.jpg)

Likewise, the broader BSE 500 stocks are also showing weakness in earnings, with ~168 companies reporting EPS decline in 2QFY26 vs ~101 companies reporting earnings decline over FY22-25. Resultantly, whilst the BSE 500 index has delivered a 13% return YTD; 1/3rd of stocks within the index are down >-12%.

Lastly, whilst the Nifty Microcap 250 index has appreciated by 12% YTD, it is not representative of the broader markets as more than a third of the stocks have shown negative returns.

However, there is a silver lining ahead, as there is an expectation of a recovery in earnings in 2H led by (a) a revival in consumer demand thanks to the cut in GST announced recently, (b) a pick-up in Government and private capex led by recent rate cuts announced by the RBI and several measures taken to fuel credit growth, and (c) the base effect given lower GDP growth of 6.3% in 2HFY25 vs 6.7% in 1HFY25.

We expect markets to recover from this earnings growth and urge investors to use the current weakness in broader markets to their advantage by increasing their equity allocation.

Ambit Coffee Can Portfolio

Ambit Coffee Can Portfolio delivered a 11.2% YTD underperforming the benchmark Nifty 50 Index by 130bps. On the earnings front, the strategy delivered a revenue/EBITDA/PAT growth of 17%/25%/15% on a YoY basis in 2QFY26 vs 1%/11%/7% for Nifty 50 companies. The earnings growth was led by Hitachi Energy India Limited, Ultra Tech Cement Limited and Bharti Airtel Limited companies which delivered an impressive YoY PAT growth of 247%/121%/67% respectively. The detractors to the portfolio were Inter Globe Aviation Limited/Zydus Wellness Limited/Eternal Limited delivering YoY PAT growth of -106%/-296%/-538% respectively.

1765449719400.jpg)

**Revenue and EBITDA calculations are ex-BFSI.

*PAT is calculated excluding Other Income and Exceptional Items, although in BFSI, other income is considered for calculation purposes.

*Calculation is as per the simple average of absolute revenue/EBITDA/PAT for all companies.

Source: Ambit Asset Management

Top 3 and Bottom 3 Performers:

1765449732097.jpg)

Source: Ambit Asset Management

Hitachi Energy India Limited

- Hitachi Energy India (HEI) reported results ahead of consensus estimates with revenue/EBITDA/APAT of +5.7%/+45.4%/+69.6%, respectively.

- The EBITDA margin was a positive surprise at 16.3%, driven by operating leverage and cost optimization.

- HEI's annualized below-EBITDA-line costs are ~1,000bps higher than peers, primarily driven by ~450bps higher royalty and other expenses.

- HEI has ~INR 294.1 bn of Order Book as of Sept’25, of which INR 100bn are base orders. With volume growth, we expect the positive margin trajectory to be maintained.

Ultratech Cement Limited

- Ultratech’s standalone (ex-ICEM, UAE) EBITDA of Rs 27.7 bn (+43% YoY, -34% QoQ) was below estimates, led by higher costs. Volumes of 29.6 mn tons grew 9.6% YoY on a like-for-like (LFL) basis and were broadly in line, while blended realizations increased 1.5% QoQ (+2.4% YoY).

- Cost/ton increased 9.1% QoQ (-1.2% YoY), due to a combination of kiln shutdown costs (~Rs 80-100/ton), higher advertising costs (~Rs 50/ton), variable employee costs (Rs 25/ton), higher pet coke prices, and QoQ operating deleverage. Blended margins stood at Rs 935/ton.

- Near-term price hikes appear unlikely, given GST pass-through optics. We expect demand to pick up after the festive season and margins to recover through operating leverage.

Bharti Airtel Limited

- Bharti Airtel posted a better-than-expected Q2FY26 performance with revenue coming in at INR 528.7 bn (+5.8% QoQ), supported by ARPU improvement to INR 256 (+2.2% QoQ) and 1.4mn QoQ net subscriber additions. EBITDA margin improved by 56bp QoQ to 57.3%.

- Despite higher capex of INR 114 bn (INR 83bn in Q1FY26), FCF remained solid at INR 186 bn (INR 199 bn in Q4FY25).

- Bharti’s industry-leading ARPU, steady subscriber additions, and robust FCF continue to bolster its balance sheet.

