We at Ambit are constantly trying to stay ahead of the curve by drowning out the noise and looking ahead. In keeping with our long term investment thesis, we like to stay up to date with not just the present impediments faced by your portfolio companies but also long term disruptions which can hit these companies. Hence we will regularly come out with our thoughts on disruptions in your portfolio companies/ sectors and for the 18th volume of this series we have selected IndiaMart Intermesh – Digitizing MSME

A disruptive technology/ innovation is one that helps create a new market and value network, and eventually goes on to disrupt an existing market and value network, displacing conventional wisdom or technology. This note takes a closer look at how IndiaMart Intermesh has successfully navigated multiple challenges and how it is placed in light of probable future disruptions in an ever changing technology led world.

IndiaMart Intermesh: Journey of Digital Transformation

IndiaMart, founded in late 1990s by Dinesh and Brijesh Agarwal, started out as an online directory of exporters. The company was largely successful and remained one of the few surviving and profitable digital businesses post the 2000 Dot-com Bubble. However multiple challenges due to global events such as 9/11 and 2008 GFC compelled IndiaMart to look at domestic market which was aided by improving internet access in India. IndiaMart, thus, pivoted to a B2B classifieds model.

IndiaMart is a digital B2B market place which connects prospective buyers to sellers and vice-versa. Prospective buyers visit IndiaMart to fulfill their purchase requirements and IndiaMart helps them in getting the relevant suppliers. The monetization happens on the suppliers’ front where subscribers pay a subscription fee for access to leads. Due to the subscription based revenue model, IndiaMart works on a negative working capital model.

Over the years, IndiaMart has transitioned from primarily providing RFQs (Buy Leads) to suppliers to providing augmented services such as Price Discovery, Customer Relationship Management (CRM) and Order Management System. The use of technology such as behavioral matchmaking for better fulfilment of leads, multi-language search and supplier reviews has also resulted in optimized matchmaking and user experience.

This has helped IndiaMart become the largest B2B player in India with 1bn+ website hits in FY22. (Exhibit 1)

Exhibit 1: IndiaMart is a market leader in the B2B marketplace and fares the highest amongst most key metrics

Source: Ambit Asset Management, Company. Note: For Traffic and UBE data is for FY 22. For all other metrics data is as on June 30, 2022.

Success Factors for IndiaMart – Secret code for the largest market share?

1. Building a robust Marketplace – On-boarding of Buyers and Suppliers and seamless interaction between them is key to building a robust marketplace. IndiaMart has been able to execute all of the same which makes it extremely difficult for competition to enter and replicate the same. This also results in IndiaMart enjoying economies of scale as their platform develops and evolves.

- Network Effect – An average enterprise in India is present only across ~2-3 online platforms. Thus, an on-boarded supplier provides great competitive advantage as newer competition will collectively find it difficult to get suppliers on their platform.

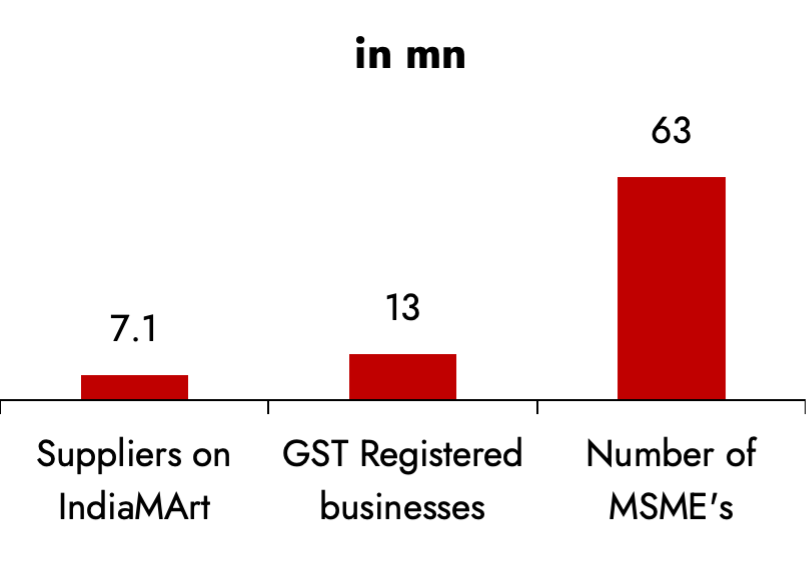

- Large untapped supplier base – IndiaMart has ~7.1 million suppliers and has on-boarded >4.8 million suppliers over the last 6 years. Currently India has ~13 million GST paying businesses (of ~63 million MSME’s) which is the target market for most internet based B2B players in India. There still lies a large untapped market for MSME’s not having an internet presence, yet. (Refer Exhibit 4).

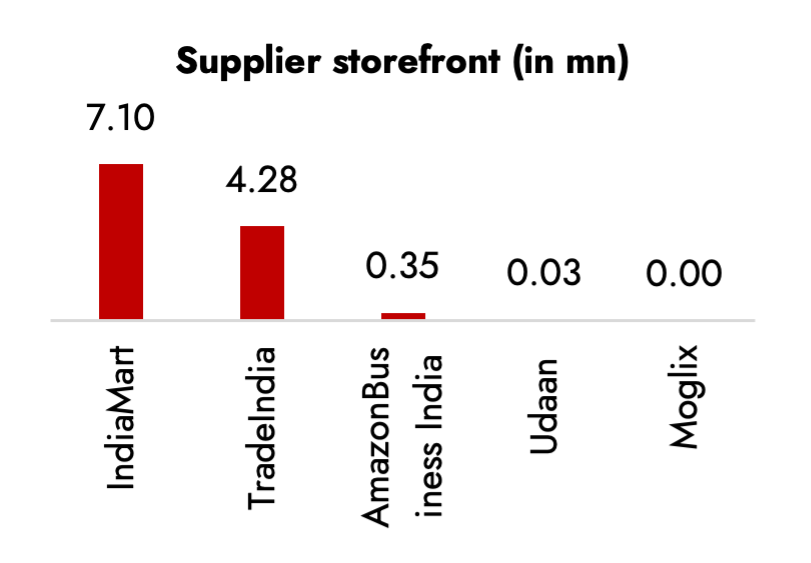

- As highlighted in Exhibits 2 & 3, IndiaMart has the largest database of addressable suppliers amongst comparative peers. As internet penetration for SME businesses widens, the higher number of supplier fronts should result in a better competitive advantage.

