Indian Automotive Landscape

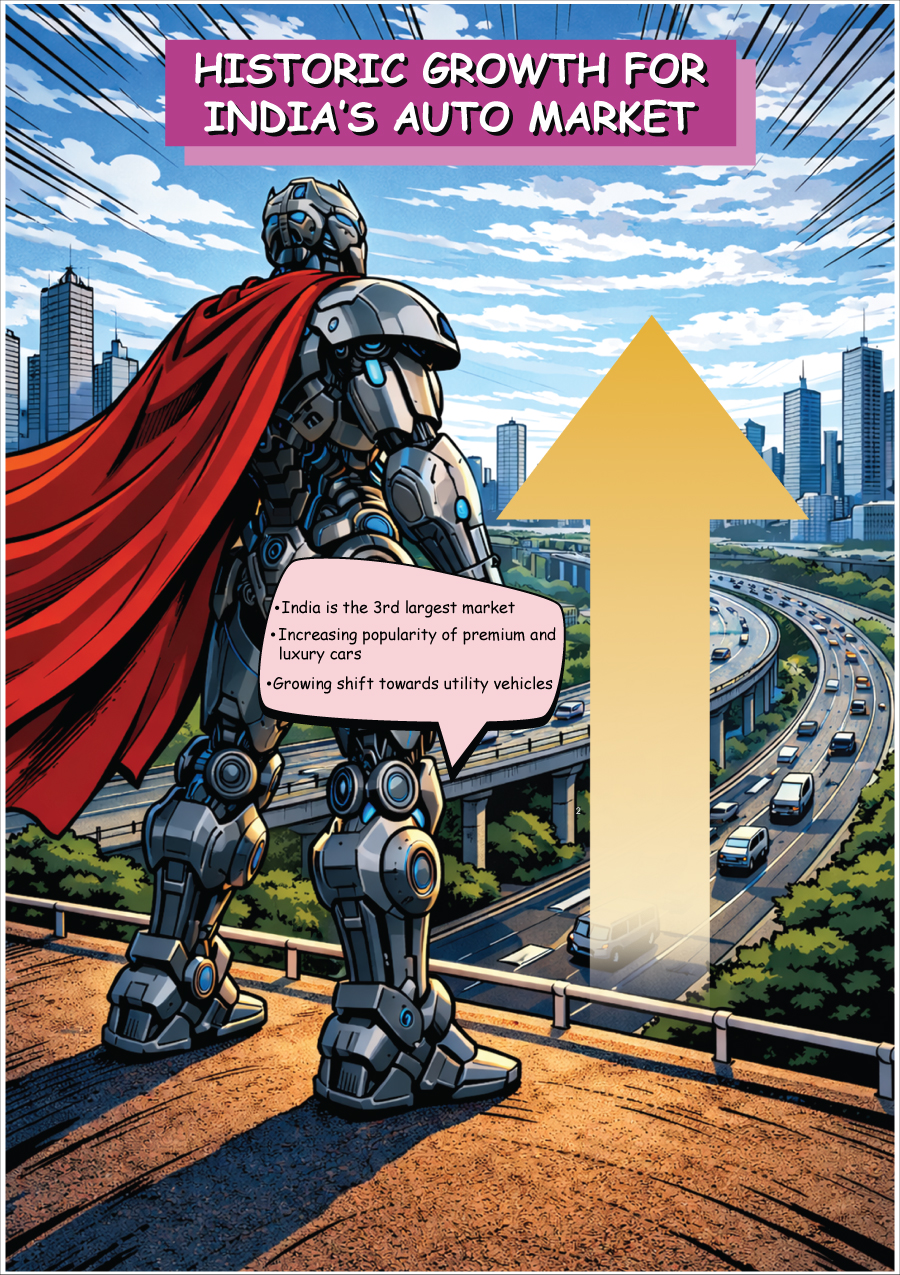

India is the 3rd largest passenger vehicle market globally, after China and the USA. In 2024-25, the Indian PV industry achieved its highest-ever retail sales of 4,153,432 units, reflecting 4.8% YoY growth and marking the highest-ever retail sales for the industry. Growth was driven by a combination of factors, including expanding product portfolios, rising consumer aspirations, expanding urbanisation, especially beyond major metros into Tier-II cities and a supportive regulatory environment. Within the industry, there is clear and growing evidence that premium and luxury passenger vehicles are gaining prominence in the Indian market compared to entry-level cars, driven by rising affluence, changing consumer preferences, and expanding market reach. An important trend shaping the segment was the growing shift towards utility vehicles, which now comprise a significant share of overall PV sales. Consumers are increasingly gravitating towards larger, feature-rich vehicles, valuing comfort, versatility, and safety - qualities that reflect India’s maturing buyer profile. Top OEM's in India