Source: Ambit Asset Management

InterGlobe Aviation Limited

- IndiGo’s 2QFY26 revenue at Rs 195 bn grew 9% YoY. ASKs (Available Seat Kilometers) grew 8% YoY. However, PLFs (Passenger Load Factors) were flat at 82.5%. Yields at Rs 4.69 increased 3% YoY. Aircraft fuel expenses were reduced by ~10% YoY, albeit offset by higher FX losses. FX losses at Rs 28 bn were high due to ~6% USD/INR depreciation.

- This led to muted EBITDARM/EBITDAM in 2QFY26 at 6%/3%. That said, EBITDARM ex-FX loss was 20.5% in 2QFY26 vs 15.7% in 2QFY25.

- Capacity addition on international routes will create a natural hedge against FX. IndiGo retains top market share with 64.3% in 2QFY26. Management guided for mid-double-digit ASK growth in FY26.

Zydus Wellness Limited

- Zydus witnessed a soft 1H26 as unseasonal rain weighed on its summer-centric brands like Glucon-D and Nycil.

- The foray into the high-growth healthy snacking category through the acquisition of the Ritebite Max Protein brand augurs well for medium-term growth momentum.

- Further, the acquisition of CCL provides an additional growth level and aids in normalizing the seasonality impact of the summer portfolio.

- Management is focused on multi-category, multi-channel, and multi-geography expansion and is targeting EBITDA margins of 17-18% over the next two years.

Eternal Limited

- Eternal reported 2QFY26 net revenue of INR 135b (+90% QoQ / +183% YoY). This high growth is mainly on account of a shift to inventory ownership in quick commerce (Q-commerce).

- FD continues to underperform expectations, with no clear inflection yet. Growth remains muted due to a share shift toward Q-commerce and muted discretionary demand in H1FY26.

- Losses in the going-out vertical are expected to remain range-bound at ~INR 600m per quarter, as per management commentary. No material change in trajectory is expected in the near term. The company continues to prioritize Blinkit’s scale-up and efficiency initiatives over profit milestones across smaller adjacencies.

We expect the earnings growth of the strategy in H2FY26, to be led by (a) a revival in consumer demand, (b) a pick-up in Government and private capex, and (c) key portfolio changes.

On valuations, the portfolio is attractively valued at 34x FY27 PE despite a 22% EPS CAGR over FY25-27 and an ROE of 22% in FY27. Relative to the Nifty, the portfolio trades at a 75% premium given superior earnings growth and ROE.

Ambit Good & Clean Midcap Portfolio

Ambit Good and Clean has underperformed YTD; portfolio changes made in the last 2 months are beginning to work.

The portfolio delivered a 7.4% return, underperforming the Nifty Midcap 150 Index by 800bps.

On the earnings front, the strategy delivered Revenue/EBITDA/PAT growth of 16%/34%/-1% on a YoY basis in 2QFY26 vs 3%/ 16%/14% for benchmark-based companies. The earnings growth was led by One 97 Communications Limited, Lupin Limited, and TVS Motor Company Limited, which delivered impressive YoY PAT growth of 98%, 71%, and 46% respectively. The detractors to the portfolio were Deepak Nitrite, Axis Bank, and Supreme Industries, with the companies delivering YoY PAT growth of -46%, -26%, and -22% respectively.

**Revenue and EBITDA calculations are ex-BFSI.

*PAT is calculated excluding Other Income and Exceptional Items, although in BFSI, other income is considered for calculation purposes.

*Calculation is as per the simple average of absolute revenue/EBITDA/PAT for all companies.

Source: Ambit Asset Management

Top 3 and Bottom 3 Performers:

Source: Ambit Asset Management

TVS Motor Company Limited

- Revenue grew 29% YoY to Rs 119.05 bn, above estimates.

- Volume grew 23% to 1.51m units and Realizations grew 5% (largely driven by a favorable mix of exports, EVs, and a lower share of mopeds).

- Market share gain has been demonstrated consistently across segments; PAT growth of 37% is a reflection of operating leverage.

Lupin Limited

- Revenue, EBITDA, and PAT were up 24%, 63%, and 73% YoY, beating street expectations due to strong performance in the US and other markets with controlled costs, leading to EBITDA margins expanding to ~33.2%.

- The US has been a key driver of growth with sales of US$315m, the highest since 3QFY17.

