.jpg)

In this edition, we dive deep into this evolving ecosystem to capture:

- The Catalyst: The core reasons behind the surge in direct private deal-flow.

- The Reality Check: The critical risks inherent in bypassing professional fund structures to invest directly in unlisted entities.

- The Playbook: Actionable strategies to mitigate these risks and participate in private opportunities.

Private Equity & Venture Capital Investments Stagnating?

India's private equity and venture capital ecosystem has expanded dramatically over the past decade but is now showing signs of stagnation. Overall, Indian PE/VC deal flow reached approximately USD 43bn, with 2025 exhibiting a similar trend. Companies are thus exploring alternative pools of capital, which now include family offices and HNIs.

Exhibit 1: Annual PE/VC Investments in India (USD billion)

1776320039377.jpg)

Source: Bain Report India Private Equity Report, Ambit Asset Management

Note: Deals with undisclosed values are included in the count of deals but excluded from average deal size

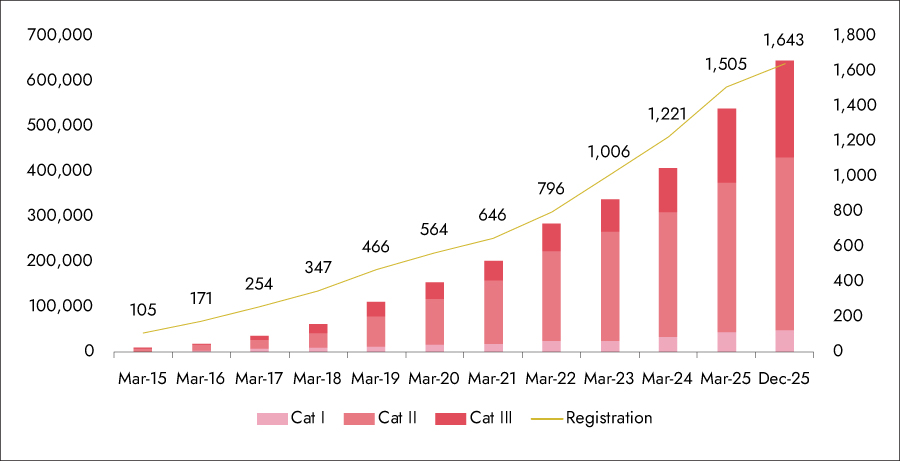

Exhibit 2: Rise of Capital Raised by AIFs in India over the Last Decade

Source: SEBI, Ambit Asset Management

Note: Capital raised in INR Crores

Exhibit 3: Growth in AIF Commitments: Domestic vs. Foreign

1776321687264.jpg)

Source: SEBI, Ambit Asset Management

Note - In thousand crores, Foreign Investors are inclusive of FPIs, FVCIs, NRI, Others

Case Study: NSE — India's Most Traded Unlisted Name

The National Stock Exchange (NSE) is arguably the single most written-about name in the Indian unlisted equity market. With a valuation of INR 5.37 lakh crore, a near-monopoly in equity derivatives, and an FY25 net profit of INR 12,188 crore (up 47% year-on-year), it represents a fundamentally exceptional business. NSE is increasingly being owned by non-institutions; this shift has picked up pace over the last six years. The rapid rise of small shareholders in NSE truly reflects the growing risk appetite amongst HNIs and Family Offices to participate in the unlisted capital.

Exhibit 4: Change in NSE’s Shareholding over the Years

1776320049202.jpg)

Source: NSE, Ambit Asset Management

NSE's shareholding base is already reaching 200,000 shareholders. In comparison, listed players in the Indian capital market infrastructure segment, like K-Fin Technologies and MCX, have about 250,000 shareholders. This massive increase in the number of shareholders symbolizes (a) intent to participate in the Indian capital markets boom, (b) ability to take risk of investing in illiquid businesses (relative to the listed segment) which are sizable, scalable and profitable, and (c) development of the over-the-counter market in India for unlisted companies.

Exhibit 5: Shareholder base across Key Market Institutions

1775801384782.jpg)

* as on 10 July 2023 (DRHP). **as on 23 Jul 2025 (RHP).

Source: Screener, NSE, Ambit Asset Management

NSE has led the way for savvy investors participating in the unlisted securities but has not been alone. Many companies that are listed or have filed DRHPs have a large public shareholder base as well.

Exhibit 6: Retail Participation Widespread among Pre-IPO & Listed Companies

1775801411170.jpg)