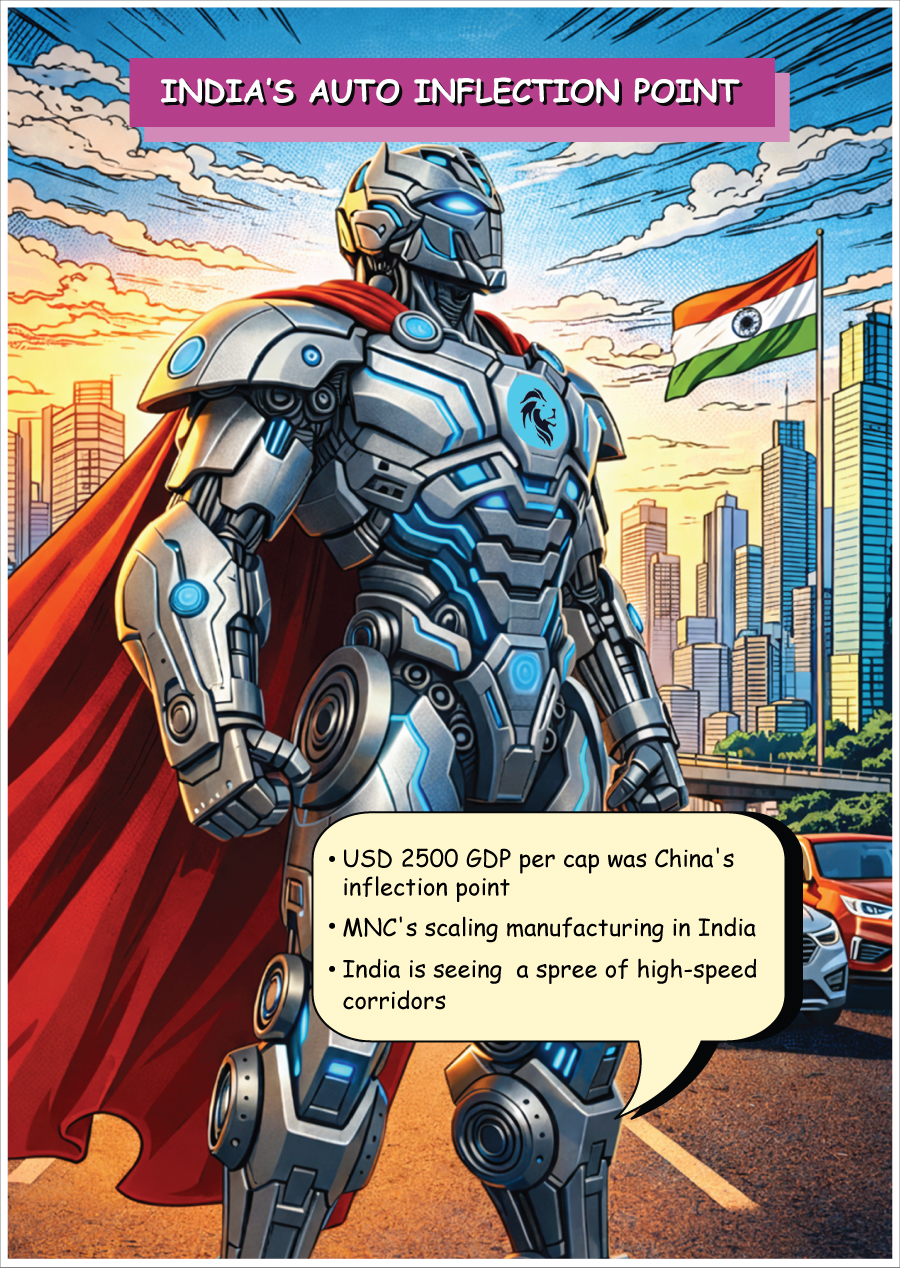

India’s Premium and Luxury Car segment at an inflection point

Chinese Auto Penetration increased significantly post GDP per capita crossing USD 2,500 India today is at a similar stage of economic development as China was in 2007, when China’s per capita

income was around USD 2,500. This income threshold proved to be a critical inflection point for vehicle adoption in China. As per capita income crossed USD 2,500, car penetration rose sharply—from 17 cars per 1,000 people in 2007 to 43 by 2010 (at ~USD 4,500 per capita income), and further to 153 by 2019 (at ~USD 10,000 per capita income). The Chinese experience underscores how rising incomes can drive a sustained and non-linear increase in automobile ownership, a trajectory that India is now well-positioned to follow.