- Guiding ~ US$1 bn+ revenue in the US in FY26 on the back of new launches, strong performance of Tolvaptan, Spiriva, etc., coupled with an upgraded FY26E EBITDA margin guidance to 25–26% (from 24–25%).

One 97 Communications Limited

- Solid growth with revenue up 24% YoY and GMV up 27%, with strong operating performance.

- Adj. EBITDA margin was healthy at ~8% (Rs 1.8 bn); the contribution margin eased slightly to 59%; PAT was hit by a Rs 1.9 bn gaming-JV loan write-off.

- New businesses are scaling well, with Wealth, lending, and international segments gaining traction, supporting the medium-term growth and margin expansion outlook.

Source: Ambit Asset Management

Deepak Nitrite Limited

- Weak performance across segments due to US tariff actions, Chinese dumping (mainly in sodium nitrite, DASDA, and nitro-aromatics), and weak agrochemical exports continues to distort trade flows.

- Major nitration, hydrogenation, nitric acid, MIBK (Methyl Isobutyl Ketone )/MIBC (Methyl Isobutyl Carbinol), and multi-purpose plant assets are expected to be commercialized in FY26–Q1FY27, which will support future growth.

- Management remains cautiously optimistic and expects H2FY26 to be better than Q2FY26, aided by an improvement in market sentiment and project commissioning.

Axis Bank Limited

- Growth & Margins - Stable: Loan growth was strong at 5% QoQ (corporate-led), and NIM held better than expected (down only 7 bps), but core profitability weakened with core PPOP down 2% QoQ.

- Asset Quality - Negative: Slippages improved significantly (total down to 2.1% from 3.1%), but credit costs remained elevated at 1.3%—the highest among large banks—due to RBI-mandated one-time provisions on discontinued crop-loan variants.

- Profitability Impact - Negative: Higher Opex (PSLC [Priority Sector Lending Certificates] purchases) and elevated provisions drove PAT down 12% QoQ and RoA down to 1.2% from 1.5%, resulting in an overall mixed performance.

Supreme Industries Limited

- Supreme Industries reported a muted 2QFY26 with Revenue/EBITDA/PAT growth of 5%/ -7%/-20% YoY.

- Overall volume grew 12% YoY (+10% organically, excluding 3,000 MT of Wavin volumes) vs. our estimate of 10%. Piping business growth for agricultural applications was impacted by the early onset of the monsoon.

- Prolonged rainfall further weighed on demand, leading to a decline in plastic piping volumes for the agriculture segment.

The renewed strategy on Ambit Good and Clean Midcap Portfolio centers on four distinct themes designed to capture alpha through market mispricing, long-term secular growth, aggressive earnings momentum, and strong business fundamentals.

1. Market Underestimation (Value and Growth Arbitrage): Businesses currently under-appreciated by the market either in terms of future growth potential or intrinsic valuation, offering a compelling margin of safety and significant upside. Our idea is to capitalize on temporary market pessimism or slow re-rating cycles for fundamentally sound companies.

Investment Ideas:

- Manappuram Finance: Identifying a potential value opportunity in the NBFC space, especially if the core gold loan business or microfinance segments show resilient performance despite broader regulatory/economic concerns.

- State Bank of India (SBI): Targeting a potential re-rating opportunity for a large public sector bank, driven by improving asset quality, credit growth, and continued market share gains in a robust financial sector environment.

2. Cyclical Upswing: Allocating capital to sectors or businesses where growth is anticipated to accelerate significantly, often due to government policy, new industry tailwinds, or a multi-year capex upcycle. The idea is to secure an early entry into businesses positioned to be primary beneficiaries of structural, large-scale national spending plans.

Investment Ideas:

- BHEL (Bharat Heavy Electricals Ltd): Positioning for a cyclical upturn in the power sector and industrial capex, benefiting from a potential revival in thermal power or increased orders in non-power segments like defense and railways.

- Bharat Electronics (BEL) (Aerial Defense): A direct play on the aerial defense and electronics indigenization trend, with high order book visibility driven by government priority and increased defense spending.

3. Aggressive Earnings Growth & Evolving Businesses: We focus on high-growth companies experiencing aggressive earnings growth by successfully leveraging changing business dynamics and technology shifts within their industries. The idea is to generate alpha associated with successful business model evolution and rapid scaling in dynamic markets.

