We at Ambit are constantly trying to stay ahead of the curve by drowning out the noise and looking ahead. In keeping with our long term investment thesis, we like to stay up to date with not just the present impediments faced by your portfolio companies but also long term disruptions which can hit these companies. Hence we will regularly come out with our thoughts on disruptions in your portfolio companies/ sectors and for the 21st volume of this series we have selected Eicher Motors.

A disruptive technology/ innovation is one that helps create a new market and value network, and eventually goes on to disrupt an existing market and value network (over a few years or decades), displacing conventional wisdom or technology. This note takes a closer look at the structural changes taking place in the segments Eicher Motors caters to, and the possible disruptions that may lie ahead for the company over the longer term.

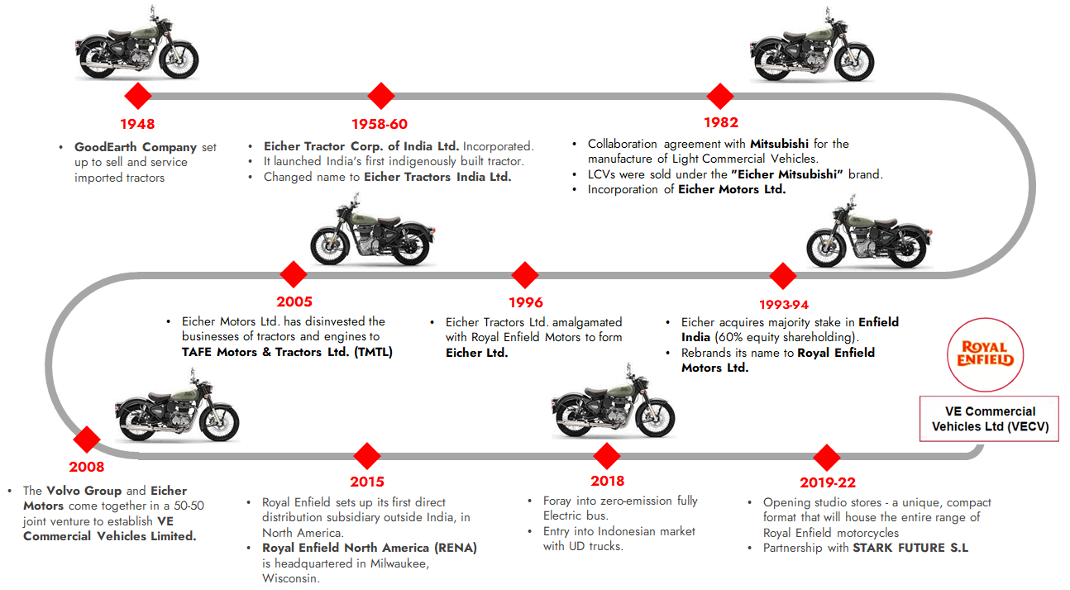

Eicher Motors – The Origins

The company's origin dates back to 1948, when the Goodearth Company was established to distribute and service imported tractors in India. The company, through the years, collaborated with Eicher Tractor Co, a German tractor manufacturer, and Mitsubishi to indigenously build and sell tractors and light commercial vehicles (LCVs) within the country. In the 1980’s, Eicher Motors Ltd was incorporated and LCVs were sold under the "Eicher Mitsubishi" brand. However, Eicher was not able to materially scale up in any of the segments it operated in (Refer Exhibit 1: the journey through the years).

Exhibit 1: Milestones of Eicher Motors

Source: Company, Ambit Asset Management

‘Biking’ into a new category:

It was in 1990’s; Eicher Goodearth co. acquired Enfield India Ltd and renamed it to Royal Enfield India (RE). Despite having a rich heritage, the company was not profitable. Eicher’s management had considered closing down and liquidating the motorbike division a few years after acquiring it.

Management change led to turn around of fortune:

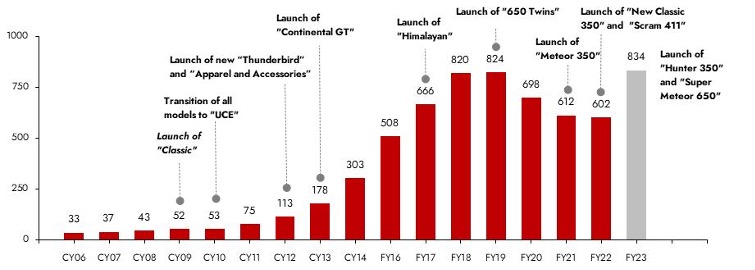

The entry of Siddhartha Lal, the third-generation heir, to Eicher had a huge impact on the future business of the company. Drawing inspiration from the Mini Cooper and Porsche – cos. focused and conscious of not diluting their core DNA – he set out to make the RE bikes fun to drive without diluting its DNA. The launch of the RE Classic, in 2009, turned out to be the inflection point for the company. The sales for the company shot up six times from 50,000 units in CY10 to a little above 300,000 units in CY14.

