Understanding the Mining Services Industry & Global Bulk Material Handling

The mining services and bulk material handling industry plays a pivotal role in supporting global industrial infrastructure. It facilitates the movement, handling, and processing of heavy raw materials such as coal, iron ore, limestone, clinker, and copper, which are critical inputs for sectors like mining, steel, cement, power, and ports. Typically, developed markets tend to be more regulated and consolidated, while emerging markets remain fragmented, served by both organized and informal players.

The industry spans multiple segments, including:

- Equipment and spares/consumables: Conveyors, crushers, screens, filtration systems, corrosion protection and rubber lining, and mill liners.

- Site-based services: Belt splicing, shutdown support, operations & maintenance (O&M), and repair services.

- Integrated solutions: Typically includes bundled packages including product models as well as the requisite servicing.

The global bulk material handling and mining services market is projected to grow from USD 47.1 billion in 2024 to USD 74.6 billion by 2034 (implied CAGR of 4.7%). Growth is being driven by long-term infrastructure projects, rising material throughput, and increasing industrial investment, especially in the mining, cement, and steel sectors.

The global conveyor systems market has grown significantly in recent years, driven by rising automation, safety compliance, and demand from industries like mining, power, cement, ports, and logistics. This market is projected to grow from USD 6.9 billion in 2025 to USD 11.8 billion by 2035. Integrating smart sensors and innovative communication systems into automated conveyors, along with more efficient motors and controllers, is expected to boost growth in this sector. The Indian conveyor systems market is projected to grow from $531 million in 2023 to $856 million by 2033, at a CAGR of 6.44%, led by industrialization, infrastructure push, and increasing cement and steel demand.

Key Players

This industry features a moderately consolidated structure on the product side, while the services segment remains highly fragmented, particularly in markets like India and parts of Africa. Global players like Metso (Finland) and FLSmidth (Denmark) with their revenue being $5.2 billion and $2.9 billion, primarily focus on equipment manufacturing and system integration. The service landscape remains dominated by regional contractors in emerging economies, where unorganized manpower-based models are common.