Investment Ideas:

- Paytm (One97 Communications): Include here for its aggressive revenue and profitability trajectory driven by the digitization of financial services and merchant ecosystem expansion.

- MCX (Multi Commodity Exchange of India): A business evolving through technology (new trading platform) and benefiting from increased market sophistication and liquidity, which can lead to disproportionate growth in transaction volumes and earnings.

4. Bottom-up Strong Fundamentals (Quality and Resilience): A bottom-up stock selection approach that identifies high-quality companies with proven business models, strong management, and resilient financial profiles, irrespective of broader macro themes.

Investment Ideas:

- City Union Bank: A bottom-up pick in the private sector banking space, characterized by regional dominance and robust risk management.

- Asahi India Glass: A market leader in the automotive and architectural glass segment, benefiting from a cyclical upswing in the auto industry and a strong focus on margin improvement and high-end products.

- Aditya Birla Capital: A play on the financial conglomerate theme, leveraging the cross-selling synergies across insurance, asset management, and NBFC businesses.

We expect the earnings growth of the strategy to bounce back in 2H driven by an uptick in credit growth that affects Financials. b) Better volumes in auto and ancillary companies as GST benefits set in. c) Stronger execution in Industrials is leading to higher profits in H2.

On valuations, the portfolio is attractively valued at a 24x FY27 PE despite a 19% EPS CAGR over FY25-27 and an ROE of 17% in FY27. Relative to the Nifty Midcap, the portfolio trades at an ~8% discount despite superior earnings growth and ROE.

Ambit Micro Marvels Portfolio

Ambit Micro Marvels delivered an 8.7% YTD return, underperforming the Nifty Microcap 250 by 770 bps. On Fundamentals of the Ambit Micro Marvels Portfolio, continue to remain strong. 2QFY26 PAT growth of 13% YoY stands superior to peers in a similar market cap bucket. We believe that there is no index that represents our Micro Marvels universe. The reason for this is that whilst the average market cap for Micro Marvels is ~Rs 20 bn, it is ~Rs 178 bn for the Nifty Small Cap 250 and ~Rs 73 bn for the Nifty Microcap 250 index.

Exhibit 1: The average market cap of MM is much lower than the Nifty Small Cap 250 and Nifty Micro-Cap 250 indices

1765447529902.jpg)

Source: Ambit Asset Management

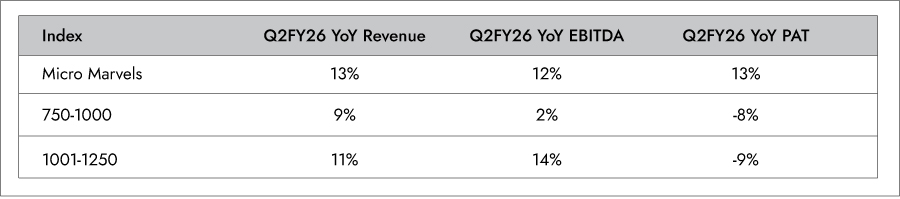

Resultantly, we believe that comparing the earnings growth of the MM strategy with either of the indices is not an apples-to-apples comparison. To do a peer comparison, we computed the PAT growth for the 750-1000 companies ranked by market cap, which have an average market cap of Rs 39 bn, and for the 1001-1250 companies ranked by market cap, which have an average market cap of Rs 21 bn. Herein, MM’s performance looks far superior; MM’s TTM/2QFY26 PAT growth came in at 11%/13% YoY vs -23%/-8% for the 750-1000 bucket and -12%/-9% for the 1001-1250 bucket of companies by market cap.

MM’s earnings growth is superior to its peers in 2QFY26 on a YoY basis

*Calculation is as per the simple average of absolute revenue/EBITDA/PAT for all companies. PAT calculation excludes other income.

Source: Ambit Asset Management

Top 3 and Bottom 3 Performers:

Source: Ambit Asset Management

Globus Spirits

- Profit growth was driven by steady IMIL performance, a reduction in IMFL losses, and a recovery in manufacturing margins to INR 5.4/litre.

- The Board announced Vision 2029, where they are targeting to achieve revenue of Rs 4500 crore vs ~Rs 2500 crore in FY25.

- Rajasthan volume growth should resume at a single-digit level in the R&O segment; the UP distillery is expected to start in Q3FY26.