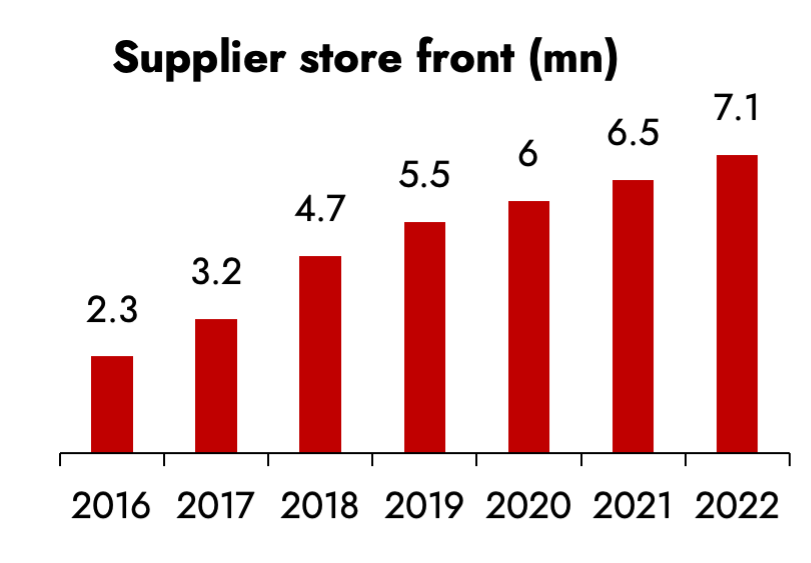

Exhibit 2: IndiaMart has added suppliers at a staggering space

Source: Ambit Asset Management, Company

Exhibit 3: …and comfortably has the highest number of suppliers

Source: Ambit Asset Management, Company

Exhibit 4: …while there still remains a large untapped market for MSME’s

Source: Ambit Asset Management, Company, TradeIndia

2. On-boarding of buyers/ users: The second leg of building a marketplace is getting buyers/users on the platform. Buyers usually tend to flock where there are larger number of suppliers as it tends to coincide with higher fulfillment rate.

Higher number of suppliers bring in higher number of buyers and vice-a-versa which results in a self-reinforcing fly wheel which results in a stronger platform.

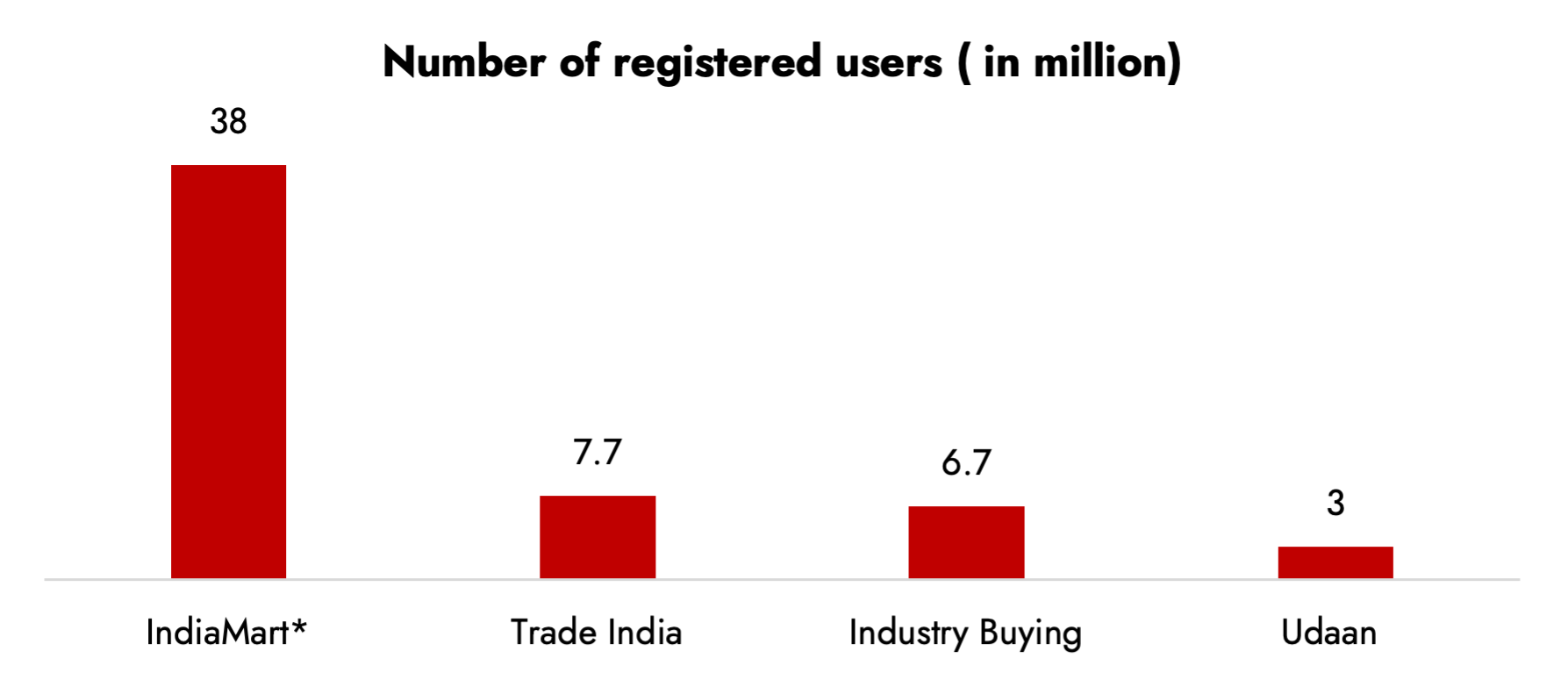

IndiaMart has the highest number of registered buyers and even on an active buyer basis the company has ~37million buyers, which is ~20x higher than any competitor in the space. The higher number of buyers and sellers thus bring out a network effect which results in strengthening of the marketplace model.

One example of superior network effect can be seen in stock exchanges where NSE commands >85% />95% market share in Cash/Derivatives and despite heavy investments by BSE to garner back some market share, they have been unable to do the same due to strong network effects in NSE.