Source: SEBI, RHP/DRHP, Ambit Asset Management

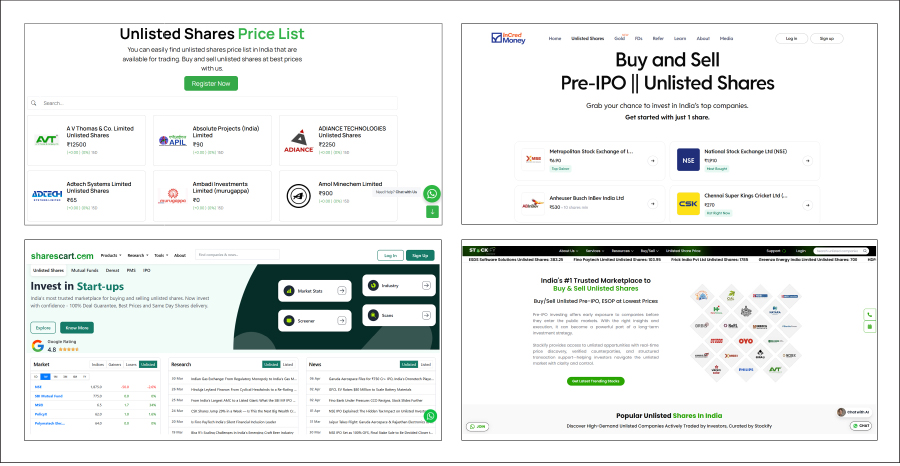

Whilst many of these companies have raised capital in multiple rounds from institutions, family offices, and UHNIs, the rapid rise in the number of small public shareholders can be ascribed to secondary sales of shares by primary fund raise participants, as well as employees who exercised their ESOPs. Unlike stock exchanges, which deal in listed securities only, there is no formal mechanism for dealing in unlisted securities. The over-the-counter trade of these securities mostly happens through intermediaries who specialize in these trades. A few intermediaries have also used digital channels to create a marketplace for these secondary markets.

Exhibit 7: Private Companies Market Place Websites

Source: Unlistedzone.com, Sharescart.com, Stockify.net.in, Incredmoney.com, Ambit Asset Management

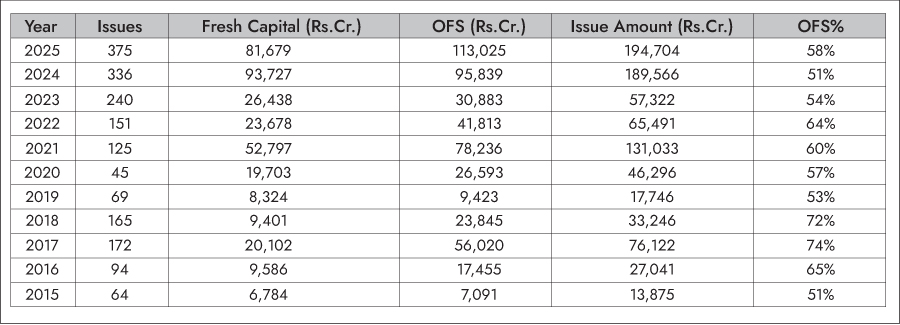

The IPO Exit Boom

The Indian IPO market has served as a critical exit route for PE/VC investors. The table below tracks IPO volumes, fresh capital raised, and Offer-for-Sale (OFS) proportions over the last decade — illustrating how the stock market has matured into a reliable liquidity window.

Exhibit 8: India IPO Market: Decade of Growth (2015 - 2025)

Source: Chittorgarh, Ambit Asset Management

- The trend of PE/VC-backed IPOs in India has accelerated in recent years, underscoring the increasing maturity and depth of the country's capital markets. Public listings are emerging as a preferred exit route for investors, as they often provide higher valuations and liquidity compared to private transactions.

- This shift reflects growing investor confidence in India's market ecosystem. IPOs can unlock significant value - particularly for early-stage investors who support companies through their formative growth phases - while also enhancing the credibility and visibility of portfolio companies.

- The year 2021 was pivotal, recording the highest-ever number of PE/VC-backed IPOs (USD 5.2bn across 44 IPOs). A decline followed in 2022 on account of sharp corrections in global equity markets amid rising inflation, rate hikes, and geopolitical conflicts.

- Years 2023 and 2024 saw a resurgence. 2024 recorded the second-highest number of PE-backed IPOs (41 IPOs), supported by buoyant Indian markets, stable economic conditions, and controlled inflation.

- Over the last five years (since 2020), PE/VC-backed IPO exits have realized USD 13.9bn across 158 IPOs. In terms of sectors, financial services recorded the highest volume and value, followed by e-commerce, technology, healthcare, and automotive - these five sectors collectively accounted for 70% of total PE-backed IPO value since 2020.

- PE/VC-backed IPOs now constitute a substantial and growing portion of India's overall IPO market, reflecting the positive evolution of the country's capital markets.

Exhibit 9: PE/VC-backed IPOs: Trend in PE/VC-backed IPO exits

1775801398971.jpg)

Source: EY IVCA Monthly PE-VC Roundup Report, Ambit Asset Management

Why Investors Invest In Private Markets?

Private markets have seen significant growth over the last decade. Most of that growth has been driven by institutional investors, largely due to a lack of access points for non-institutional investors. However, with more opportunities for private investors to access this area, demand is rising significantly. Investing in the unlisted securities has moved from a niche activity to a mainstream strategy for wealth creation in India. While they carry higher liquidity risk, the potential rewards often outweigh the constraints for patient investors. Here is why investors are increasingly allocating capital to unlisted companies:

1. Superior Returns (The "Alpha" Factor)

One of the top reasons investors are drawn to private markets is the potential for higher returns than public markets. Investors can prioritize maximizing returns, accepting slightly higher risk for the potential of increased performance. The 'illiquidity premium' and 'complexity premium' together can significantly boost returns for investors. The primary driver is thus the valuation gap. By the time a company hits the public markets (IPO), much of its exponential growth has often already occurred. Investing in unlisted space allows investors to capture value during the Growth or Late-Stage phases.