Global Industry Characteristics

About Thejo

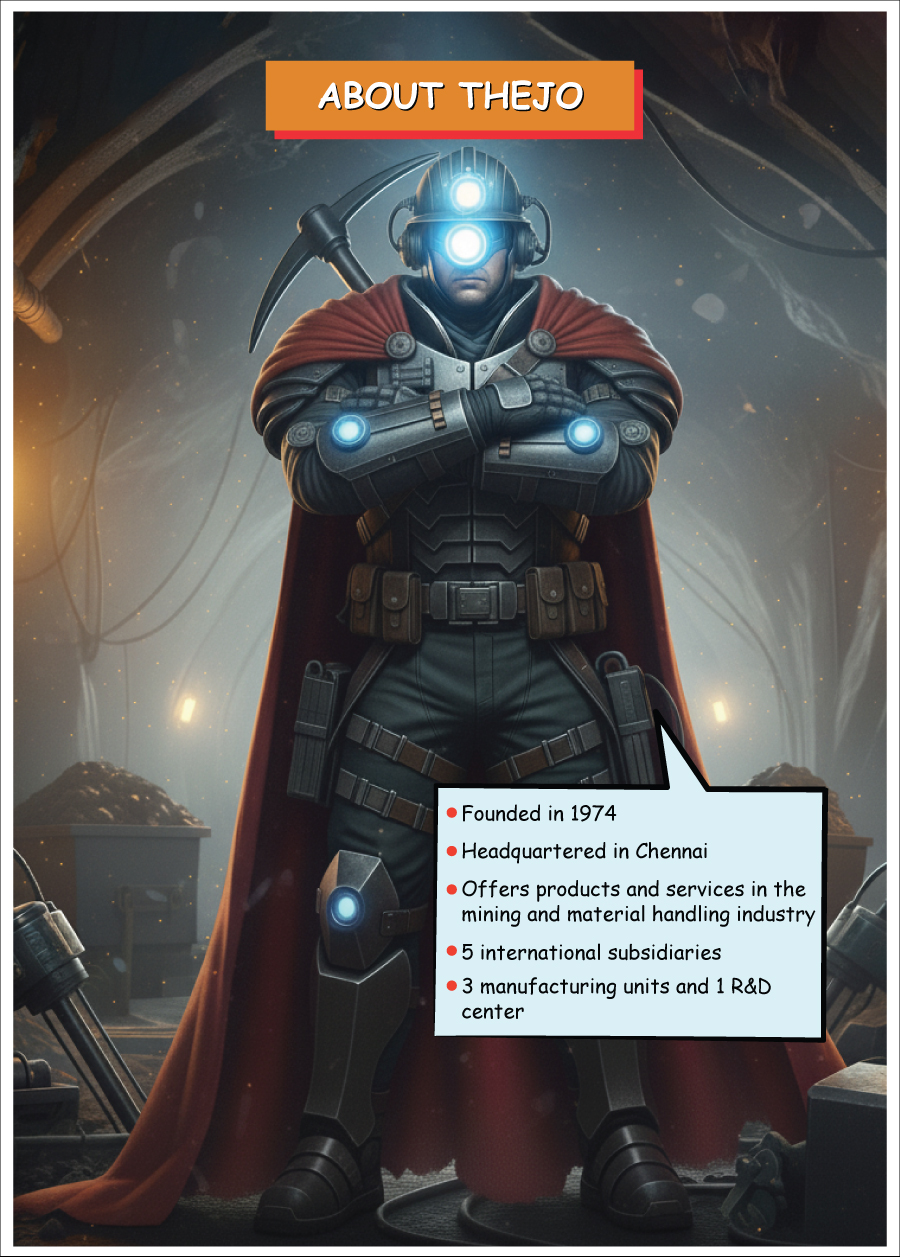

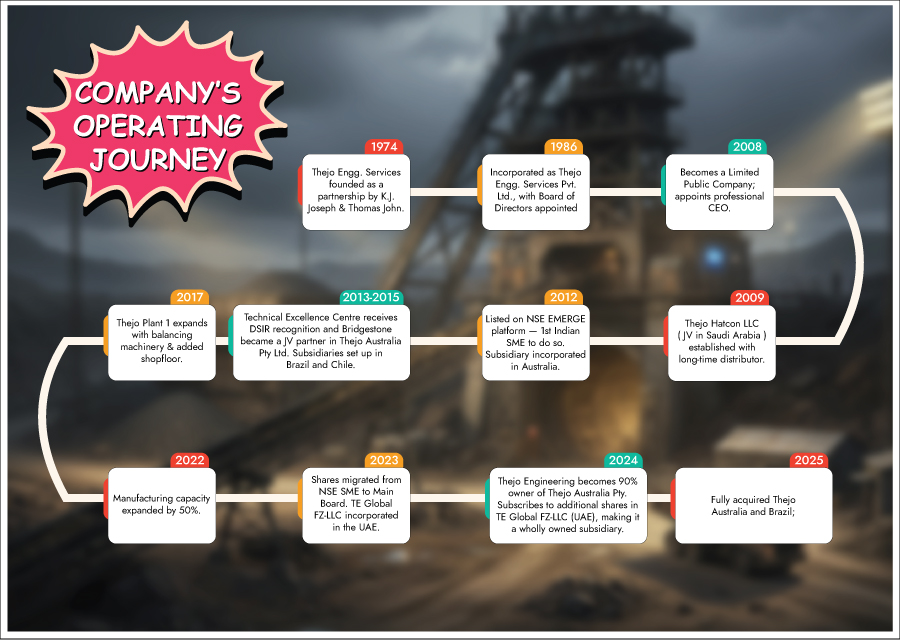

Founded in 1974 as a partnership firm, Thejo Engineering Ltd is a leading Indian provider of specialized engineering solutions for the mining, mineral processing, and bulk material handling industries. Headquartered in Chennai, the company was founded by Mr. K.J. Joseph and Mr. Thomas John (two friends) in 1974 as a partnership firm. Over the decades, Thejo has evolved into an integrated player offering a unique blend of engineered products, site-based services, and operation & maintenance (O&M) solutions, setting it apart in a niche, technical market.

Thejo’s leadership includes a highly experienced management team with deep expertise in conveyor systems, wear protection, and industrial rubber technologies. Thejo is the first company in India to be listed on NSE Emerge.