Exhibit 5: IndiaMart comfortably has the highest number of registered users in the B2B e-commerce space

Source: Ambit Asset Management, Company

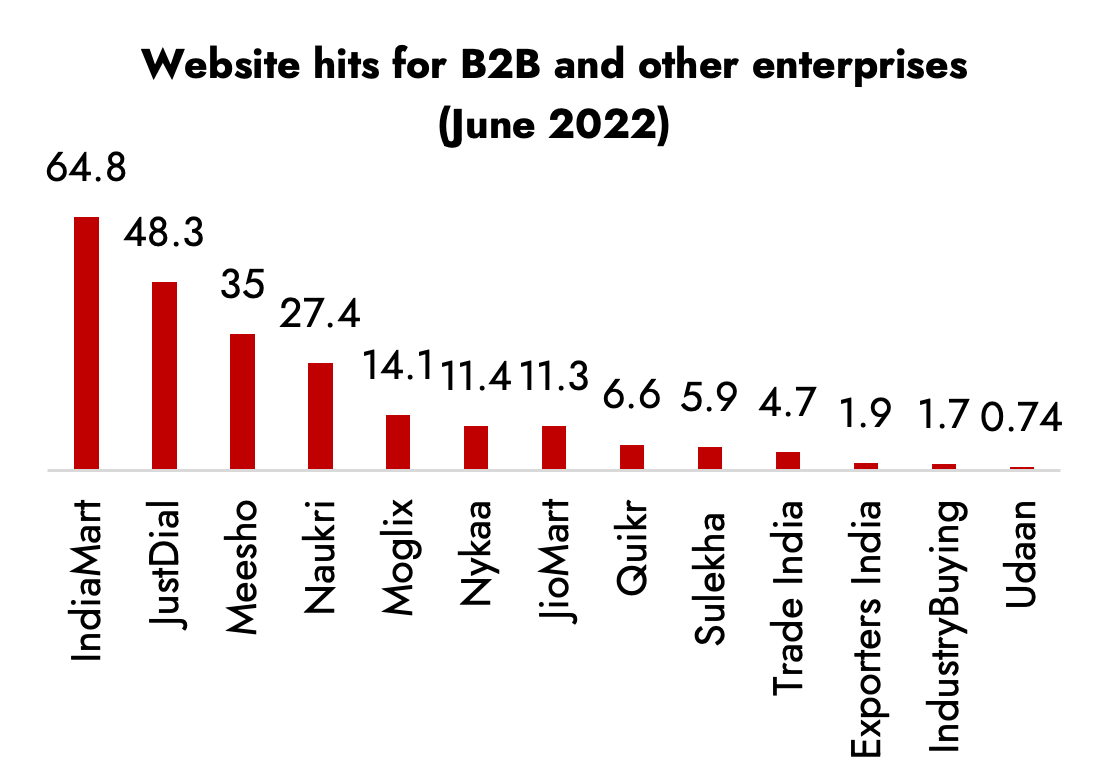

3. Interaction between buyers and sellers: Once both buyers and sellers are on-boarded the interaction between them is paramount for monetizing the platform. Website hits is a correct metric to assess the same.

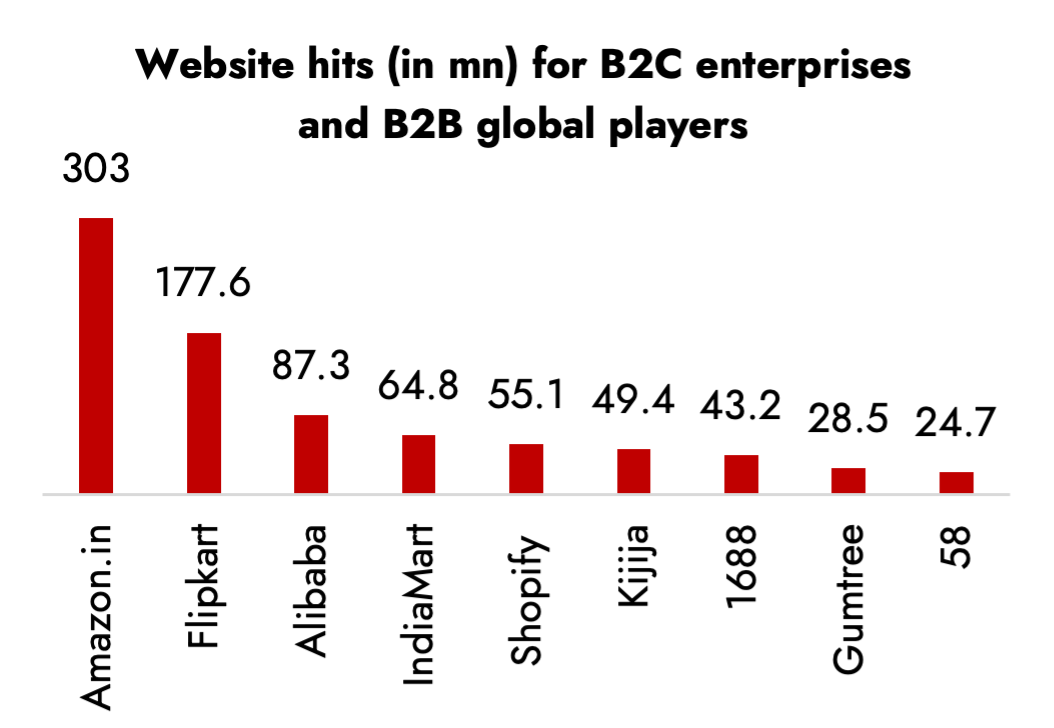

When compared to other internet companies both B2B and non-B2B, IndiaMart stacks up extremely well in terms of website hits which showcases the extent of activity on the platform (Exhibit 6). IndiaMart’s platform generates more traffic than most other B2B enterprises – domestic and globally – barring Alibaba (Exhibit 7).

Higher website traffic results in additional data generation and better sense of user and supplier behavior resulting in better lead-matching and in-turn better fulfillment rates resulting in strengthening of competitive advantages.