2. Diversification Beyond The Index

The public market is often heavy in specific sectors like Banking (BFSI), IT Services, Pharma & Healthcare, etc. The unlisted market, however, provides exposure to new-age sectors that aren't yet well-represented on the stock exchange, such as:

- E-commerce & D2C Brands

- Clean Energy & EV Infrastructure

- Specialized Manufacturing

Private investors have also been captivated by the potential to harness major secular trends like decarbonization, demographic shifts, and disruptive technologies — trends largely driven by private companies. Key current thematic opportunities include:

- AI Revolutin

- Aging Populations - biotech, healthcare services, and senior living

- Space-tech and Deep-tech

Private markets offer a much wider spectrum of opportunities than public markets, driven by companies staying private for longer and securing funding from private capital instead of going public.

3. Early Access To Future Blue Chips

Unlisted investing allows you to "own the future" today. Many of India’s current market leaders were once held exclusively by private investors for decades. By identifying high-quality companies with strong fundamentals and professional management before they go public, an investor position themselves as an early stakeholder in tomorrow's household names.

4. Influence and Information

For HNIs and Family Offices making direct investments, the unlisted space offers a level of engagement not possible in public markets. One may get:

- Information Rights: Access to detailed monthly/quarterly financial health beyond what public companies disclose.

- Strategic Input: In some cases, a seat on the board or an advisory role to help steer the company’s direction.

5. Institutional "Signal"

Many unlisted companies available to sophisticated investors are already backed by top-tier Global PE firms or Sovereign Wealth Funds. Investing alongside these giants provides a level of comfort that the company has undergone rigorous institutional due diligence.

Key Considerations For The Unlisted Space

Risks of Investing in Private Markets

The private market space, while offering genuine alpha potential, is structurally tilted against the uninformed investor. While the promise of "founder-like" returns is compelling, the private markets operate with a different set of gravity - one where capital can remain locked for years and transparency is often a luxury. Unlike the public markets, where liquidity is a click away, direct investments in unlisted companies are inherently illiquid, often requiring a 3 to 7 year horizon with no guaranteed exit window. Furthermore, the absence of centralized exchange means price discovery is subjective, and valuation gaps can be significant, leaving investors vulnerable to "information asymmetry" and governance lapses. From the sudden shifting of regulatory goalposts to the operational risks of a single-asset bet, navigating this space demands a rigorous due diligence framework and a stomach for volatility that public indices rarely test. We highlight few such core risks below:

- Liquidity & Exit Risk: There is no "ready market." There is no mechanism for real-time matching of buy and sell orders in the unlisted space. In periods of market stress, buyers vanish entirely. Unlike listed securities, where an investor can sell any day, an unlisted position can remain permanently locked. NSE itself was unable to provide its unlisted shareholders an exit for a long time due to regulatory reasons. Selling stake requires finding a willing private buyer or waiting for an IPO, which often comes with a mandatory 6-month post-listing lock-in period for pre-IPO investors.

The Indian private equity and venture capital ecosystem is currently facing significant liquidity challenges, largely driven by a higher bar for institutional-grade IPOs and a preference in capital markets for mature, profitable companies. Public market exits (which include IPOs) have plummeted from 40% of VC exits in 2022 to just 13% in 2024, and the median time for a startup to reach an IPO has lengthened from 10.5 years to 13 years.

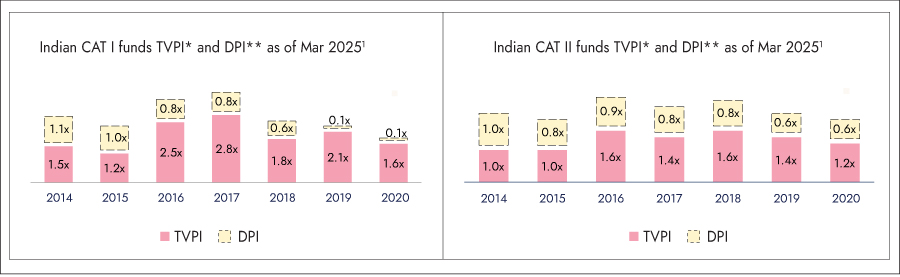

Because companies are staying private longer, a massive gap has formed between paper valuations (TVPI) and actual cash distributions (DPI). Only 8.9% of early, growth, and late-stage funds initiated between 2014 and 2020 managed to return their initial capital (achieving a 1.0x median DPI) after roughly 11 years. This severe lack of liquidity has made returning cash to Limited Partners (LPs) a top priority, with DPI now being considered the "new IRR". Ultimately, these delayed exits are starving the ecosystem of cash and making it significantly more difficult for managers to raise new funds.

Exhibit 10: Resulting in Growing Pressure on Funds to Return Cash to their Limited Partnership’s

Source: 1 CRISIL Intelligence – AIF Benchmarks (Total of 735 schemes across CAT I/II have been analyzed – Funds that did not provide adequate/required data were excluded)

Note: * TVPI – Total Value to Paid In Multiple: Net Asset Value to Paid In Capital; ** DPI – Distributed Value to Paid In Multiple: Distributed Capital to Paid In Capital; CAT I – VC, Social Venture and SME Funds; CAT II – Equity (Unlisted + Listed), Real Estate, Debt, Distressed Asset, Venture Debt Funds

India's DRHP pipeline is ballooning unsustainably, with closing numbers climbing from 58 at the end of FY24 to 197 by FY26 — a 3.4x surge that signals regulatory overload, creeping bottlenecks and market preference. New filings exploded to 219, yet closures lagged proportionally (dropping from 40% to 33% of total), while expirations and withdrawals spiked to 37 cases (11% vs. prior 4%), exposing heightened scrutiny. This growing backlog risks market clutter, which dilutes quality and stalls momentum as SEBI grapples with vetting the influx.