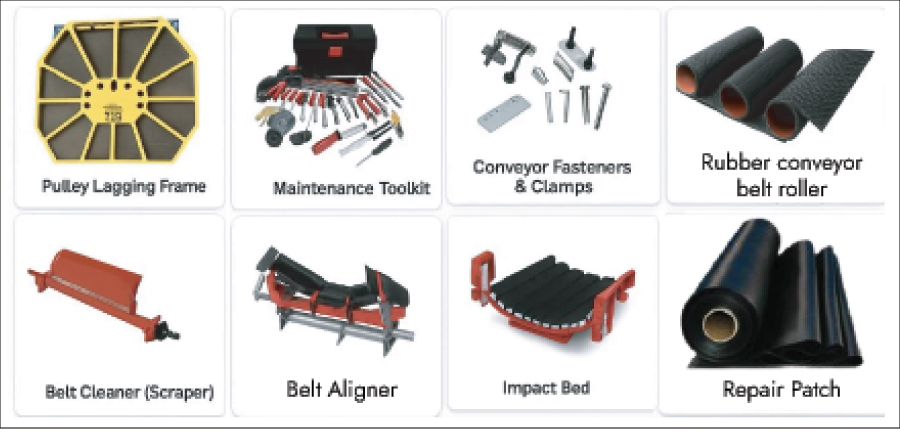

Operating under a dual business model - products and services - Thejo manufactures rubber and polyurethane-based products such as sheeting, adhesives, wear liners, corrosion resistant lining, belt conveyor accessories, screen panels, filtration spares, belt vulcanising machines etc... through its Chennai-based facilities. On the services side, it provides conveyor maintenance, belt splicing, and rubber lining at client sites across mines, power, mineral processing, ports, base metals like steel, aluminum etc., cement, phosphate, rare earth, precious metals like gold, copper, etc.

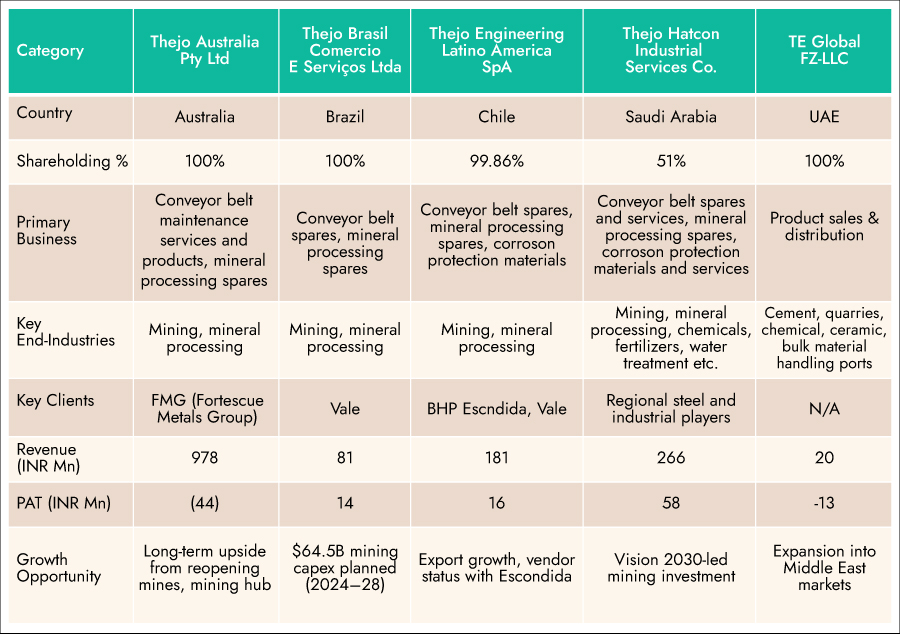

With a growing international footprint, Thejo operates 5 overseas subsidiaries in Australia, Brazil, Chile, Saudi Arabia, and the UAE, supporting both exports, localized services and Products. International revenue constitutes ~31% of consolidated sales of the company.

With a strong base in South India and a pan-India operational presence, Thejo operates 3 state-of-the-art manufacturing units and an in-house R&D center in Chennai. Thejo is present across 45+ locations in India, through its branch and site offices, and operates globally through its subsidiaries and distributors across 10 countries, offering access to a wide range of patented and high-performance engineered products. This robust infrastructure and global reach have positioned Thejo as a dominant and differentiated player in the material handling and industrial maintenance space - both in India and globally.