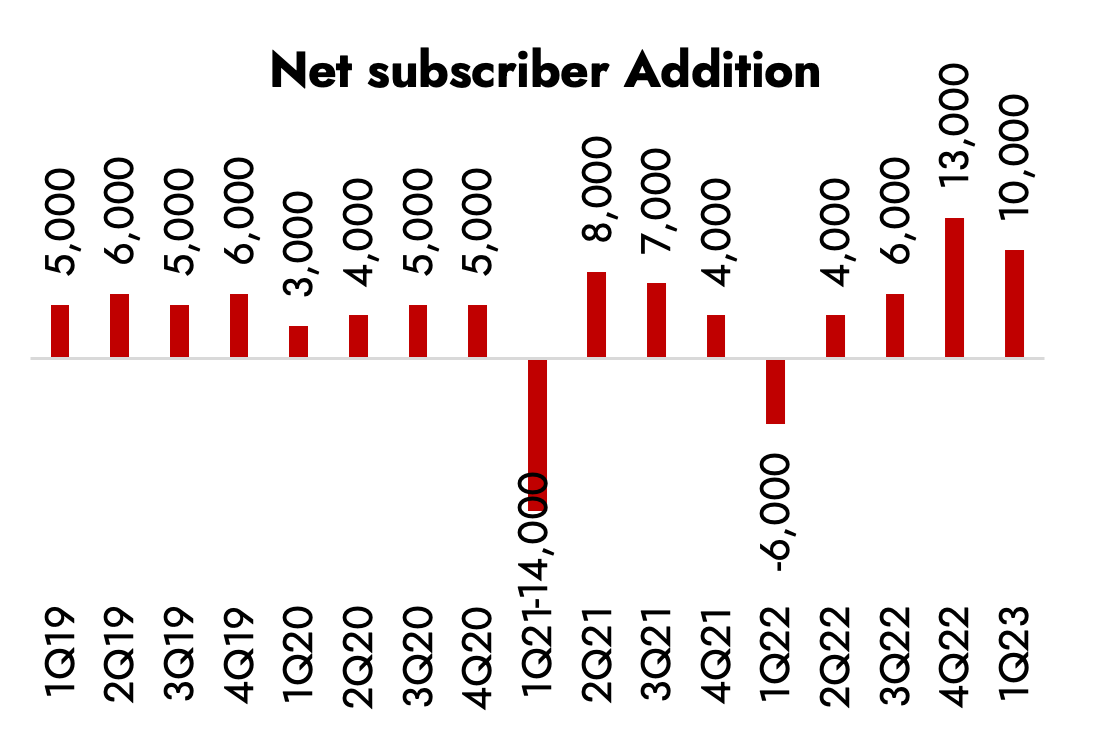

Exhibit 6: Growth in subscribers has been steady for IndiaMart barring 2 covid waves

Source: Ambit Asset Management, Company

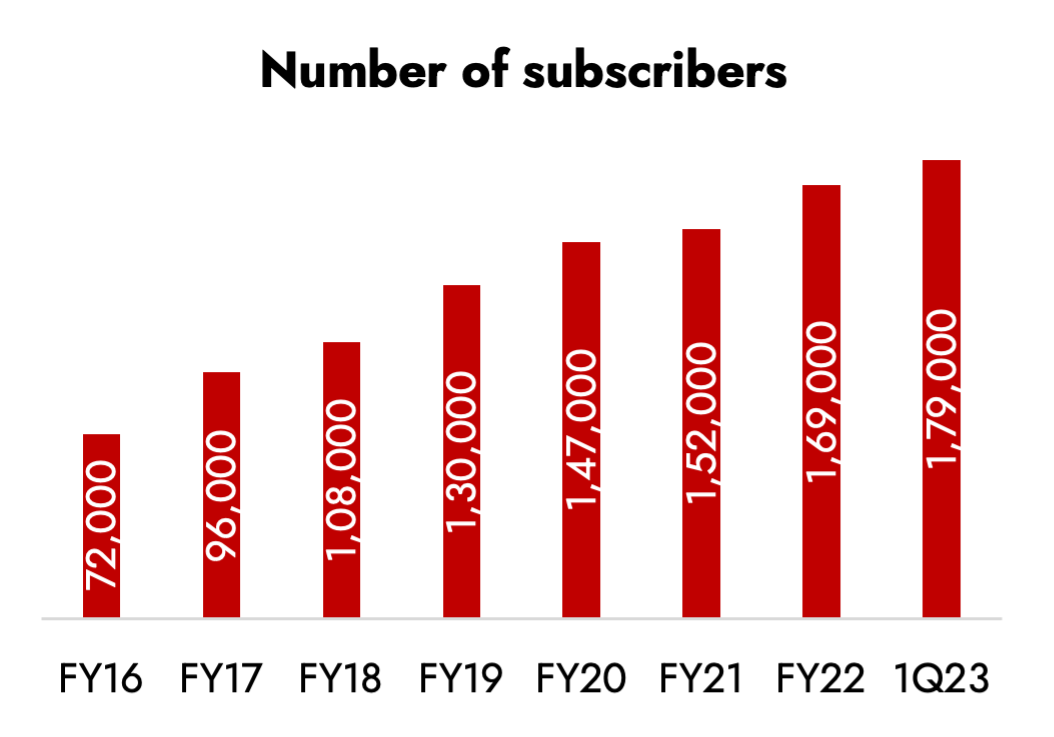

Exhibit 7: IndiaMart despite covid has managed to add subscription at ~15% CAGR despite covid waves