USD 2,500 GDP per capita was an inflexion point in China…for car penetration to increase rapidly

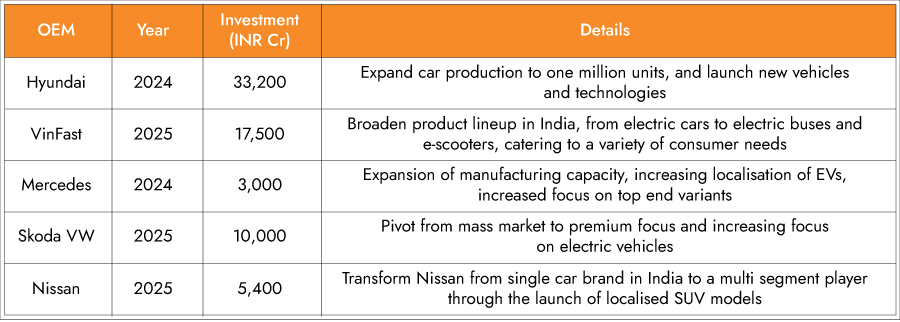

Rising Localization by OEMs to facilitate higher penetration led by affordable cost and efficient supply chain:

Over the past five years, global luxury automotive brands have aggressively scaled their Indian manufacturing investments to transition from a niche import model to a high-volume, localized strategy. This shift is critical for capturing market share, as domestic assembly allows brands to bypass heavy import duties and significantly lower on-road prices for consumers. Beyond affordability, deep localization ensures a resilient supply chain that improves the immediate availability of new vehicles and drastically reduces lead times for spare parts, which is vital for the timely servicing and reliability expected of premium brands.

Several MNC brands have scaled up manufacturing investments in India

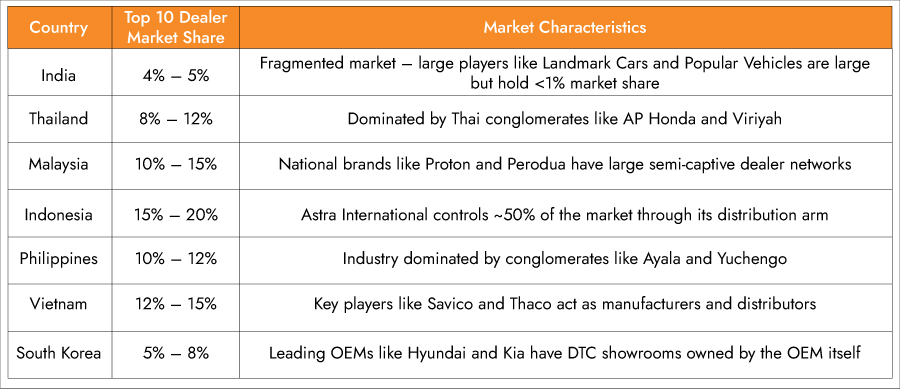

Industry Consolidation: A Global Trend Playing Out in India

Global Context – From Fragmentation to Consolidation

The automotive retail landscape across Asia exhibits a sharp contrast in structural maturity and concentration. While the Indian market remains largely fragmented and dominated by regional entrepreneur-led networks, Southeast Asian markets are characterized by heavy institutional consolidation. In Thailand, massive conglomerates such as AP Honda and Viriyah exert significant control over the dealer ecosystem. This concentration reaches its peak in Indonesia, where vertical integration is the norm; players like Astra International manage both the distribution and retail arms, commanding a dominant 40–50% market share. Conversely, South Korea bypasses the traditional dealer model entirely, with key OEMs utilizing DTC platforms and company-owned showrooms to maintain a captive relationship with the end-user.

Market share of top 10 dealers in South East Asian countries

Landmark Cars’ numerous acquisitions are an indicator of industry consolidation

1769746432097.jpg)