Thejo's Sub Brands

Esteemed Client Base

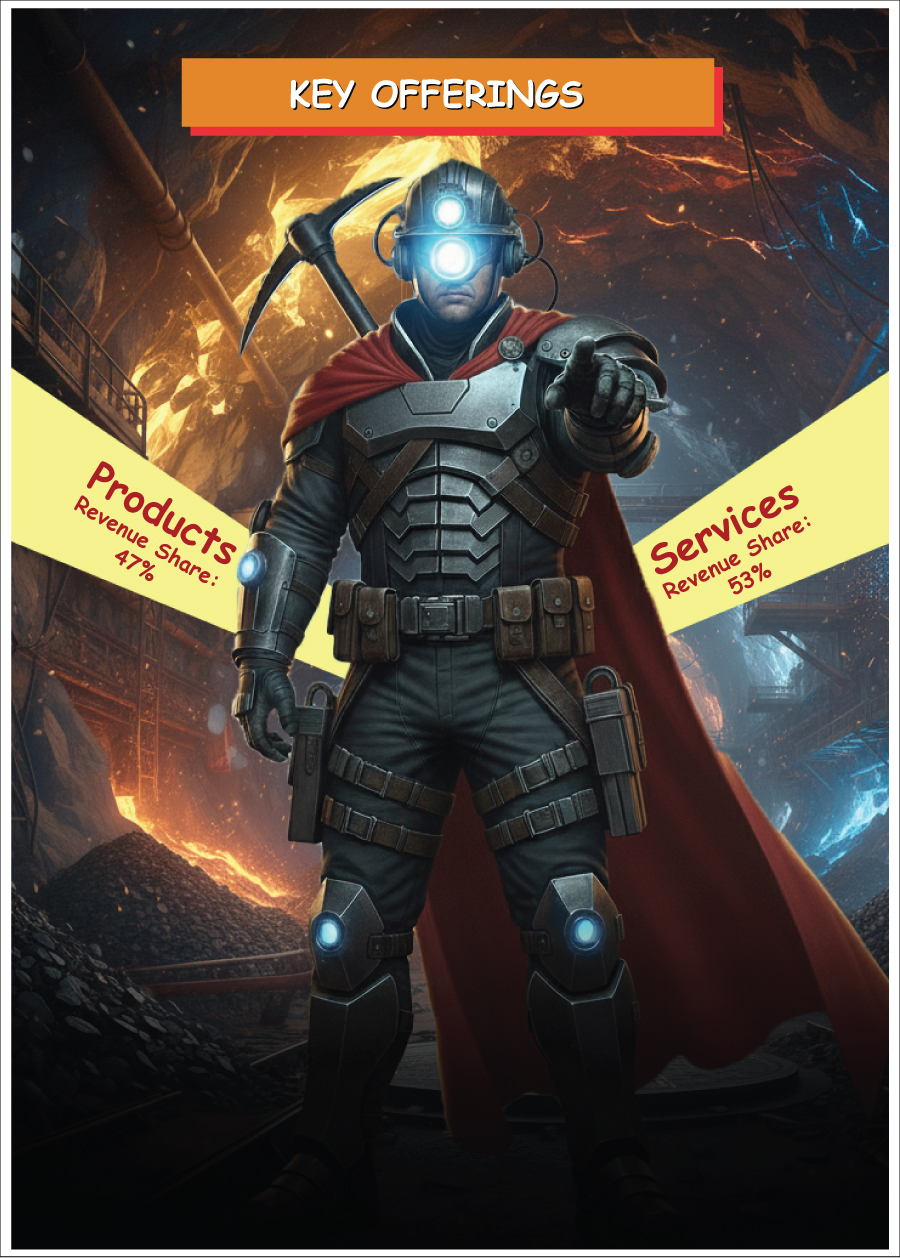

Products: (Revenue Share: 47%)

Mineral Processing:

Range of products for the mineral processing segment, designed to enhance productivity, efficiency, and operational lifespan in grinding and filtration applications within the mining and mineral processing industries.

Bulk Material Handling:

Products in the bulk material handling segment are designed to ensure efficient and reliable movement of materials, in a range of industries like mining, steel, cement, ports.

Services: (Revenue Share: 53%)

Technical Services (~70% of services revenue)

Focused on specialized, project based support and plant operations such as preventive and breakdown maintenance, conveyor installations, belt audits, scanning, splicing, and commissioning. These are high-skill, high-impact tasks, often requiring 24/7 deployment during critical plant outages.

Operations & Management Services (~30% of services revenue)

Involve ongoing, routine management of industrial plants and mines—covering daily inspections, equipment upkeep, and manpower deployment. Historically seen as a labor-intensive support function, the segment is now transitioning toward long-term, KPI-linked contracts with bundled equipment supply.

Thejo’s Global Presence

Brazil Market Turnaround

1. Why Growth Was Initially Slow (Pre-FY24):

Between FY19 and FY23, Thejo Brasil remained a small, loss-making entity with total revenue under ₹30 million. The company was intentionally in a build-out phase, focusing more on establishing its foundation than scaling aggerssively.

- Operations were being built from scratch in a new market.

- Investments went into infrastructure, local hiring, and market understanding.

- The client base was narrow, and scale had not yet been achieved.

2. What Triggered the Turnaround in FY24:

FY24 marked a sharp inflection point for Thejo Brazil, with revenue jumping from ₹27 million to ₹179 million and PAT rising from ₹9 million to ₹102 million. This shift was driven by stronger product traction and a game-changing engagement with Vale.

- Higher sales of mineral processing products like mill liners and filtration parts.

- Stronger presence among large clients, especially Vale.

Vale’s Breakthrough Order:

Vale, a global mining giant, needed to restart a key filtration plant after a major 2019 accident. Instead of choosing OE supplier Larrox (now Metso), Vale awarded the contract to Thejo based on:

- Proven success at BHP’s Escondida mine (Chile).