Source: Ambit Asset Management, Company

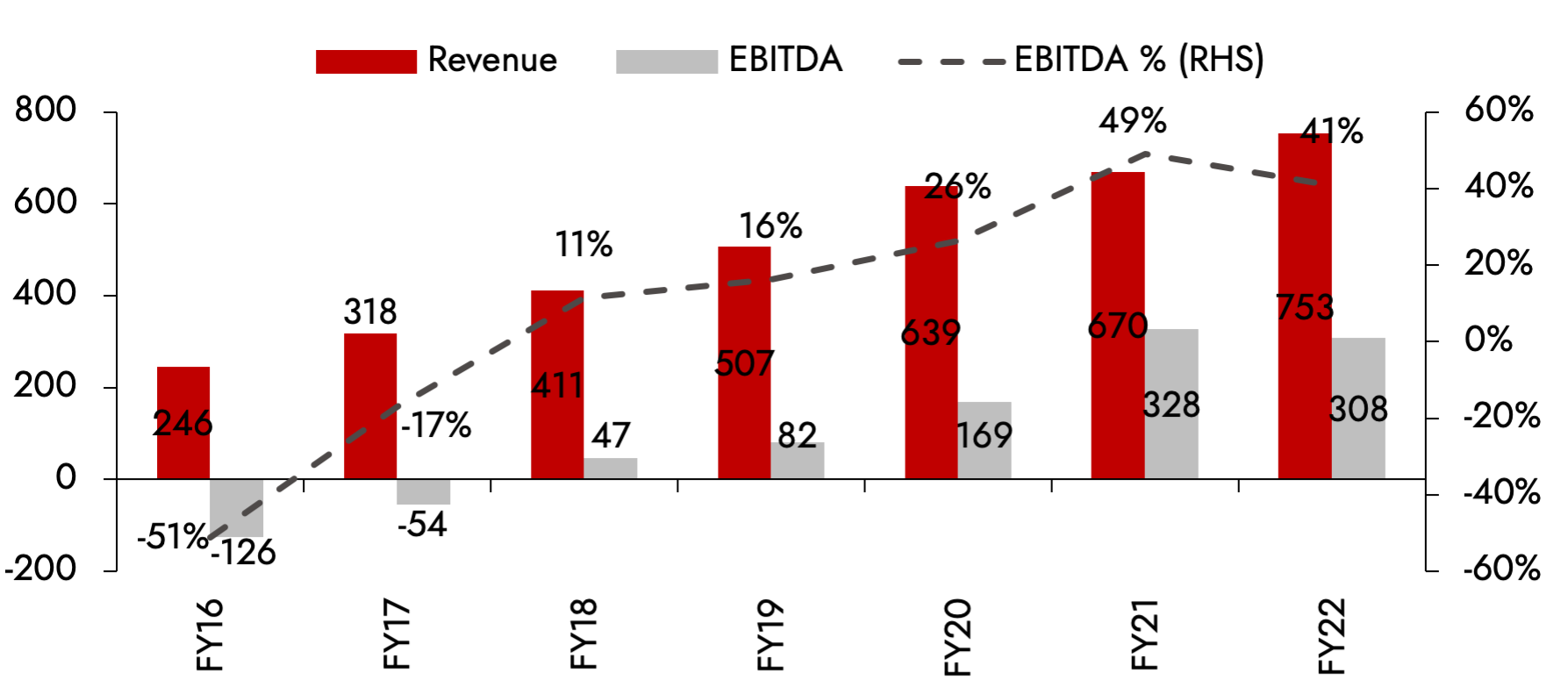

On the back of the same, IndiaMart has leveraged the strong network and has been able to execute the monetization of the platform. The same can be seen with revenues almost growing 3x from FY 16-22 and EBITDA margins seeing around a ~90% delta across the last 6 years (-51% in FY 16 to 41% in FY 22).

Exhibit 8: IndiaMart’s monetization of the platform and scale benefits can be seen in the revenue / EBITDA trajectory

Source: Ambit Asset Management, Company

In the longer run, as the network and scale benefits grow stronger, IndiaMart should be further able to strengthen economic moats while incorporating operational efficiencies.

Disruption Points -

1. Inability to add and retain subscribers – Converting existing suppliers into paid subscribers and keeping them on the platform is essential for IndiaMart to scale its business.

Inability to add or retain subscribers is a key disruption point which can derail the business. Moreover, controlling churn, especially in the lowest subscription tier (Silver Monthly) where it is ~5% per month, while adding additional customers will be an important factor for the AMC.

In addition to the same, any major economic event or distress in MSMEs can result in inability to retain subscribers/ loss in subscribers as seen during 1st / 2nd waves of covid. Current subscriber base of ~179k has grown at 15% CAGR over the last 6 years, despite covid led challenges. IndiaMart continues to add subscribers at ~8-9k per quarter (Exhibit 9 & 10). Any issues in subscriber addition in the future or macro-economic headwinds may result in slowdown in subscriber addition.

Exhibit 9: Subscriber growth for INMART has been steady barring the two COVID waves…

Source: Ambit Asset Management, Company

Exhibit 10: …but despite that, it has managed to add subscribers at ~15% CAGR over the last 6 years

Source: Ambit Asset Management, Company

2. Inability to provide value added propositions – IndiaMart primarily generates revenue via selling RFQs or buyer leads to paid suppliers. The subscription based model still contributes to 95% of total business.