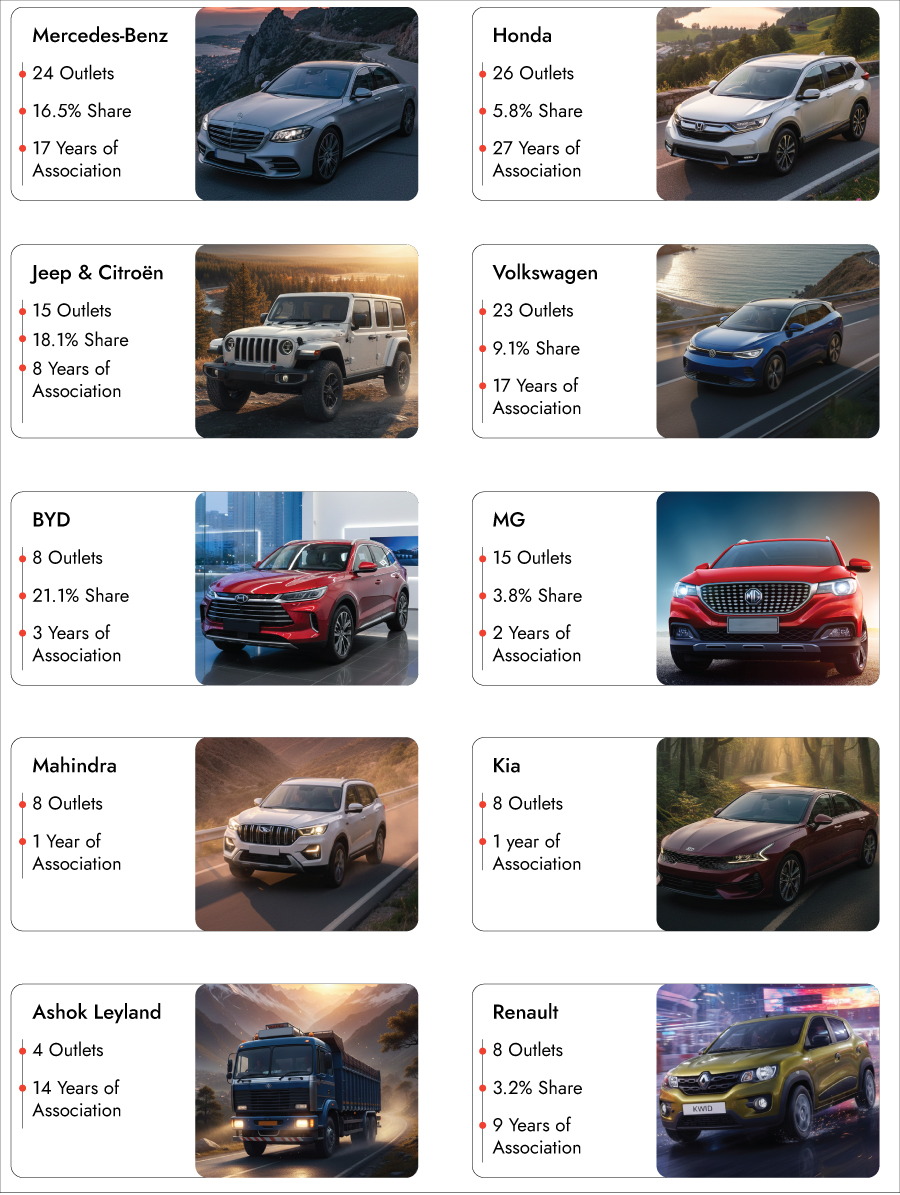

Landmark Cars Ltd is one of India’s leading premium and luxury automobile retail groups, operating dealerships for brands such as Mercedes-Benz, Honda, Jeep, Volkswagen, BYD, MG, and Mahindra.

Headquartered in Ahmedabad, the company has a presence across 28+ cities in 10 states through over 130 facilities, covering the entire automotive value chain — new car sales, after-sales service, spare parts, accessories, pre-owned vehicles, and third-party finance and insurance facilitation.

Landmark has also expanded into the electric vehicle space through partnerships with BYD and MG Select and operates commercial vehicle dealerships for Ashok Leyland. The company benefits from its strong brand portfolio, increasing focus on the higher-margin after-sales business, and a gradual shift toward an asset-light agency model.

1769755033365.jpg)

1769746707302.jpg)

1769746995983.jpg)

Multi-Brand Portfolio

1769747026468.jpg) Large no of OEM tie-ups: Maintains a strong competitive advantage through its diversified portfolio of OEM tie-ups, which provides a crucial hedge against cyclical downturns and brand-specific risks.

Large no of OEM tie-ups: Maintains a strong competitive advantage through its diversified portfolio of OEM tie-ups, which provides a crucial hedge against cyclical downturns and brand-specific risks.

The company effectively covers the entire retail spectrum, catering to a wide range of vehicles priced from approximately INR 1 Mn up to INR 40 Mn.

Diverse customer base: Enables Landmark to serve customers across metros, Tier 1, and Tier 2 markets spanning multiple segments. For example, just for Mercedes, Landmark has outlets in Gujarat, Maharashtra, West Bengal, Bihar, Telangana.

OEM negotiating power: As one of the largest volume dealers, Landmark rationally should enjoy stronger bargaining power on dealership terms, discounts, and incentives, along with greater leverage

to secure favorable vehicle allocations and marketing support. Its scale also gives it significant influence in future dealership planning and brand exclusivity decisions.

Enhances Brand Credibility: Amid a fragmented and competitive dealership landscape, Landmark stands out for its wide brand portfolio, demonstrating its strength in operational execution, governance discipline, and effective management of OEM relationships.