- Comparable product quality, with 15–20% lower pricing.

- Superior on-site service capability.

This order validated Thejo’s product and service quality in a highly demanding environment and led to repeat orders for high-value filtration components.

3. Expected Growth in the Near Future:

Thejo Brazil is now well-positioned for sustained growth, supported by internal control and external market conditions.

- Thejo assumed 100% ownership of the Brazil operations post-FY25, ensuring full profit consolidation and tighter control.

- Brazil’s mining sector is entering a capex upcycle. IBRAM forecasts US$64.5 billion in mining investments between 2024 and 2028 vs ~$40bn over the preceding 4 years.

Thejo has successfully completed the qualifying trials for Mill Liners with VALE, and are in the process of entering into long term supply contract with VALE. Successful Mill Liner perforrmance at other mineral projects is pushing growth of this product line.

Growth in the Australian Market

Issues Faced by the Australian Mining Sector:

- Dependence on China

- Demand slowdown from China (Australia’s largest trading partner) led to lower prices for iron ore, coal, and lithium, putting pressure on margins and causing temporary shutdowns.

- Environmental and Regulatory Pressures

- New laws on carbon emissions and indigenous land rights delayed project approvals, especially for new coal mines and expansion of existing ones.

- Labor Shortages and Strikes

- Widespread labor disputes over wage conditions and strikes affected mining schedules and production output.

- Extreme Climate Events

- Floods, cyclones, and heatwaves in key mining states like Western Australia and Queensland disrupted operations and transport.

- Energy Inflation and Supply Chain Constraints

- High energy costs and delays in importing mining equipment (especially post-COVID) inflated operating expenses and slowed expansion.

Why Growth is Returning

- China is seeing a turnaround

The Chinese market, which is highly dependent on Iron Ore, is at the cusp of a recovery after having seen a demand slowdown.