Exhibit 11: IPO Market Surge

1776320062375.jpg)

Source: Ambit Asset Management

- Absence of Regulatory Oversight: Unlike listed securities governed under SEBI's comprehensive framework, unlisted equity transactions occur over the counter between counterparties. There is no centralized exchange, no real-time price discovery, no mandatory disclosure norms, and no grievance redressal mechanism. SEBI explicitly clarified in December 2024 that electronic platforms facilitating transactions in unlisted securities of public limited companies are operating in violation of the Securities Contracts (Regulation) Act, 1956.

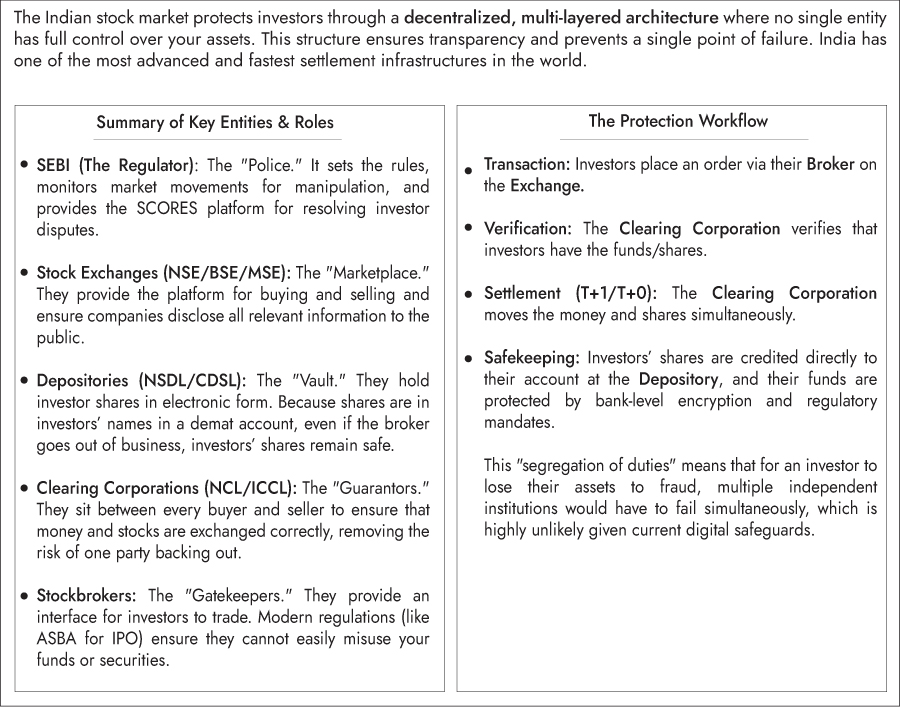

Exhibit 12: Investor Protection in the Listed Markets in India

Critical Risk: NSE's ISIN was not Activated until March 2025

NSE's ISIN Was Not Activated Until March 2025 For years, NSE's shares traded in the unlisted market through a cumbersome two-stage manual transfer process outside of CDSL/NSDL standard settlement. This meant that buyers had no depository-level protection on their holdings — a significant departure from how even other unlisted shares function. The ISIN was only activated for standard T+1 demat settlement in March 2025 pursuant to SEBI prescribing the framework for monitoring the shareholding norms of Market Infrastructure Institutions. Investors who transacted in NSE shares before this date were exposed to settlement risk that is simply not visible to retail participants.

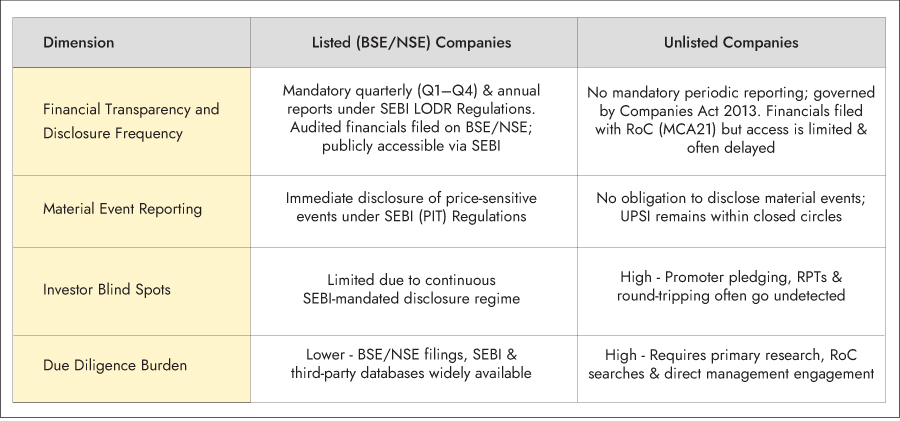

Information Asymmetry: Unlisted firms are not mandated to provide the same level of quarterly disclosures as public companies. Financial reports can be delayed, making it difficult to assess real-time performance.