Outlet presence across Key States

1769747085080.jpg)

1769755060997.jpg)

Strategic OEM Relationships

Landmark Cars (LC) benefits significantly from its strong and enduring partnerships with global and domestic automotive OEMs, such as Mercedes-Benz (largest partner), Honda, Jeep, Volkswagen, Renault, and Ashok Leyland (Commercial Vehicles). These long-standing ties offer several critical advantages:

Preferred Partner Status is Earned, Not Bought: Unlike other retail businesses, auto dealerships are non-transferable assets. New market entrants cannot simply acquire or build a showroom and begin operations; they must first pass the OEM's extensive screening and due diligence process. LC's nearly

three decades of continuous operations since 1998 and strong compliance history, grant it this privileged "preferred partner" status.

Decades of Mutual Trust Lead to Market Lock-in: Automakers strongly prefer partners that consistently deliver high customer satisfaction scores and adhere to brand standards. LC's long-term relationships with major brands like Mercedes-Benz and Jeep—which often trust LC with multiple cities or

regions—make it unlikely to be replaced by competing dealers in its established markets.

High Switching Costs and Exclusivity: For a new dealer, gaining an OEM's approval is a slow, complex process. OEMs are hesitant to risk their brand reputation on untested partners, especially in the high-stakes luxury segment. Crucially, LC often enjoys geographic exclusivity for some of its outlets, a

right that is locked in by historical contracts. OEMs are reluctant to alter these agreements unless there is a clear case of severe underperformance.

Technical Lock-in through Deep Integration: LC has made key investments in dealer-approved technology, including Dealer Management Systems (DMS) and proprietary diagnostic tools. This deep technical integration creates a "lock-in" effect, significantly raising the upfront cost and time burden for

any new dealership trying to achieve the same level of operational connectivity with the OEM.

Annuity Income Fueled by Customer History: By servicing over 1.8 million customer vehicles since FY20, LC has compiled an invaluable, extensive database of customer histories and vehicle service records. This data is actively used to drive high-margin upselling activities—such as extended warranties

and service packages—and creates strong customer service loyalty that new rivals simply cannot match.

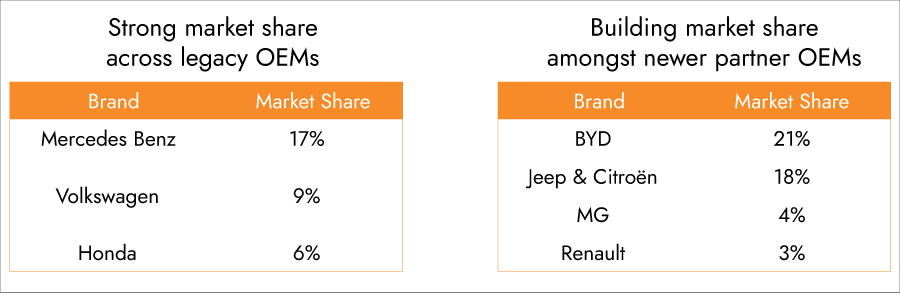

Market share across OEMs

Tie-ups with modern OEMs

The new focus OEMs for Landmark Cars have been MG, Mahindra, and Kia. These brands, especially Mahindra, have seen exemplary performance over the last few years. Mahindra’s market share has

improved from 6% in FY21 to 13% in FY25.

Honda, Renault and Jeep are laggards – but can’t be written off

Honda

Honda Motor Company is charting an aggressive comeback in India, unveiling a major product offensive that includes at least 10 new models by 2030, of which 7 will be SUVs. Currently, the Elevate is Honda’s only SUV offering — a limited lineup that has contributed to its muted recent performance. The upcoming launches are aimed at reviving the brand’s past prominence and strengthening its position in the fast-growing SUV segment.

As one of Landmark Cars’ earliest dealerships, established in 1998, Honda also commands a large and mature installed base of vehicles across Landmark’s operating regions. This extensive fleet ensures steady, high-margin aftersales revenue from maintenance, repair, and spare parts — providing predictable earnings that remain resilient even during periods of soft new car demand.

Renault

Renault is set to re-enter the compact SUV segment with the all-new Duster, slated for launch on Republic Day 2026. The original Duster was among the first compact SUVs in India and played a pivotal role in shaping the segment’s early success, making its comeback an event of strong industry interest.

Jeep and Citroën

Landmark Cars strategically optimizes its existing infrastructure by partnering with Stellantis (the parent group of Jeep and Citroën). The company has implemented a capital-efficient model by selling and servicing Citroën vehicles through its existing Jeep outlets, eliminating the need for incremental showroom or workshop investments. This approach underscores Landmark’s disciplined cost rationalization and focus on maximizing asset utilization.