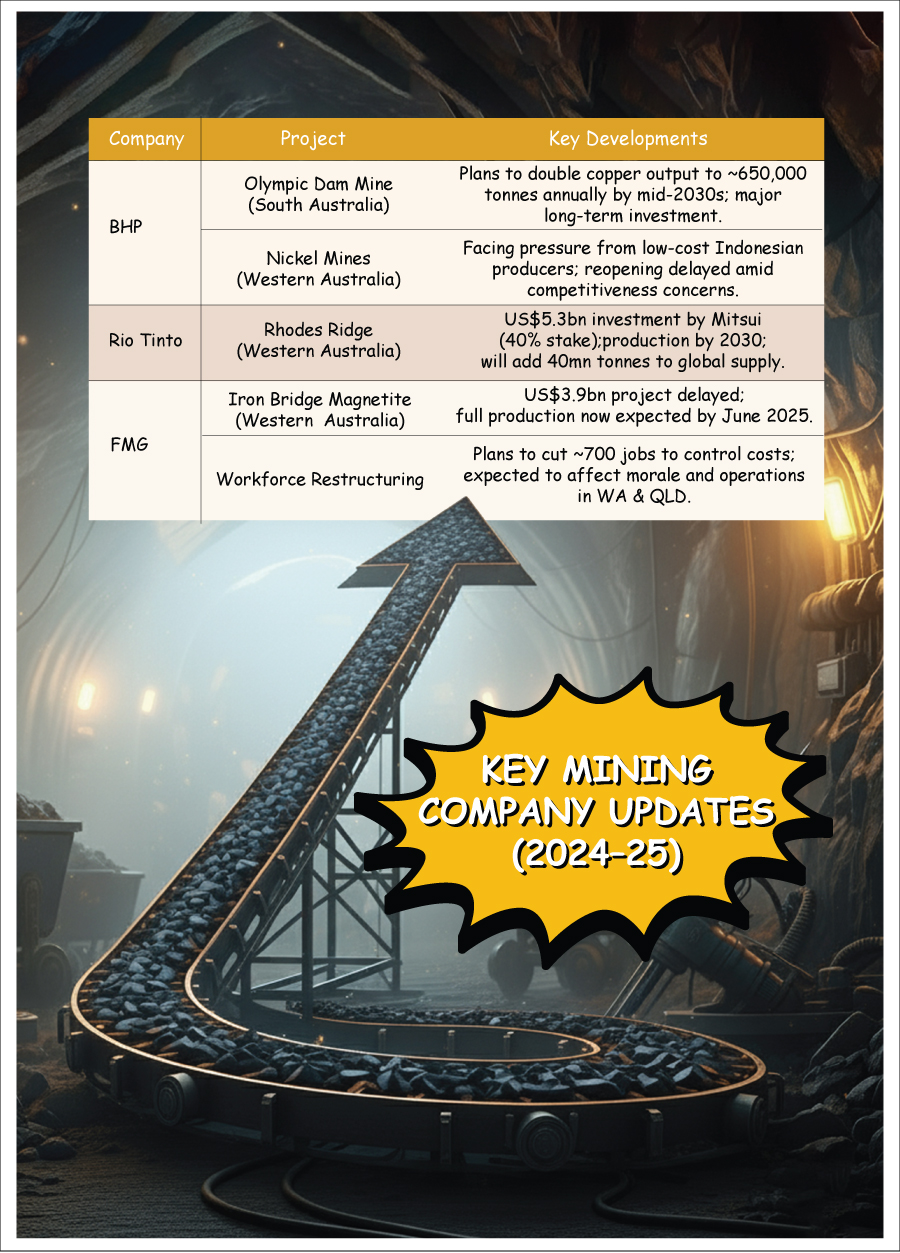

- Mine Expansions and Reopenings

Companies like BHP, Rio Tinto, and Fortescue are expanding production to meet rising global demand for iron ore, lithium, and rare earths.

- Boom in Critical Minerals

The electric vehicle and renewable energy sectors are driving strong demand for lithium, nickel, and rare earths.Australia is positioning itself as a key global supplier in this value chain.

- Government Incentives and Trade Agreements

Policies supporting foreign investment, along with trade partnerships with the US, EU, and Japan, are reducing dependence on China and enabling faster project approvals.

- Automation and Digital Transformation

Growing use of autonomous vehicles, AI-driven exploration, and digital mine management is improving efficiency, safety, and scalability.