Bajaj Healthcare

- QoQ margin improvement driven by increasing focus on API exports (since domestic prices are falling).

- Strong pipeline with 10 CEPs (7 approved), as well as approvals for phase 3 of the insomnia molecule and an anti-epileptic molecule.

- Alkaloid business revenue was NIL in 1H and we expect around 40crs revenue in H2. Rs 300 crore addition to revenue led by the new revenue stream of CDMO business.

Entero Healthcare Solutions Ltd

- Entero reported strong revenue growth of 20% YoY, led by acquisitions, and 50% EBITDA growth, led by favorable operating leverage.

- The OCF decline reduced significantly, led by a reduction in inventory days from 70 to 60.

- The guidance is to report Rs 1 bn OCF in FY26 and report 40% revenue/EBITDA growth in FY26.

Source: Ambit Asset Management

Foods & Inns Limited

- PAT declined due to higher other expenses led by higher export freight and MTM loss - GP per MT fell by 6% YoY, led by some impact of tariffs.

- Production volumes are higher by 20%, led by better pricing thanks to a good crop.

- Mango exports are looking promising due to relative competitiveness with Mexico on account of falling Tota Puri prices.

Landmark Cars Limited

- Profitability got impacted on account of the abolition of cess which made recovery of unutilized cess for dealers difficult; hence discounts given to recover cess before 22nd Sept.

- OCF was very strong at Rs1.7 bn in 1H; >60% YoY growth. 100 bps GM improvement expected in H2 led by discounts no longer available and rising share of after-sales service revenue.

- Q3 so far has been doing very well (>20% revenue growth) as per management in the concall.

Khadim India Limited

- Revenue declined given the impact of the GST transition; all footwear companies like Bata and Relaxo reported weak results. GM was impacted by discounts in July and August due to weak demand from the heavy monsoon.

- GST has been cut to 5% from 12% in the category below Rs 2,500 per pair. This should boost sales as ~70% of Khadim's portfolio is in this range.

- GM should improve to 50-52% in FY27, led by the GST cut leading to higher demand for premium products within value retailers.

Liquidity for microcaps has seen a significant dip in the last year:

One of the biggest reasons for the negative portfolio performance in MM is the reduced liquidity. The ADTV of the portfolio in the last year has declined by 27%, and every month for the last six months the same has been falling consistently. A few stocks that have seen a significant decline in ADTV are Platinum Industries, Ice Make Refrigeration, and Team Lease Services. In these stocks, despite a strong performance in the recent 2QFY26 results, the stock reaction has been very weak.

Conclusion:

Market conditions remain challenging and polarized, but the earnings recovery expected in the second half of FY26, supported by improving consumer demand, stronger capex momentum, and a favorable base, creates a constructive backdrop for equity investors. In this environment, using near-term weakness to selectively increase exposure to high-quality, fundamentally strong businesses with robust earnings trajectories and reasonable valuations can help build resilient, long-term compounding in equity portfolios.

Ambit Coffee Can Portfolio

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has an unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced with disruptions at regular intervals. As the industry evolves or is faced with disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

Exhibit 2: Ambit Coffee Can Portfolio point-to-point performance

1765447548185.jpg)

Source: Ambit Coffee Can Portfolio inception date is Jun 20, 2017;

**1M Return: 1st - 30th Nov'25; 3M Return: 1st Sept'25 – 30th Nov'25; 6M Return: 1st Jun'25 – 30th Nov'25; 1Y Return: 1st Dec'24 –30th Nov'25

*Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The performance related information provided herein is not verified by SEBI.

Exhibit 3: Ambit Coffee Can Portfolio calendar year performance

1765447569339.jpg)

Source: Ambit Coffee Can Portfolio inception date is June 20, 2017;

*Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The performance related information provided herein is not verified by SEBI.

Ambit Good & Clean Midcap Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

1. Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

2. Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longerwith annual churn not exceeding20-25% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with these compounding earnings acting as the primary driver of investment returns over long periods.

3. Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

Exhibit 4: Ambit Good & Clean Midcap Portfolio point-to-point performance

1765447627079.jpg)

Source: Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015;

**1M Return: 1st - 30th Nov'25; 3M Return: 1st Sept'25 – 30th Nov'25; 6M Return: 1st Jun'25 – 30th Nov'25; 1Y Return: 1st Dec'24 –30th Nov'25

*BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Mid cap. The performance related information provided herein is not verified by SEBI.