Product and Geographical expansions:

RE bikes have seen real evolution through the decades and after more than 65 years being built in India, the company is constantly enhancing its products (Refer Exhibit 2: for the current product lineup). The company is reportedly planning to launch its first electric motorcycle by 2025 on its L-platform, codenamed L1C. It believes that riders wanting accessible, affordable, yet characterful bikes are under-represented not just in India but globally.

Exhibit 2: Royal Enfield wants to be the global leader in middle-weight motorcycle segment (250-750cc)

Source: Company, Ambit Asset Management

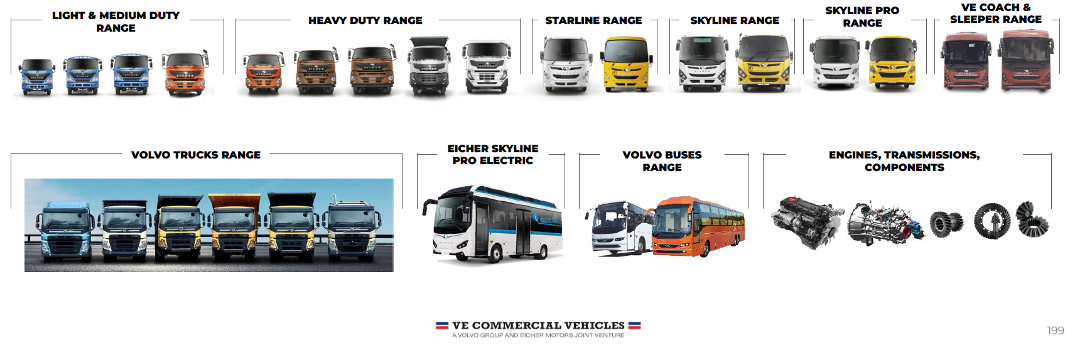

VE Commercial Vehicles:

Siddhartha realized that the growing demand for technologically advanced trucks and buses, Eicher would need more - funds, systems and technology. So in 2008, Eicher Motors tied up with Volvo, with a common vision of driving modernization in the commercial transport business in India. Volvo, through the JV would: (1) gain a significant market share in the country, (2) make India a base for exports to other emerging markets, and (3) produce trucks at a lower price through frugal engineering by injecting technology.

In 2020, Eicher motors through its subsidiary VECV acquired Volvo Group India’s bus business. This integration will help the company maximise the synergies and complement exports. Currently, VECV offers a range of trucks across 4.9-55 tonnes, along with a wide range over 150 fully built and bus chassis variants across light, medium and heavy-duty applications (Refer Exhibit 3: for the current product lineup).

Exhibit 3: Eicher and Volvo leveraged their respective strengths to achieve their separate goals

Source: Company, Ambit Asset Management

Royal Enfield Technology Centre

The new Royal Enfield UK Technology Centre in Bruntingthorpe (Refer Exhibit 4) is the innovation hub and global headquarters for Royal Enfield’s product strategy, product development, industrial design, research, programme management and analysis. They are focused on new products to spearhead Royal Enfield’s push for international growth.

“RE wishes to build bikes that reflect the brands history, that capture the character and feel of the RE bikes and also met modern expectations and requirements. Wish to bring global standard motorcycles that are relevant all over the world without any differentiation in any markets”. - Mark Wells, Head Product Strategy and Industrial design.

Exhibit 4: The 650 twins were developed in Bruntingthorpe with help from the Chennai Tech centre

Source: Company, Ambit Asset Management

The process when it comes to creating a bike!

- Ideation – All the ideas, looking more than five years into the future, come from anywhere within the business – customers, the sales team, designers, marketing, press etc.

- Proposals – These proposals are discussed with the senior management team before going full steam ahead.

- Blueprint – From there, they start with initial sketches and ideas. The Industrial Design team makes the 2D and 3D sketches and renders, then the Engineering Design team splits across chassis, engine and electrical. Within those teams they’ll have several designers submitting ideas, but once a project is agreed, they all work in the same direction.