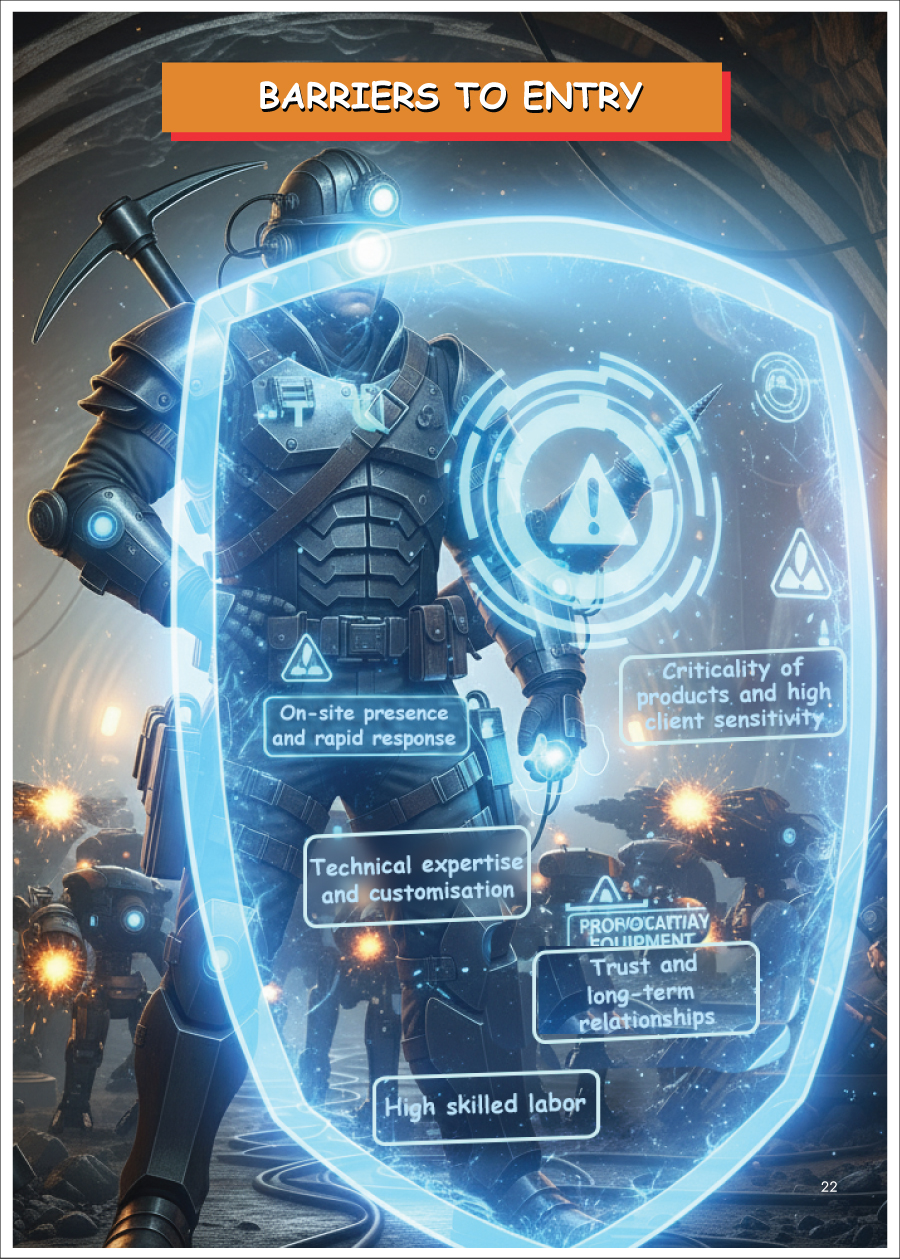

Barriers to Entry: Built Through Product Criticality, Customization, and Service Integration

- Criticality of Products and High Client Sensitivity:

Thejo's products—such as conveyor belt components, filtration press spares, and mill liners—are mission-critical consumables in industries like mining, steel, and cement. While these components may constitute less than 1% of a client’s total operating cost, their failure can cause complete plant shutdowns and heavy financial losses. This creates extreme sensitivity to quality and reliability, making clients unwilling to switch vendors even for a 5–10% price difference, especially when service execution is dependable.

- Necessity of On-Site Presence and Rapid Response:

Thejo’s competitive edge lies in its 24/7 on-site service model, often under Annual Rate Contracts (ARCs). These contracts allow the company to address equipment issues immediately, minimizing costly downtimes for clients. This deep physical integration into client operations reinforces product trust and accelerates product acceptance, as customers feel confident in Thejo's ability to resolve issues promptly.

- Technical Expertise and Customization Requirements:

Thejo’s products are not off-the-shelf; they often require customization to suit unique operating conditions, involving complex material chemistry and design modifications. Supporting such tailored solutions requires an on-ground technical team to understand customer needs and a responsive R&D team to deliver them. This engineering and service linkage is difficult for competitors to replicate without a strong field force and sustained R&D investment.

- Building Trust and Long-Term Relationships:

The company's deep engagement with clients through its service business has been instrumental in building trust. This close proximity has helped Thejo push clients to trial its products, prove their value in real-world conditions, and eventually scale product sales. Because of the proven performance and established reliability, clients typically do not switch to cheaper alternatives without a strong value reason.

- High Skilled Labor Requirement:

Thejo's integrated product-service model requires skilled manpower, in both in manufacturing and field operations. This is reflected in its employee cost exceeding 30% of consolidated revenue, significantly higher than product-centric peers like Tega Industries (15–20%). While this raises the cost structure, it reinforces the entry barrier, as replicating Thejo’s workforce quality and customer trust is not easy for new entrants.

Senior Management Hire:

Mr. Thorsten Wach was hired as President of International Sales & Marketing in March 2025. He is an esteemed professional with experience in leadership (CEO) roles in companies like Continental AG and Rema Tip Top.

We believe, Mr Thorsten can significantly help Thejo in spreading its wings in the international markets given his significant achievement at Rema Tip Top where he successfully established presence of Rema Tip Top in various geographies like Africa, APAC, Germany and Northern Europe.

About Rema Tip Top:

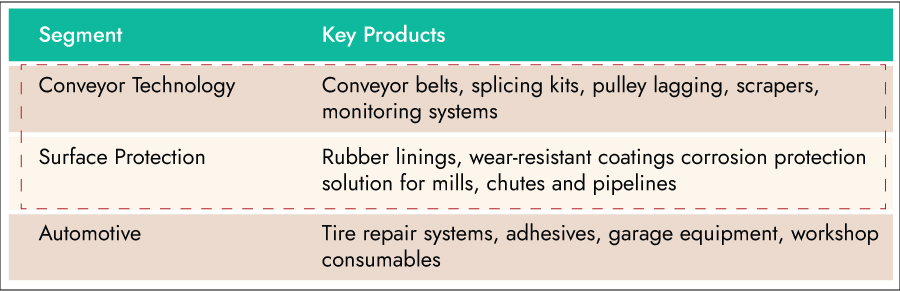

Rema Tip Top is a Germany-headquartered global engineering group that specializes in conveyor technology, surface protection, and automotive solutions. Founded in 1923 and now part of STAHLGRUBER Otto Gruber AG, the company has grown into a multinational with more than 8,000 employees, operations in over 170 countries, and annual revenues of ~€1.5 billion.

Rema Tip Top Product Portfolio:

Key Ventures at Rema Tip Top:

Revitalizing African Operations:

- Hired in 2006 as CEO of the African cluster.

- Transformed it into one of the leading service providers across key African markets by expanding the service network and orchestrating the acquisition of Dunlop Industrial Products.