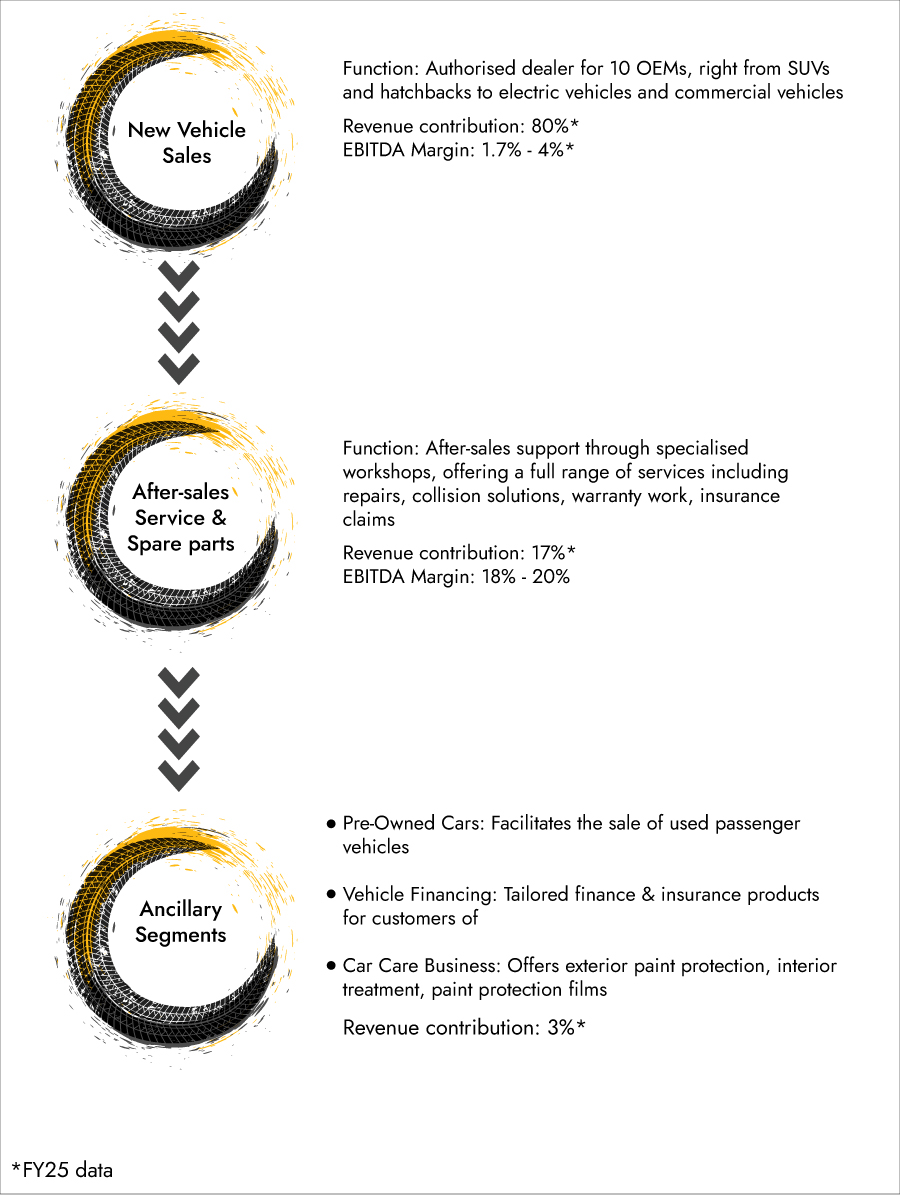

Integrated 3S Business Model – Sales, Service, Spares

Landmark Cars (LC) centers its retail operation around the Integrated 3S Model (Sales, Service, Spares), a sophisticated strategy designed to convert a single vehicle transaction into a long-term, profitable customer relationship. This model differentiates LC from traditional dealers by ensuring that the three core functions of car ownership are tightly linked, maximizing both operational efficiency and financial returns.

The Financial Multiplier: Shifting from Sales to Service

- The 3S model deliberately deemphasizes relying solely on the sales of new cars, which yields relatively low upfront gross margins. Instead, it utilizes the sale as the entry point to generate predictable,

- high-margin annuity revenue from the subsequent two phases:

- Service & Spares Dominance: The revenue generated from vehicle Service and Spares is the core profit driver, achieving gross margins that are typically 5 to 6 times higher than those from vehicle sales. This high-margin, recurring income stream secures the financial resilience of the Group.

- Maximizing Wallet Share: The model expands revenue generation beyond basic service by systematically upselling extended warranty packages, offering comprehensive insurance and financing solutions, and managing certified pre-owned vehicle exchanges.

This cohesive approach allows LC to capture the customer's entire automotive spending, significantly boosting the Customer Lifetime Value.