- Process – The Company uses a ‘gate’ process for each stage of production, which helps in keeping checks on achievement v/s what was set out, before the final quality-control gate, and then production. They also test-ride the designs right through the whole process. The investment goes up as it passes through each stage gate.

- Time frame – If it’s a brand-new bike with a new engine it can take four years while others take significantly less time.

Story in charts – Company Overview

Exhibit 5: Expansion of the middle class segment will increase the customer base for RE

Source: Company, Ambit Asset Management

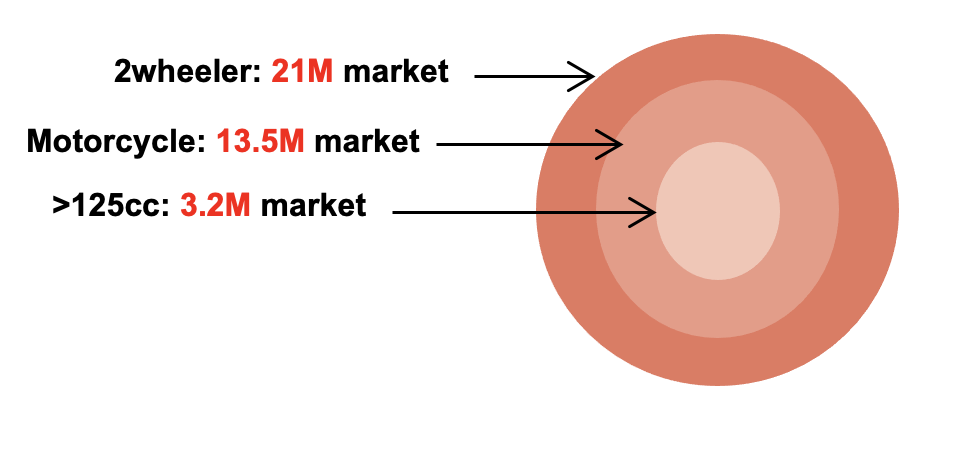

Exhibit 6: Rising income and favorable demographic present a ~3 million domestic (addressable) market

Source: Company, Ambit Asset Management

Exhibit 7: Volumes (in ‘000) grew by ~15X from CY-2010 to FY-2023, prior to significant external headwinds

Source: Company, Ambit Capital Research

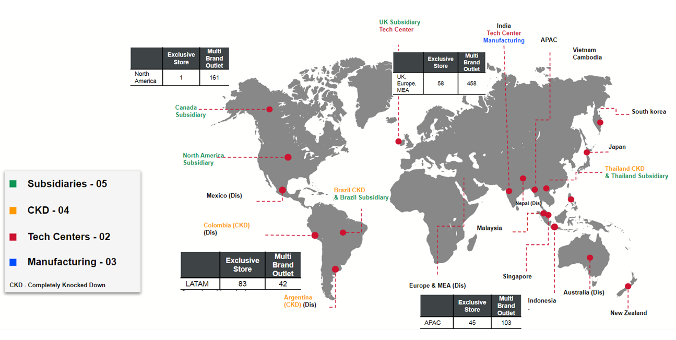

Exhibit 8: 950+ global touch points presents a ~1 million export opportunity for RE

