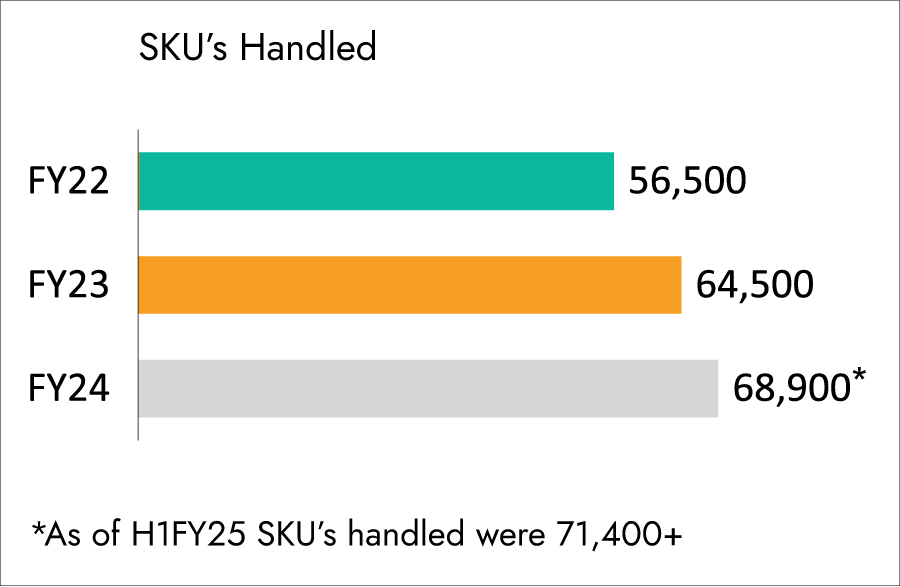

Exhibit 3B: Catalogue of over 68,900 SKUs in FY24

1766037247774.jpg)

Source: Company, Ambit Asset Management

1766038597321.jpg)

Aggressive acquisition and integration strategy

Entero’s strategic and aggressive acquisition approach has enabled it to rapidly become one of India’s top three pharma distribution players within just six years. The company focuses on acquisitions that expand its product portfolio and enhances geographical reach, targeting distributors at attractive valuations of 0.25-0.40x sales or 3-8x EV/EBITDA multiples. Post-acquisition, Entero efficiently integrates acquired distributors, retaining around 50% of the original owners while smoothly transitioning the rest. This strategy has not only strengthened Entero’s market position but also delivered substantial gains in operational efficiency and profitability, as demonstrated in Exhibit 4.

Exhibit 4: Entero’s acquisitions (subsidiaries) have witnessed strong revenue growth post acquisition

1766038681537.jpg)

Source: Ambit Asset Management

Exhibit 5: Channel checks indicated consolidation is imminent

1766038768421.jpg)

Source: Channel check, Ambit Asset Management

1766039195677.jpg)

The following are various platforms/tools to provide one stop solutions

The following are various platforms/tools to provide one stop solutions:

Entero Direct: A cloud-based SaaS platform that streamlines procurement for retailers, enabling order placement, shipment tracking, and payment management via smartphones or computers.

Integrated with Entero’s delivery fleet, it offers real-time status updates, enhancing supply chain visibility and efficiency.

Entero CRM: A customer relationship management tool that tracks behavior and preferences to optimize interactions, helping Entero enhance retention and tailor services for stronger long-term relationships.

Entero ERP: A cloud-based ERP system that integrates data across locations, providing control over product and customer information. With advanced security, it streamlines processes and boosts operational efficiency while minimizing data loss.

Exhibit 6: Single-interface platform for pharmacies to ease the ordering process

1766039257288.jpg)

Source: Company, Ambit Asset Management

Teqtic: Entero’s data warehouse and analytics platform uses customer transactional data to generate customized reports and insights, providing real-time performance analysis while ensuring data privacy with identity-based access control.

Healthedge: A platform that simplifies supply chain management for retailers, enabling them to focus on healthcare professionals and patients. Currently piloting in Bombay, Entero aims to supply 70% of retailer needs and convert 10% of retailers to this model within three years to drive growth.

1766039594223.jpg)

1766039623769.jpg)

1766040000354.jpg)

Exhibit 7: A little background of the Marquee investors (as of Dec-2024)

Source: Company, Ambit Asset Management

1766040212590.jpg)

Entero is exploring new revenue streams, including Group/Centralized Purchase Orders (GPO/CPO) to manage hospital supply chains, potentially adding Rs 1 crore per month from a single hospital. Currently managing this for a hospital in Lucknow, further expansion will drive growth. Additionally, Entero is pursuing partnerships with quick commerce platforms for OTC product distribution, diversifying revenue and strengthening its market position.

Exhibit 8: Entero aims for a 1.5-2x times organic growth vis-a-vis IPM growth of ~9%.