Exhibit 13: Information Asymmetry - Public vs Private Markets

Source: Ambit Asset Management

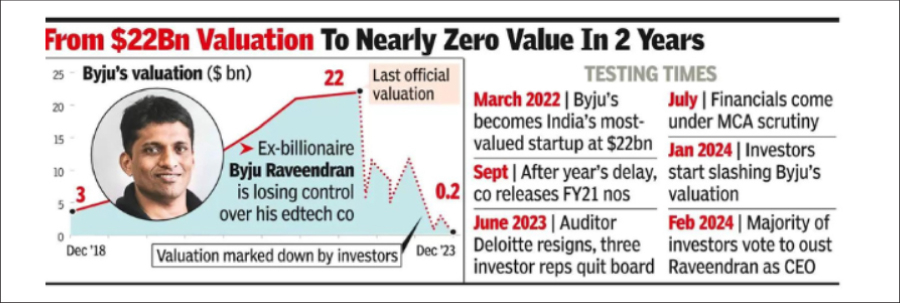

Exhibit 14: From India’s most Valued Startup to Crisis

Source: Timesofindia.indiatimes.com, Ambit Asset Management

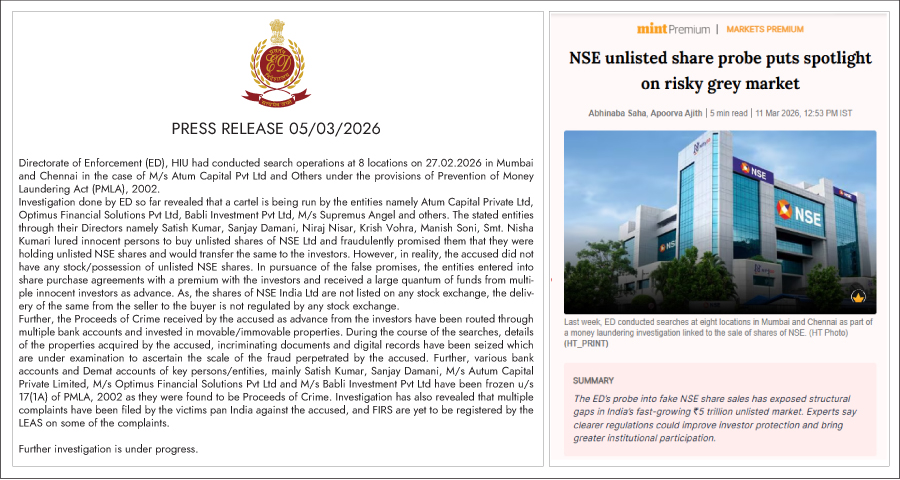

- Counterparty Risk: No Disclosure Obligations; Settlement Depends on Trust. Direct retail purchasers of unlisted shares receive no statutory information rights: no audited financials, no board disclosures, no regular updates. All information flows through informal broker relationships with conflicting incentives. Settlement is bilateral — the Atum Capital case (INR 115cr of NSE shares allegedly not delivered) demonstrates that even large transactions involving India's highest-profile unlisted security are not immune to counterparty failure.

Exhibit 15: ED Press Release NSE Scam

Source: Press Release, Director of Enforcement, India, Ambit Asset Management

- Valution Uncertainty: Without daily price discovery, valuations are often based on the most recent funding round. If the sector cools or the company misses a milestone, an investor’s "on-paper" value could evaporate without a clear benchmark. Unlisted share prices are set by market sentiment, rumors, and the seller's ask, not by any audited, independently determined valuation. Prices routinely move by double digits % with no underlying business trigger. A classic pump-and-dump dynamic operates: a coordinated network of brokers drives up the price via Telegram/WhatsApp groups, retail investors rush in, and early sellers exit.

- Concentration Risk: Direct investing often involves larger"ticket sizes" in fewer companies. Unlike a diversified PE fund, a single business failure can result in a total loss of principal for that specific allocation.

- Lock-in Risk: While IPOs are traditionally seen as the defining liquidity event for private investors, they carry a structural risk that is often overlooked. A mandatory six-month period following a listing during which pre-IPO investors are prohibited from selling their shares.

- Recent examples from the Indian market illustrate this clearly. Both Swiggy and Ola saw their stock prices surge sharply in the days immediately after listing, with Swiggy briefly approaching ~INR 600, before entering a prolonged decline in the months that followed.

The problem is one of timing. The six-month restriction coincides almost exactly with the period when stock prices are at their highest, leaving pre-IPO investors unable to sell during the most favorable window. By the time the lock-in ends and they are free to exit, prices have often already been corrected significantly. Investors who took on the most risk by entering early are thus structurally prevented from capturing peak returns — replacing one form of illiquidity with another, at the worst possible moment.

Unlike an IPO, where SEBI mandates a statutory lock-in — 18 months on 20% of promoter shareholding, 6 months on the rest, and up to 90 days for anchor investors — an AIF carries no such regulatory restriction. This means investors can capitalize on rising valuations and exit at an opportune time, a flexibility simply not available in an IPO. One is regulation-enforced, the other is trust-based.

Exhibit 16:The Lock-In Trap: Why Pre-IPO Investors miss the Peak

1775801427998.jpg)

Source: Investing.com, Ambit Asset Management

How to Mitigate these Risks?

Managing a direct private portfolio requires moving from a "trading" mindset to a "structuring" mindset:

1. Staged Due Diligence: Go beyond the pitch deck. Request audited financials for the last 3 years, verify the cap table, and conduct independent promoter background checks.

2. Right-Sized Allocation: Treat unlisted securities as a "satellite" portfolio. Most sophisticated investors cap this exposure at 5% to 10% of their total equity allocation to ensure the bulk of their wealth remains liquid.