Exhibit 5: Ambit Good & Clean Midcap Portfolio calendar year performance

1765447658418.jpg)

Source: Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015;

*BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Mid cap. The performance related information provided herein is not verified by SEBI.

Ambit Micro Marvels Portfolio

We aim to create a portfolio that invests predominantly in micro-cap companies with the potential of delivering superior earnings growth and generating relatively better risk-adjusted performance over a long period of time.

Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts while our proprietary ‘greatness’ framework helps identify efficient capital allocators. The result is a concentrated portfolio of 20-25 stocks that draws down less than the market in corrections and has low churn.

Key Features of Portfolio Companies:

1. High earnings growth companies with low leverage,

2. Market leaders or challengers with strong moat around brand, distribution, technology, and innovation,

3. Strong corporate governance coupled with apt capital allocation.

Exhibit 6: Ambit Micro Marvels Portfolio point-to-point performance

1765447674455.jpg)

Source: Ambit Micro Marvels Portfolio inception date is Jul 29, 2024;

**1M Return: 1st - 30th Nov'25; 3M Return: 1st Sept'25 – 30th Nov'25; 6M Return: 1st Jun'25 – 30th Nov'25; 1Y Return: 1st Dec'24 –30th Nov'25

**BSE 500 TRI is the selected benchmark for the Ambit Micro Marvels Portfolio. The performance related information provided herein is not verified by SEBI.

*Nifty Smallcap 250 TRI is the secondary benchmark, being provided solely for additional reference and comparison. For details refer disclaimer clause.

Exhibit 7: Ambit Micro Marvels Portfolio calendar year performance

1765447682840.jpg)

Source: Ambit Micro Marvels Portfolio inception date is Jul 29, 2024;

**BSE 500 TRI is the selected benchmark for the Ambit Micro Marvels Portfolio. The performance related information provided herein is not verified by SEBI.

*Nifty Smallcap 250 TRI is the secondary benchmark, being provided solely for additional reference and comparison. For details refer disclaimer clause.

Ambit Pricing Prowess Fund

Ambit Pricing Prowess Fund is an All-weather, Open-ended, Long-only, Category III, Flexi-cap AIF – a meticulously crafted opportunity for long-term investors seeking:

- Accelerated Portfolio Returns: The ability to raise selling prices faster than input costs (inflation) directly increases profit margins and accelerates Free Cash Flow (FCF) growth.

- Unrivaled Portfolio Resilience: Pricing Power acts as a structural defense mechanism, stabilizing margins even during periods of macro pressure, supply shocks, or weaker demand.

- Maximum Long-Term Value Creation: Pricing Power is a proxy for an irrefutable competitive advantage (deep moat).

In a market of highly varied valuations, Ambit Pricing Prowess Fund is not constrained by a single market segment. We are designed to seek the most attractive combination of Quality and Price across the entire investment universe.

We can shift capital fluidly between Large, Mid, Small, and even a select number of carefully vetted unlisted businesses. This broad mandate allows us to find and capitalize on unique opportunities that align with our core framework.

Our focus is more on business fundamentals, rather than stock price movements. We do not seek comfort of the crowd and seek exposure to companies that are "unrecognized" because the market either misprices the longevity of their growth or fails to fully appreciate the structural defense their pricing power provides.

The framework's final structure—blending Established (proven track record, mature moats) and Emerging (new, rapidly widening moats, higher growth potential) Pricing Power plays—provides a balanced approach to capture both resilience and accelerated return potential within the portfolio.

Investing in businesses with Pricing Prowess offers compelling advantages, as below:

- Proven Inflation Hedge

- Maximized Profit Margins

- Stable, Quality Compounding (non-Glamorous)

- Formidable Entry Barriers

- Long-term Value Creation

Exhibit 8: Ambit Pricing Prowess Fund

1765447705450.jpg)

Note: Data as on 30th Nov 2025; First close for Ambit Pricing Prowess Fund was done on 24th Sept 2025; Returns are computed at Fund level and are pre fees and on pre-tax basis. Returns of BSE 500 and Nifty 50 is being provided solely for additional reference and comparison. The performance related information provided herein is not verified by SEBI.