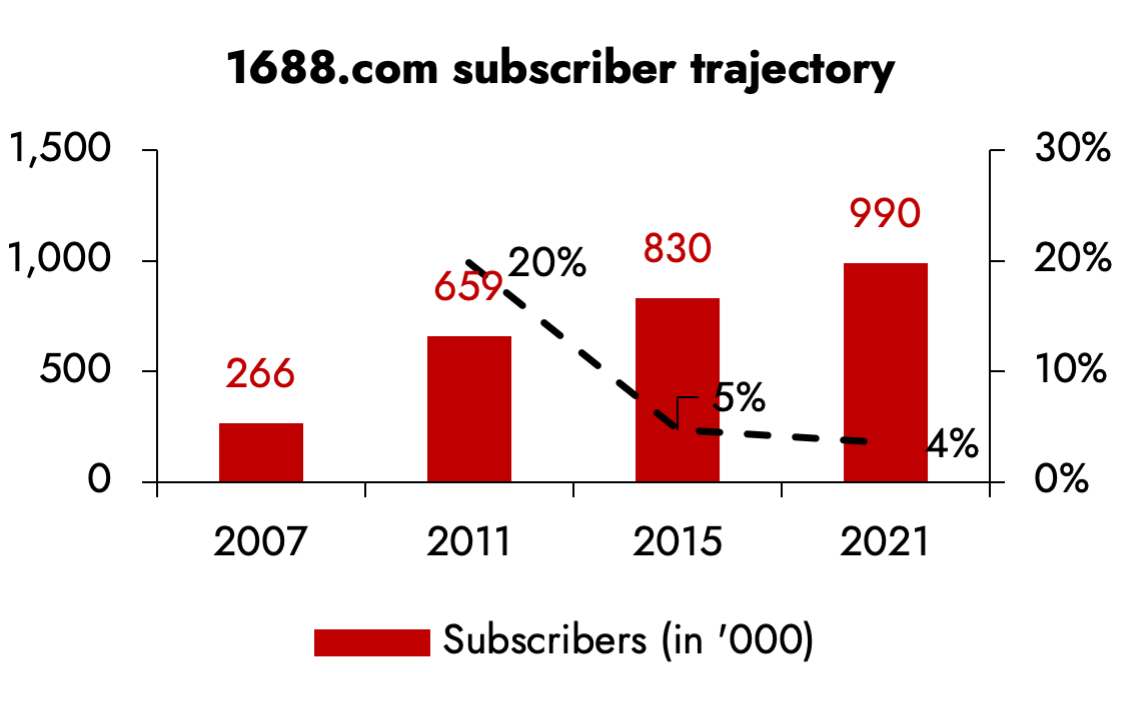

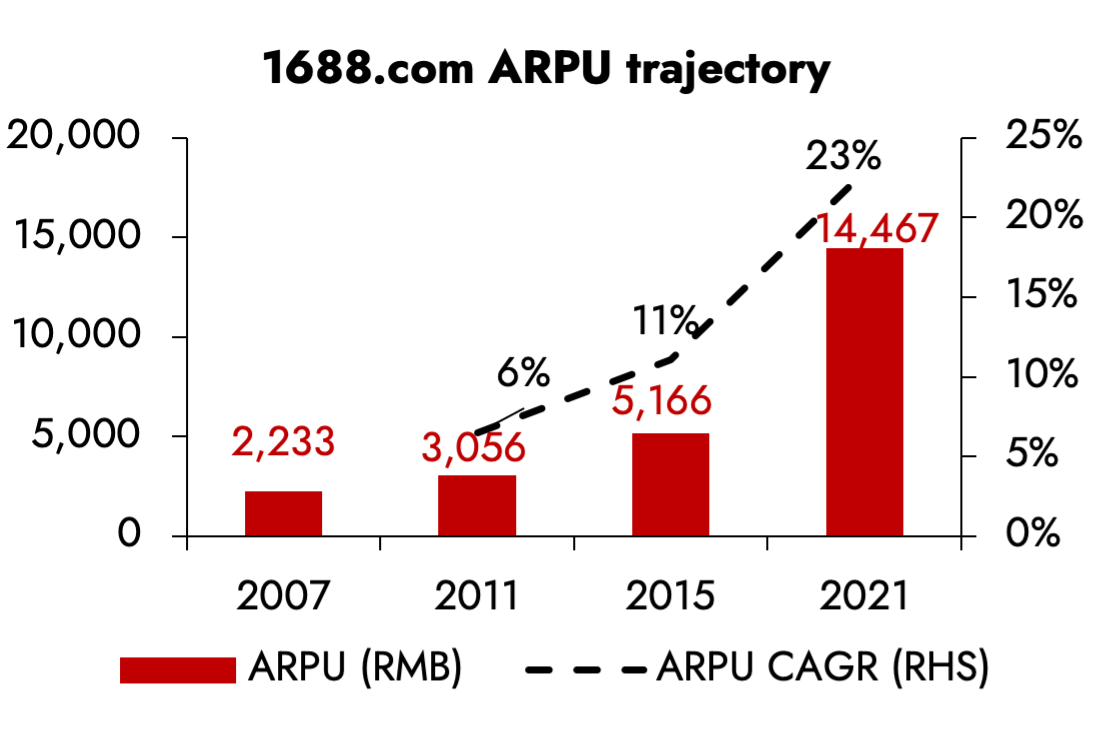

Taking cue from global peers – Global peers such as 1688.com (a subscription based B2B player similar to IndiaMart) have been able to maintain growth rates (>20%) even while subscriber addition has been moderate primarily because of adding value added services on top of buy leads.

1688.com now provides value added services ranging from premium data analytics, upgraded storefront management tools and customer management services such as marketing services. The share of value added services now accounts for ~50% of total revenues for 1688.com. This maturity in business model came when subscriber slow-down was more than offset by providing value added services which resulted in company continuing its revenue growth trajectory (Exhibit 11 & 12)

Exhibit 11: As growth in subscribers started to taper down for 1688.com …

Source: Ambit Asset Management, Company

Exhibit 12: … the ARPU trajectory picked up led by increase in value added services

Source: Ambit Asset Management, Company

Similarly, Shopify, too provides Value Added Services such as automation, shipping and payments services on top of product sale.