3. Governance Rights: When investing significant capital, negotiate for information rights or observer seats to stay informed of pivot points before they become crises.

4.Portfolio Diversification: Avoid "sector-tunneling." An investor could spread the direct bets across 5 - 10 companies in different industries to mitigate the impact of a single company / sector failing.

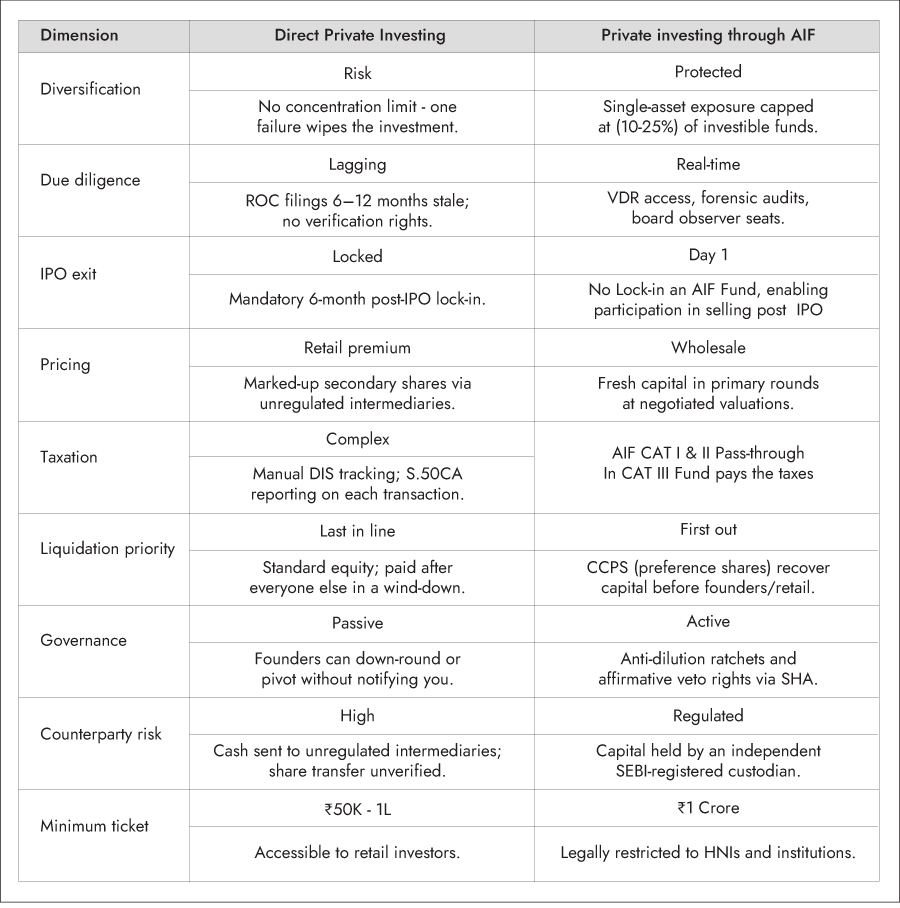

5. Fund vs DIY: Investors seeking exposure to the unlisted equity asset class, the choice of vehicle matters as much as the choice of company. The table below outlines structural differences between retail direct investing and a Category II AIF fund approach - with specific regulatory and legal references.

Exhibit 17: Advantages of Fund Structure over DIY Investments

India's pre-IPO landscape presents a compelling and still-nascent opportunity for discerning investors. Yet opportunity, absent the appropriate regulatory governance framework, is indistinguishable from risk. The evidence presented across this edition points to a singular conclusion: those who have participated most profitably in India's unlisted equity story have done so through investment vehicles underpinned by rigorous due diligence, enforceable legal protections, regulatory oversight, and incentive structures aligned with investor outcomes.

The choice of vehicle is not incidental to investment performance - it is foundational to it. In a market defined by information asymmetry and uncertain exit timelines, the discipline of how one invests is every bit as consequential as the decision of where to invest.

Opportunity in Adversity?

After navigating the complexities and risks of the unlisted market, a natural question emerges: Where should a patient, informed investor be looking right now? The answer, perhaps surprisingly, points back to listed equities. And the timing appears more compelling than it has been in years. Global markets have been rattled by the US-Iran conflict, triggering a broad selloff across equities and commodities. Indian markets have fallen 8.2%, and FII outflows persist across most emerging markets. Yet history shows that across 9 major geopolitical events, markets recovered within an average of 38 days. Furthermore, after every 18–19 month dull period, the Nifty 50 has delivered positive returns 100% of the time in the following 12 months—suggesting the current turbulence may be precisely the kind of adversity that creates opportunity.

On the fundamental side, the case for India looks increasingly compelling. Valuations have corrected significantly nearly 48% of stocks now trade below their 10-year average PE and earnings are finally being upgraded after 7 straight quarters of downgrades. India's valuation premium over broader EM has collapsed from 66% to just 14%, making it attractively priced relative to history. Combined with India's well-diversified market structure and its long-term outperformance over EM (10-year CAGR of 7.2% vs 5.6%), the overwhelming weight of evidence points to this being a strong entry point for long-term investors.