1766040241998.jpg)

Source: Company, Ambit Asset Management

Exhibit 9: The TAM is expected to grow at a CAGR of ~10-11% over FY23-FY28P, with top 3 organized players to benefit from consolidation

1766040343641.jpg)

Source: Company, Ambit Asset Management

1766040714574.jpg)

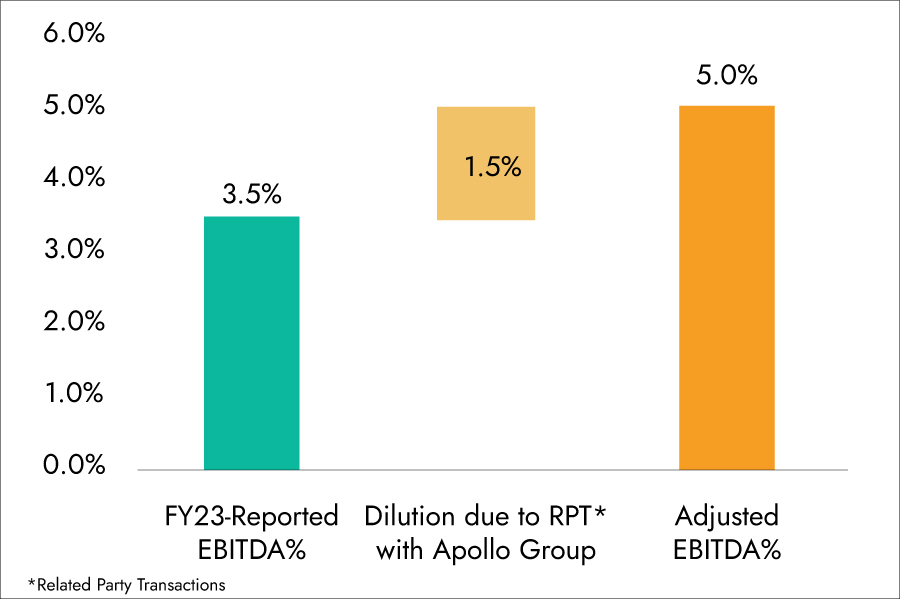

Entero is well-positioned for structural margin expansion. Keimed Ltd, India’s largest pharma distributor with over 5% market share, is a key supplier to Apollo Hospitals and Apollo Pharmacy, reporting an EBITDA margin of around 3.5% in FY23. Apollo management notes that Keimed passes 1-1.5% of this margin to Apollo Pharmacy, implying an adjusted margin of 4.5-5%. Unlike Keimed, Entero is not exposed to customer concentration risks, allowing it to capitalize on strong operating leverage and cost efficiencies. Keimed's performance highlights that high EBITDA margins are attainable in pharma distribution, and Entero is on track to narrow this margin gap through strategic execution and scalability.

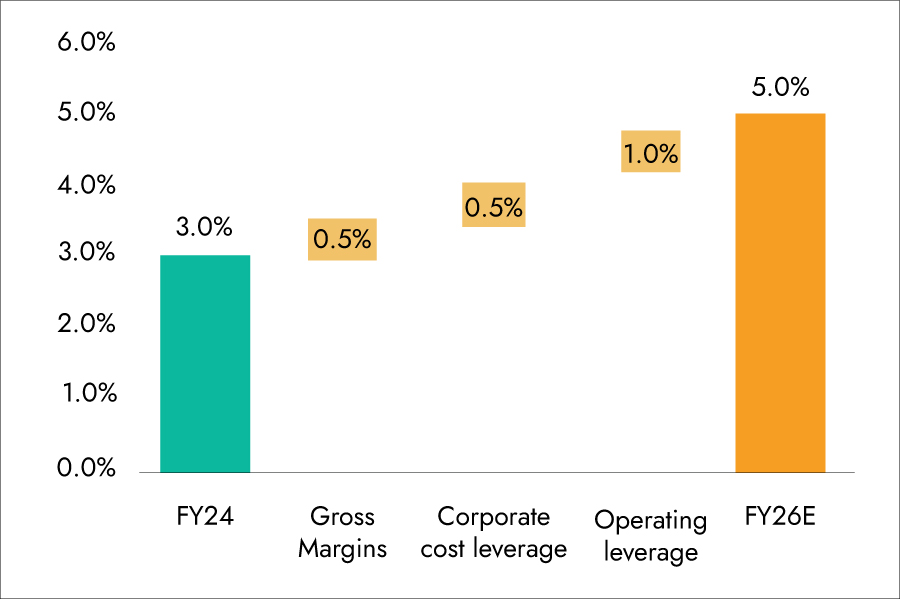

Exhibit 10A: Keimed’s impact of ~150 bps on EBITDA margins due to customer concentration

Exhibit 10B: Entero’s levers for EBITDA margins build up

Source: Ambit Asset Management

Entero’s expanding surgical equipment and devices segment is poised to drive significant margin expansion. While this segment currently contributes minimally to revenue, it represents one-third of the Indian Pharma market's distribution space and is expected to grow substantially, enhancing profitability. Additionally, the sale of private-label products-offering gross margins up to 2.5 times higher than standard pharma products-will further boost margins. Entero’s increasing scale also positions it to benefit from procurement efficiencies, unlocking volume discounts and incentives. This enhanced bargaining power, driven by economies of scale, will play a critical role in improving margins and strengthening the company’s financial position.

1766040858875.jpg)