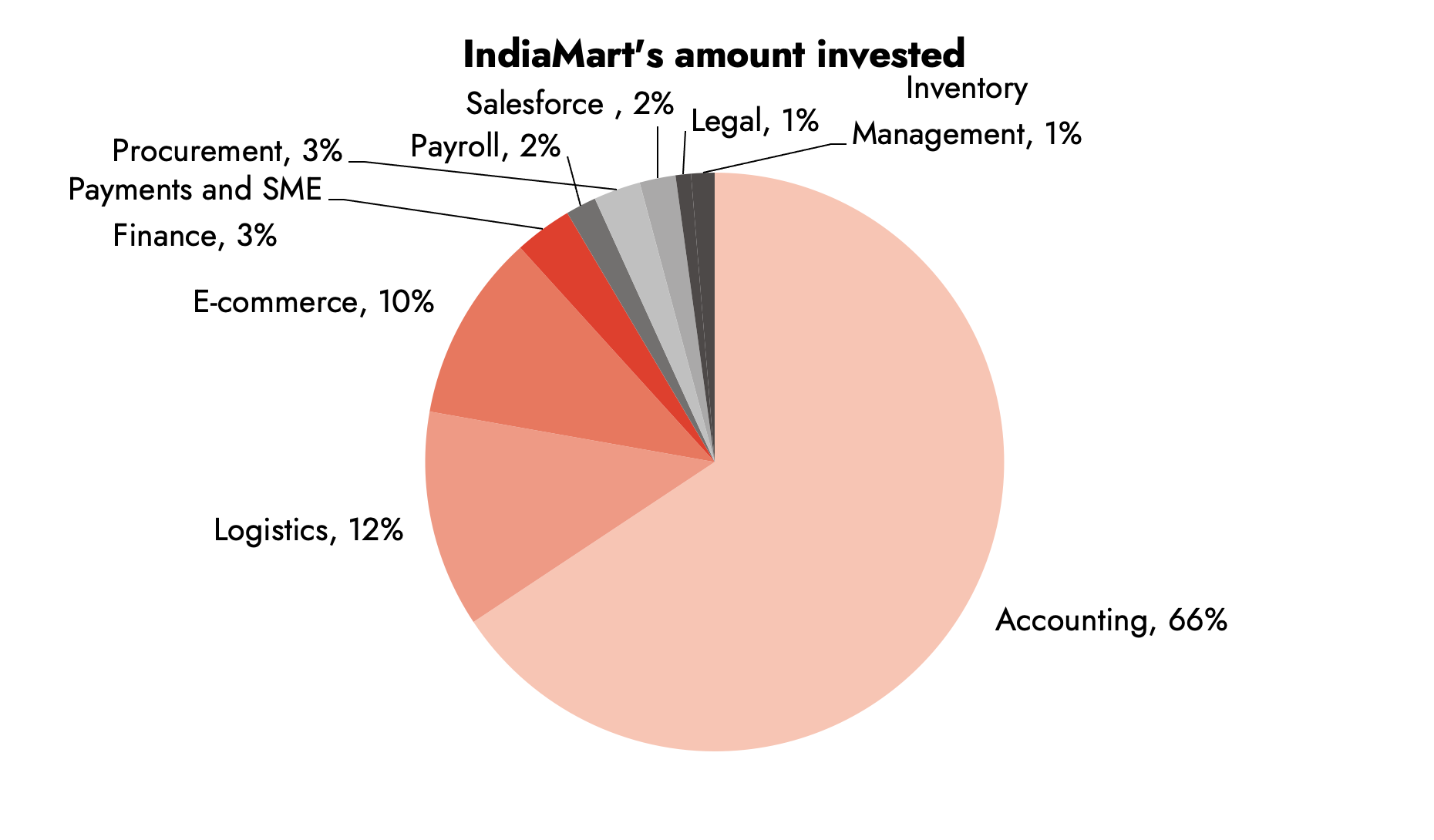

IndiaMart needs to mature from Buyer – Seller lead match to providing value added services in the coming future in order to stay relevant if they have. For the same, it has invested ~1,000 crores across verticals such as accounting, Logistics, MRO (Maintenance, Repair and Operations) E-commerce, Payroll, Procurement, Salesforce and Distribution, Inventory management and Legal Tech Platform(Exhibit 10). This is over and above the company’s existing order to cash management and payment services.

IndiaMart’s acquisition of Busy Infotech and Live-Keeping along with investments in Vyapar and Real Books gives IndiaMart a range of accounting solutions spread across on-site, mobile and cloud across small, medium and large enterprises.

Currently IndiaMart’s revenue from value added services including accounting is miniscule (~10%). The ability to scale up and cross sell these services along with IndiaMart will be critical to monitor.

Exhibit 13: IndiaMart’s investments have been across multiple verticals but primary focus is on accounting

Source: Ambit Asset Management, Company

3. Competitive intensity – The B2B ecosystem has seen a lot of capital being raised across various verticals which has resulted in rising competitive intensity for all B2B players.

Enterprises have entered business and business adjacencies solving problem areas in transaction financing, B2B procurement, supply chain, manufacturing and other areas.

Multiple B2B enterprises have reached the unicorn status across a host of B2B areas, which increases the competitive intensity in the space. In addition to the same , Just Dial (backed by Reliance) via JD Mart, Amazon business India and Tata Nexarc all have been trying to garner a piece of the B2B market.

In this heightened competitive scenario, we notice that except for Just Dial none of the above companies have attempted to enter the B2B classifieds space which can directly disrupt IndiaMart. Most of the companies have a transaction based model which is a different value proportion as compared to a subscription based model of IndiaMart.

Despite launching a while back JDMart has been unable to garner any material market share which further signifies the difficulty in creating a B2B market place similar to one which IndiaMart is. While direct competition is unlikely to disrupt IndiaMart, one needs to monitor how rest of the competition is faring providing a much better value proposition for MSME’s and how it can possibly disrupt IndiaMart in the future.

Exhibit 14: Multiple enterprises in the B2B space have turned unicorns in the recent past