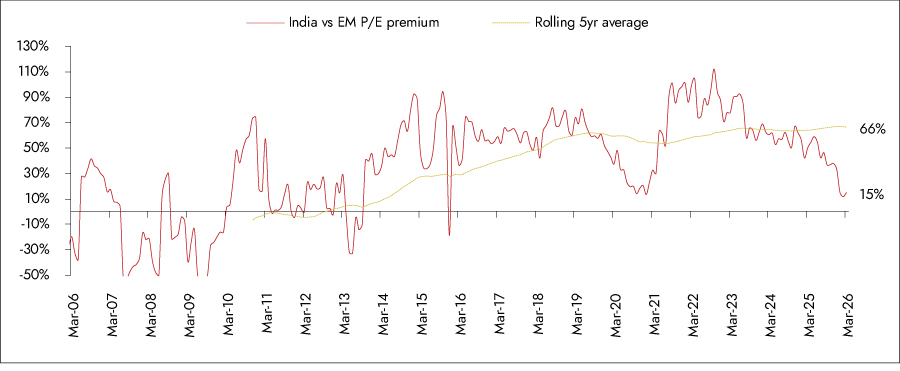

For most of the last decade, investing in India commanded a premium - and rightly so. Strong economic growth, a large domestic market, and consistent corporate earnings justified paying more than other emerging markets. But today, that premium has fallen well below its 5-year average. This has only happened twice before - during the uncertainty of COVID in 2020, and briefly in 2013. On both occasions, investors who stepped in were rewarded. Global investors appear to be underpricing India relative to its long-term potential, and historically, that gap has not stayed open for long.

Exhibit 18: India's Valuation Premium over EM is below 5 Year Average (last time it was during COVID and before that in 2013).

Source: MOSL, Ambit Asset Management

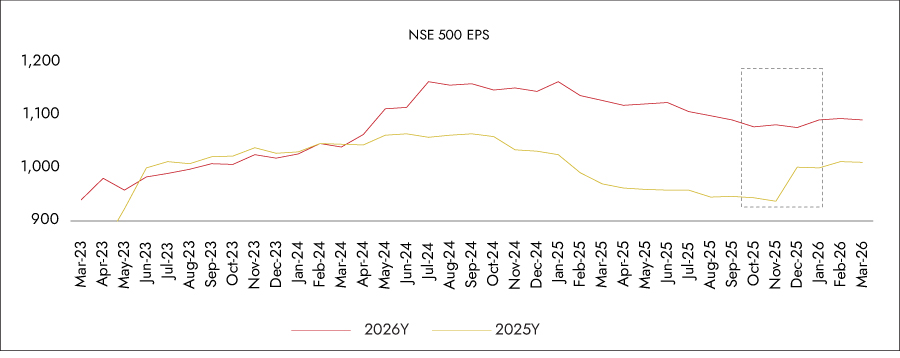

Corporate earnings in India went through a prolonged difficult stretch — seven consecutive quarters where results disappointed expectations. That is a long period of reset. But Q3FY26 marked a meaningful turning point, with earnings finally recovering. This matters because markets typically begin to move before the recovery is fully visible. Investors who wait for confirmation often miss the early and most rewarding part of the cycle. The window between when earnings begin to recover and when prices fully reflect that recovery is historically one of the best times to be invested.

Exhibit 19: Earnings Rebounded in Q3FY26 after 7 Quarters of Downgrades, Signalling a Strong Uptick in Earnings for FY27 and FY28

Source: Ambit Capital Research, Ambit Asset Management

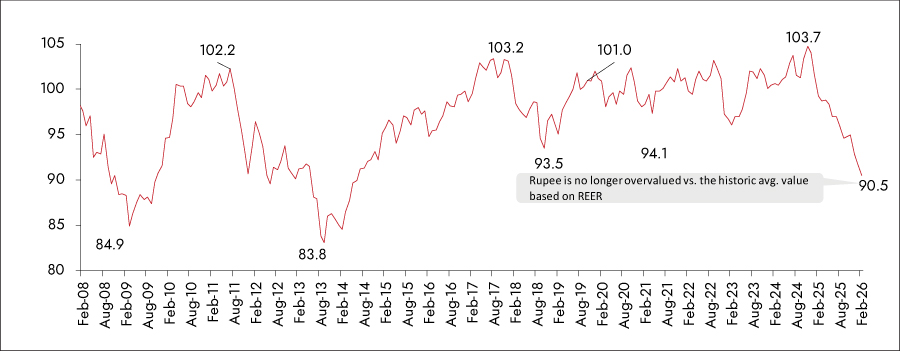

Currency movements tend to be slow and then sudden. The Rupee has weakened over the past 18 months, but that weakness is increasingly looking like a setup for a reversal. A measure that tracks the Rupee's real value against a basket of global currencies - adjusted for inflation - currently suggests it is undervalued by approximately 5% relative to its historical average. We have seen this before. Similar currency stress preceded sharp recoveries in Indian markets after the Global Financial Crisis in 2008-09, the refinancing crisis of 2013, and the financial sector stress of 2018-19. Each time, foreign investors returned in significant numbers and markets responded strongly. The conditions today bear a close resemblance to those periods.