Operational and Strategic Advantages

- LC leverages the integrated structure to deliver a superior customer experience and secure its status as the partner of choice for global manufacturers.

- Enhanced customer experience: Offering a single, familiar location for all needs (purchase, service, parts, insurance) increases customer satisfaction and fosters brand loyalty.

- Asset & Manpower Leverage: Operational efficiency is gained by co-locating the Sales, Service, and Spares functions, allowing for shared infrastructure, minimized overhead, and better deployment of highly skilled, certified manpower across the verticals.

- OEM Relationship & Expansion: LC's proven ability to execute the complete 3S customer journey at scale makes it a more reliable and attractive partner for premium OEMs, facilitating smoother territorial expansion and new brand tie-ups.

- Stable Revenue Base: The After-Sales income provides a stable and counter-cyclical revenue stream, mitigating the inherent cyclical volatility found in new car sales.

Actions to reduce employee costs

- Shared services model implementation: By establishing a centralized Shared Services vertical for non-core, brand-agnostic roles (HR, CRM, etc.), LC reduces organizational overhead and eliminates the duplication of administrative headcount across multiple dealerships.

- Resource allocation based on utilisation: The company drives down its labour-to-revenue ratio by rationalizing headcount underperforming outlets and reallocating skilled, trained staff to high-throughput locations based on efficiency benchmarks.

- Technology-enabled efficiency: LC lowers its dependency on manual labour and enables leaner sales/service teams by implementing digital CRM and lead management tools, thereby directly reducing frontline staff costs per customer interaction.

- Hiring freeze for non-revenue roles: LC maintains strict cost discipline by initiating a hiring freeze on all administrative and back-office (non-revenue) generating roles while selectively investing only in frontline sales and service advisors for high-growth brands.

Actions to reduce other expenses

- Dedicated overhead cost task force: LC drives cost discipline across the network by setting up a central task force to track and benchmark non-labour overheads (electricity, security, housekeeping) by outlet type and size.

- Energy efficiency optimisation: Implementation of LED lighting, energy-efficient HVAC, and smart power scheduling significantly lowers electricity bills across all outlets, particularly in high-cost urban

- areas.

- Outsourcing of non-core services: Standardizing and outsourcing non-core services (security, cleaning, etc.) to national vendors under fixed-rate contracts achieves economies of scale and reduces per-site overhead costs.

- IT and Process automation: Centralizing and digitizing back-office functions like payroll, inventory, and reporting via an ERP/DMS platform significantly reduces paperwork, administration hours, and the cost of manual reconciliation.

- Optimising insurance and marketing costs: Consolidation of third-party vendors for marketing and insurance facilitation under single fixed monthly contracts ensures scale without linear cost increases for customer acquisition services.

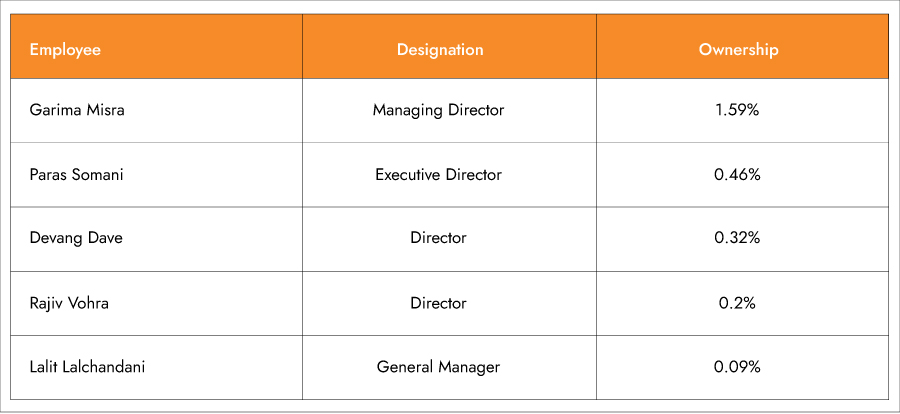

Employee Stock Option Plan

Landmark Cars utilizes ESOPs (Employee Stock Option Plans) as a core strategy to gain a human capital advantage in the competitive retail sector. The rationale focuses on retention, performance, and alignment:

- Talent Retention and Stability: The dealership business relies on skilled, experienced staff (technicians, sales experts). ESOPs, through vesting schedules, incentivize long-term commitment by requiring employees to stay with the company to realize the equity benefit. This stabilizes the workforce and minimizes costly attrition.

- Alignment of Interests and Empowerment: By giving employees a stake in the company, the ESOP directly aligns their personal financial goals with the company's long-term stock growth and profitability.

- Competitive Compensation: ESOPs serve as a powerful, non-cash compensation tool – helping Landmark attract and retain top performers at all levels, differentiating it from local competitors

- Boosting Performance Culture: The ESOP helps reinforce the company's culture of excellence and process adherence.