|

Companies |

About |

Last round valuation (USD bn) |

|---|---|---|

|

OfBusiness |

Transaction Financing |

5.0 |

|

Udaan |

End to end B2B marketplace |

3.1 |

|

Moglix |

B2B - Procurement and supply chain for Industrial and MRO products |

2.6 |

|

Zetwerk |

Global manufacturing network |

2.5 |

|

Infra.Market |

Construction related procurement solutions |

2.5 |

Source: Ambit Asset Management, Company

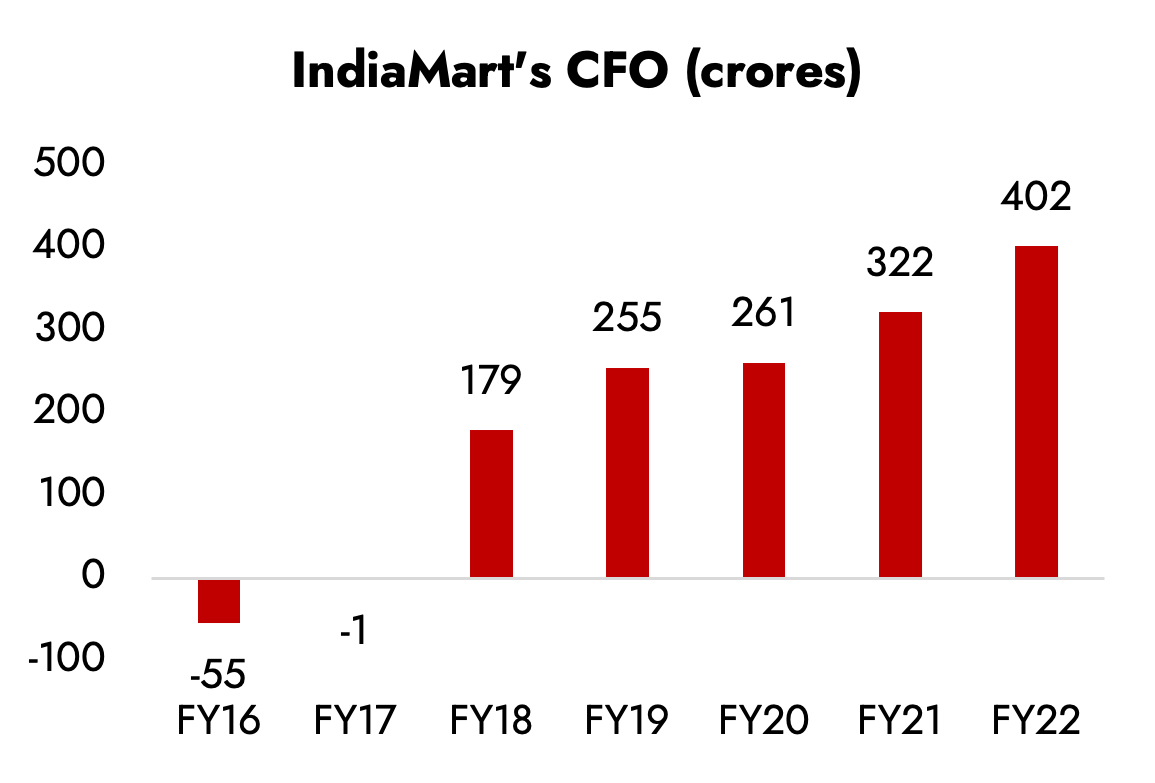

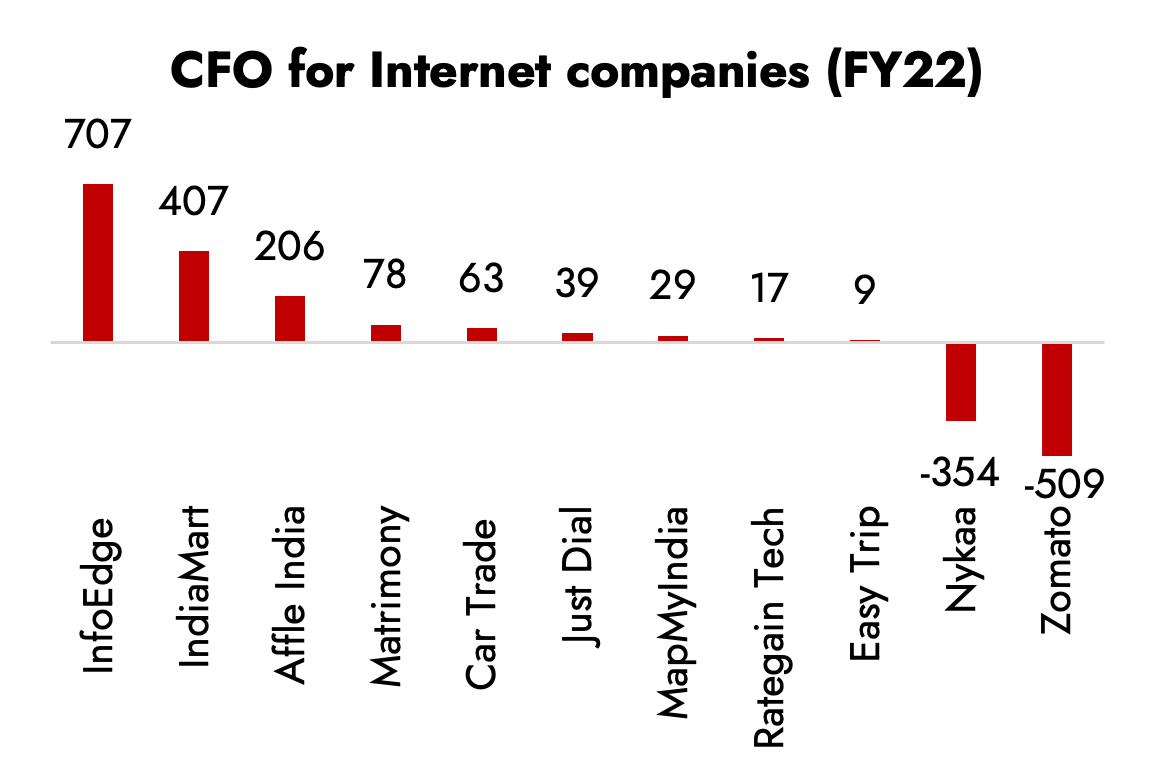

4. Capital misallocation – IndiaMart generates one of the highest operating cash flows (Exhibit 16) among the listed internet based companies. The capital outlay requirements for an internet business are minimal especially once a successful platform is created resulting in robust free-cash flows.

The company has deployed ~1000 crores in investments in adjacencies to provide a wider host of services and address the pain points of MSMEs, however, most of these investments are still financial in nature. How IndiaMart manage to scale and integrate them will be crucial for IndiaMart’s transition.

In addition to the same, IndiaMart has ~1900 crores of cash on its books which can be re-deployed for growth and enhance offerings. Redeploying capital efficiently while maintaining growth, navigating potential competition and technological challenges will be critical for IndiaMart.

Exhibit 15: IndiaMart’s OCF growth has been strong and consistently growing

Source: Ambit Asset Management, Company

Exhibit 16: Its OCF in absolute terms is amongst the highest for Indian Internet companies

Source: Ambit Asset Management, Company

5. Cyber and data security – A key threat for any internet company is cybercrime and data leakage. Cybercrime costs can include damage and destruction of data, stolen money, lost productivity, theft of intellectual property, theft of personal and financial data, embezzlement, fraud, post-attack disruption to the normal course of business, forensic investigation, restoration and deletion of hacked data and systems and reputational harm.

Some of the largest companies globally such as Yahoo (2013 and 2014), Alibaba (2019) and LinkedIn (2021) have been impacted by data breach. In India recently, PolicyBazaar (2022) and Zomato have faced similar data breach.

IndiaMart has invested heavily to secure proprietary system and it has a comprehensive policy for Data Privacy and Information Security Management Systems in accordance with ISO 27001:2013. In addition to that, on the cybersecurity side, the company has implemented various solutions for firewalls, API gateway, prevention or denial of service attack, DDoS or Distributed Denial of Service attack through sophisticated load balancers, data scraping, denial and fixing any personally identifiable mode and detection of re-entry of fraudulent buyers or fraudulent supplier.

Historically, there has been no material Data and cyber security risk associated with IndiaMart, however, any probable cyber and data security leaks can be a disruption.

Conclusion

Disruption risks for businesses especially in technology are very high. In a world where technologies are changing continually, adapting and evolving is paramount for an internet based business to succeed. The heavy level of disruption also bring out extensive competitive advantages for companies who have managed to adapt and evolved with the changing times.

IndiaMart has done extremely well in building a reliable platform with a range of products and suppliers. Pain points of transparent pricing along with supplier diversification of MSME’s are being addressed by IndiaMart. IndiaMart’s transformation journey which is to become an integrated solutions provider for MSME’s addressing further multiple pain points (accounting, logistics etc.) will be rife with challenges.

However, given the inherent strengths of the business, impressive track record of the company and how it has been able to adapt to multiple changes in technology IndiaMart is placed extremely favourably to expand, evolve and cater to multiple solutions to MSME’s.