APAC – Efficiency & Profitability:

- Took on a leadership role in the Asia-Pacific cluster from 2014.

- Boosted profitability by leveraging synergies between regions and embedding best-practice models, an astute approach for scaling margin performance.

Acquisition of COBRA:

- Led Rema Tip Top to fully acquire French conveyor specialist COBRA Group.

- This strategic move expanded production capabilities, modernized distribution, and enhanced the company's foothold in conveyor belt technologies across global markets.

- Importantly, the deal preserved COBRA’s entrepreneurial agility while bringing it into Rema Tip Top’s synergistic framework.

Strengthening German Presence:

- Further bolstered Rema Tip Top’s delivering network in Germany by acquiring Gulich, a conveyor systems provider.

- The move strategically broadened the service portfolio while retaining existing talent and operations.

Expansion into Northern Europe:

- Instrumental in acquisition of Hihnatyö Oy in 2017, a Finnish company specializing in conveyor and drive technology.

- The deal added service, commissioning, and maintenance capabilities in newly tapped industrial segments, further solidifying Rema Tip Top’s industrial reach in Northern Europe.

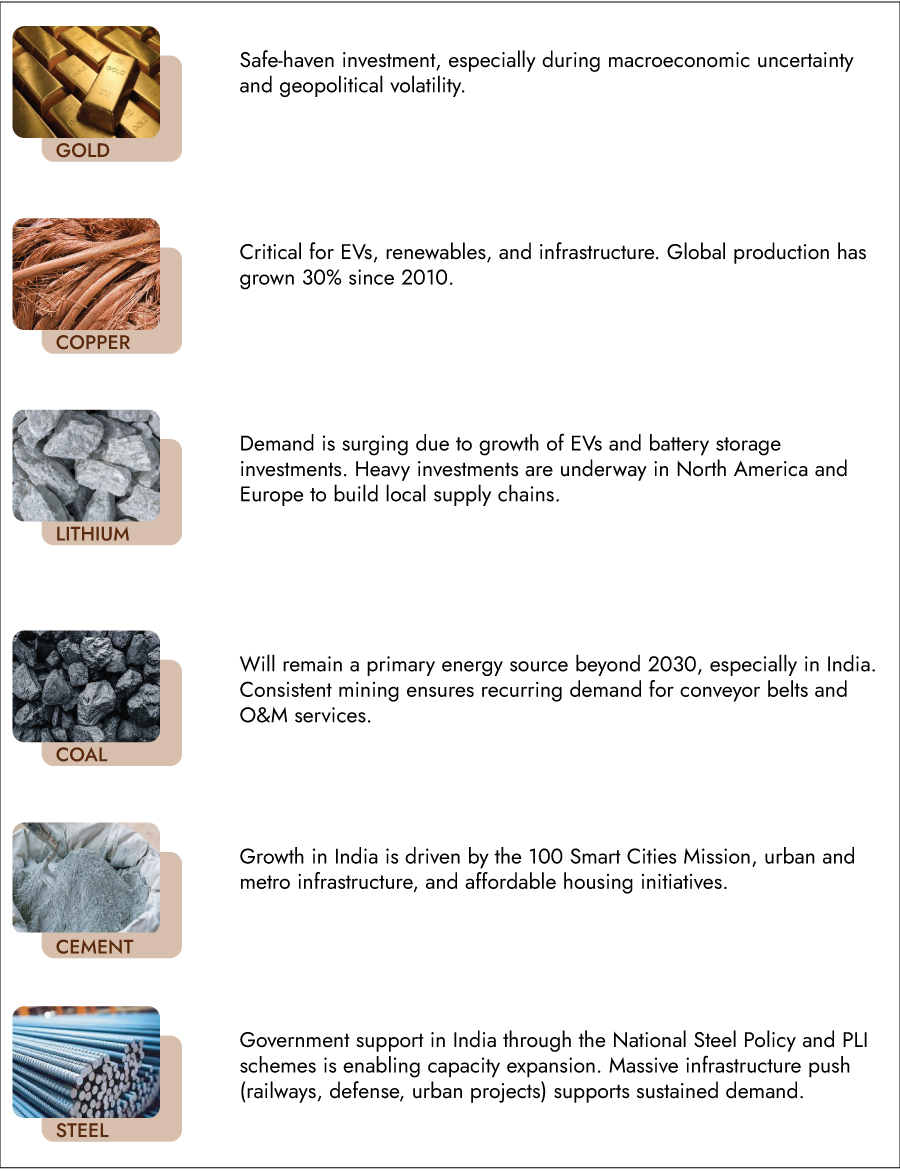

Growth linked to Underlying Industries