Substantial ESOPs given to employees

Recent Capex Spree

Landmark Cars recently completed a significant phase of capital investment and network expansion across FY24 and FY25. The focus of this strategy was the rapid scaling of its retail footprint and integration of new brands.

1. Capex Phase: Investment and Short-Term Cost

- Footprint Expansion: Landmark Cars invested heavily during FY24 and FY25, adding 43 new facilities (showrooms and workshops) with a strategic focus on high-growth markets such as Hyderabad and Jaipur. The average capex is ~INR 6 crore per combined sales and service outlet.

- Asset-Light Model: The expansion was executed using an asset-light, lease-over-own model (over 95% leased). This strategy conserves capital and supports the company’s higher RoCE focus.

- FY25 Cost Drag: The initial operational costs of launching these 43 new outlets resulted in aggregate PBT level losses of INR 400 Mn in FY25 from newly opened outlets. Capex per showroom is typically INR 30-60 Mn, and that of workshops is INR 20-40 Mn.

2.Segment Profitability and Recurring Revenue Base

The company's strategy ensures a growing base for its most profitable business segments, driven by its large network of workshops.

- High-Margin Service Revenue: The After-Sales Services and Spare Parts segment remains critical to profitability. Workshops operate at high EBITDA margins of 18-20%, substantially exceeding new car sales margins (1.7-4.0%).

- New Brand Service Base: The after-sales revenue mix for newly integrated brands (Kia, MG, and M&M) currently stands at 9% of their turnover. This contrasts with the higher ~17% mix achieved by LC’s established brands, demonstrating the gap that future maturity will address.

Robust Mid Management Structure

Landmark Cars Ltd.'s strong middle management is a critical asset, directly supporting the company's ambitious growth and ensuring high operational standards across its multi-brand dealership network.

Scalability and Network Expansion

- Scalable Operations: Middle managers, such as General Managers and City Heads, are empowered to make localized operational decisions, preventing bottlenecks at the top. This decentralized model is essential for the rapid opening and effective management of new outlets.

- Standardized Quality: They ensure consistent premium customer experience and disciplined execution of corporate strategy across all multi-brand, multi-location dealerships. This consistency is vital for maintaining brand equity and OEM partner trust.

- Seamless Integration: In the case of acquisitions, middle management is responsible for the quick and effective integration of new manpower, assets, and customer bases, ensuring acquired dealerships rapidly meet the company's financial targets.

Employee Empowerment and Retention

- Ownership Mentality via ESOPs: The Employee Stock Option Plans (ESOPs) align the interests of key employees, especially mid-managers, with shareholder value. This creates an 'owner's mindset' focused on long-term profitability and value creation.

- Talent Retention: ESOPs are a potent tool for retaining high-potential, experienced personnel in this critical layer, which is essential for business continuity and leveraging institutional knowledge.

Strategic and Financial Discipline

- Focus on High-Margin Segments: Mid-management efficiently runs and optimizes the high-margin after-sales service and spare parts business. Their operational effectiveness ensures this segment delivers stable, recurring revenue and significantly contributes to the company's overall EBITDA.

- Professional Governance: The long-tenured middle and senior management have ingrained a professional and process-driven culture. This discipline is crucial in a low-margin retail business, ensuring efficient inventory management and strong internal governance.

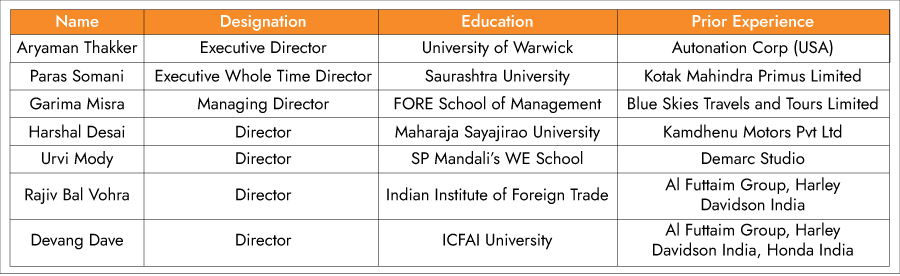

Landmark’s strong mid management pedigree

Landmark Cars trades at 9.5x TTM EV/EBITDA, compared to 12.0x for Popular Vehicles & Services Ltd. Landmark’s EBITDA has grown at a 19% CAGR over FY21–25, while Popular’s has remained largely flat. Moreover, Landmark’s ROCE of 8% exceeds Popular’s 5%. With a strong growth runway driven by new outlet additions, higher aftersales contribution, and proven execution capability, Landmark is well positioned to deliver profitable and sustained growth.