Exhibit 20: The Currency is Positioned for a Recovery

Source: Ambit Capital Research, Ambit Asset Management

A Large Part of the Market is Available at Attractive Prices:

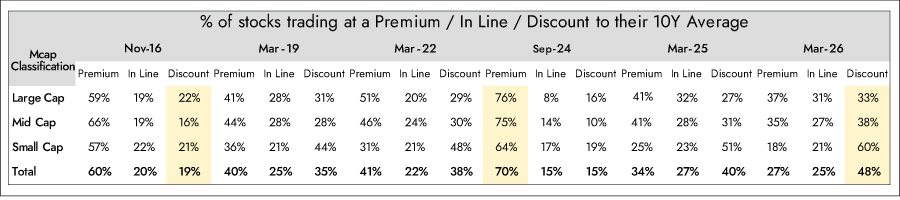

Perhaps the most tangible signal — nearly half of all listed stocks, concentrated particularly in the mid and small cap space, are currently trading below their 10-year average prices. These are not distressed or struggling businesses. Many are fundamentally sound companies that have been caught in a broader market correction. When quality businesses become available at below-average prices, it is not a warning sign. It is an opening.

Exhibit 21: Valuations have become most Attractive Recently. Nearly 50% of Stocks (Primarily In Mid And Small Caps) are Trading below their 10Y Average

Source: Avendus Spark, Ambit Asset Management

Every market cycle throws up moments where the risk-reward balance shifts in favour of the patient investor. Today, several factors are converging at the same time — valuations have corrected, earnings are recovering, and the currency appears poised for a reversal. For investors willing to look beyond the noise, the public markets are quietly presenting one of the more compelling entry points seen in recent years.

Ambit Coffee Can Portfolio

The Ambit Coffee Can Portfolio pursues long-term wealth creation through a large-cap biased, discretionary strategy centered on high-quality, "all-weather" companies with enduring competitive edges. Its core theme emphasizes the "Quality minus Junk" philosophy, favoring resilient franchises that boast pricing power, conservative balance sheets, exceptional management, steady revenue streams, and robust capital efficiency to sustain growth across cycles.

It targets firms in their "Sweet Investment Zone," that high-growth lifecycle phase offering valuation re-ratings, downside shields, and muted volatility, curating a concentrated portfolio that commands a fair premium for lasting superiority.

This approach suits patient investors seeking cycle-resilient, risk-adjusted outperformance, balancing a moderate risk profile - rooted in market swings and discretionary calls - with inherent protection from disciplined quality filters, ideal for those valuing enduring value over fleeting gains.

Ambit Good & Clean Midcap Portfolio

The Ambit Good & Clean Midcap Portfolio navigates polarized markets through a strategic shift from a rigid mid-cap focus to a market-cap agnostic, agile approach that has begun delivering meaningful alpha. Its core theme revolves around "Good and Clean" principles - selecting resilient franchises with exceptional capital efficiency, quality management, and robust governance to drive superior risk-adjusted returns.It employs an evolved framework structured around four distinct investment themes: exploiting market underestimation, capitalizing on inflection points from capex and policy shifts, embracing high-growth new age businesses, and prioritizing bottom-up quality leaders with proven models.

This portfolio suits patient investors seeking outperformance across cycles. It balances a moderate risk profile—stemming from market volatility and strategic shifts—with downside protection through disciplined qualitative filters that emphasize enduring franchises and governance strength, making it ideal for those prioritizing long-term value over short-term stability.

Ambit Micro Marvels Portfolio

Ambit Micro Marvels Portfolio embodies an anti-consensus theme, targeting overlooked micro-cap marvels in niche oligopolistic markets that boast deep moats and immense scaling potential into future market leaders. Its standout features include the proprietary "Good and Clean" framework to pinpoint companies with exceptional capital allocation and governance, the scuttlebutt approach to reveal authentic business strengths beyond management commentary—and a firm commitment to low leverage, curating 20-25 resilient, high-growth stocks for superior long-term, risk-adjusted performance.

Suited for patient, high-conviction investors like family offices and HNIs who embrace micro-cap volatility, the portfolio's risk profile balances inherent uncertainties through disciplined qualitative filters that protect downside while chasing transformative upside across cycles.

Ambit Pricing Prowess Fund

Ambit Pricing Prowess Fund is an All-weather, Open-ended, Long-only, Category III, Flexi-cap AIF – a meticulously crafted opportunity for long-term investors seeking:

- Accelerated Portfolio Returns: The ability to raise selling prices faster than input costs (inflation) directly increases profit margins and accelerates Free Cash Flow (FCF) growth.

- Unrivaled Portfolio Resilience: Pricing Power acts as a structural defense mechanism, stabilizing margins even during periods of macro pressure, supply shocks, or weaker demand.

- Maximum Long-Term Value Creation: Pricing Power is a proxy for an irrefutable competitive advantage (deep moat).

In a market of highly varied valuations, Ambit Pricing Prowess Fund is not constrained by a single market segment. We are designed to seek the most attractive combination of Quality and Price across the entire investment universe.

We can shift capital fluidly between Large, Mid, Small, and even a select number of carefully vetted unlisted businesses. This broad mandate allows us to find and capitalize on unique opportunities that align with our core framework.

Our focus is more on business fundamentals, rather than stock price movements. We do not seek comfort of the crowd and seek exposure to companies that are "unrecognized" because the market either misprices the longevity of their growth or fails to fully appreciate the structural defense their pricing power provides.

The framework's final structure—blending Established (proven track record, mature moats) and Emerging (new, rapidly widening moats, higher growth potential) Pricing Power plays—provides a balanced approach to capture both resilience and accelerated return potential within the portfolio.

Investing in businesses with Pricing Prowess offers compelling advantages, as below:

- Proven Inflation Hedge

- Maximized Profit Margins

- Stable, Quality Compounding (non-Glamorous)

- Formidable Entry Barriers

- Long-term Value Creation