Source: Company, Ambit Capital Research

Exhibit 9: Manufacturing enhanced with Volvo buses and Industry 4.0 Bhopal plant

Source: Company, Ambit Capital Research

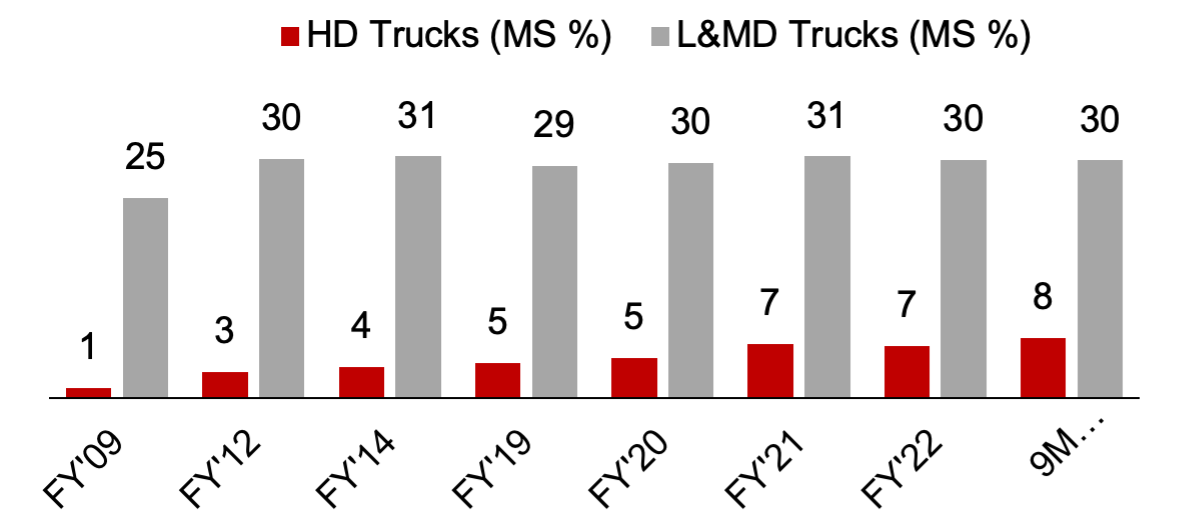

Exhibit 10: Eicher is an established OEM with 300+ variants in the LMD portfolio

Source: Company, Ambit Asset Management *HD – Heavy Duty, LMD – Light & Medium Duty

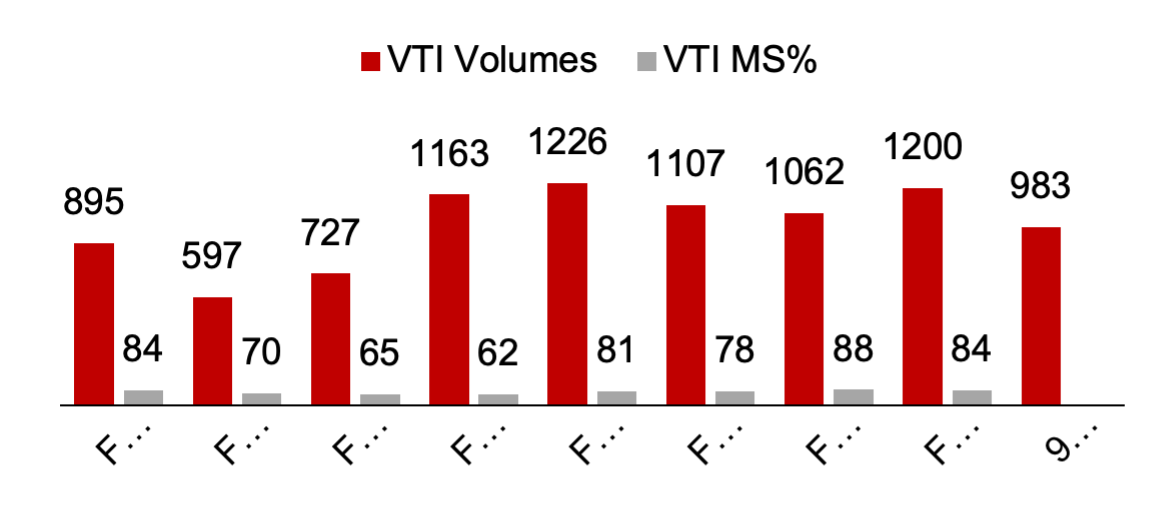

Exhibit 11: VTI is a leader in the high end premium segment

Source: Company, Ambit Asset Management *VTI – Volvo trucks India

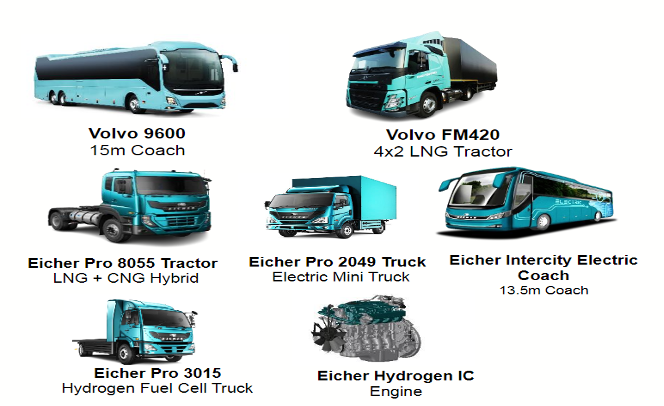

Exhibit 12: VECV showcased future readiness through sustainable technology, products @ Auto Expo’23

Source: Company, Ambit Capital Research

Scanning for Disruptions:

1. Changing Consumer behavior:

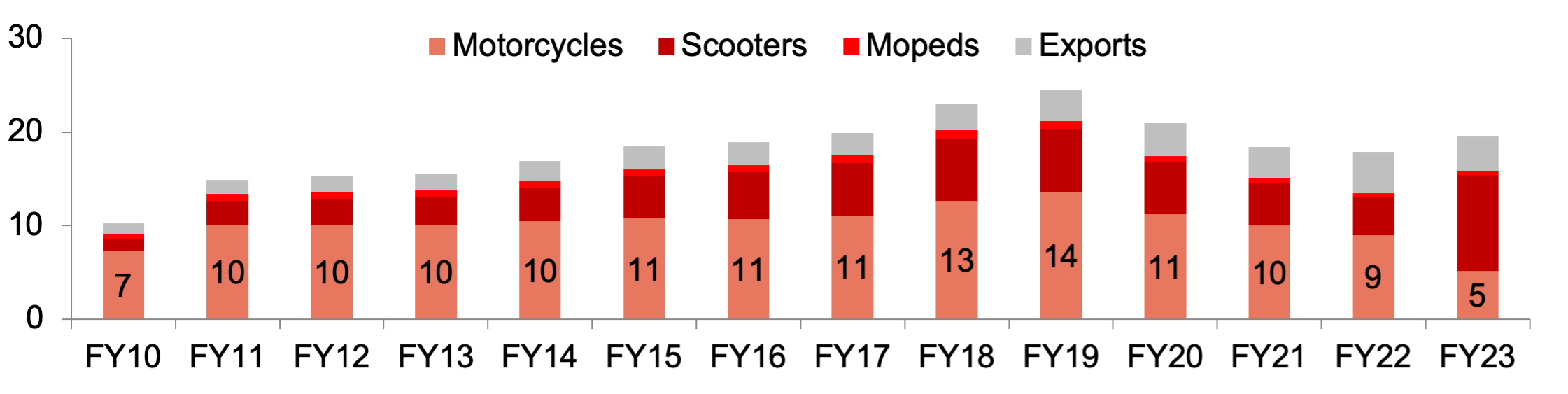

Declining Ridership – Since the high of FY19, 2-wheeler OEM’s have been struggling with sliding sales. Motorcycles have been the worst hit with volumes pushed back to FY10 levels (Refer Exhibit 13) while scooters have been relatively better with volumes hitting an 8-year low. There have been many reasons postulated for the shrinking ridership numbers and flagging sales:

- The wage growth in rural India has been slowing down and hasn’t kept pace with inflation; Semi-urban/rural markets (~40% of sales).

- New regulatory norms, high insurance costs, fuel price hike have pushed up cost of ownership;

- Consistent price increases (~40% jump in costs in 3 years). It decreases the value proposition;

- Availability of cheaper mass transit systems

- Urbanization leading to higher vehicular traffic. People opting public over private mobility.

Exhibit 13: India’s motorcycles sales for FY23 at 5.1 mn units have fallen to their lowest in a decade, declining below the 7 mn mark that was reached for FY10

Source: SIAM; Ambit Asset Management

Even in the export markets, red flags were visible in many pockets of the motorcycle industry. Harley-Davidson’s woes in terms of sliding sales are well known (Refer Exhibit 14), but other bike makers were struggling as well – barring a few, such as Triumph and Polaris-run Indian, saw growth. Key reasons attributed for the decline were:

- Boomer buyers, the most consistent motorcycle consumers, are aging out of the industry fast. Additionally, the motorcycleindustry spent most of its time marketing to the boomer generation and deprived itself of new sales from the younger customers.

- The industry has failed to attract new riders out of women, and millennial. Younger buyers usually don’t consider spending their savings on recreational vehicles and appear to be motivated to consider motorcycles only for practical reasons.

- The arrival of autonomous vehicles may push motorcycles off the road entirely due to advances in technology making cars safer and more efficient.

- Increasing popularity of ride-sharing services have led to a decrease in the number of people who own motorcycles, as these services make it more convenient and affordable to get around without a vehicle.

Exhibit 14: Worldwide, Harley-Davidson reported 2022 bike sales (in ‘000) that were down by 8%, year on year

Source: Company; Ambit Asset Management

Riders are downsizing to smaller motorcycles – Globally, a trend observed pre-COVID and continues to remain relevant today, especially in the developed markets, is the rise of small-displacement but full-sized motorbikes that appeal to new riders, and experienced ones as well. The best example is the Street 750 and Street 500 by Harley Davidson. BMW Motorrad is concentrating on the smaller capacity bikes with the G 310R through their collaboration with TVS. Motorcycles in the 200-400cc along with a new emerging class of retro-styled 125cc city-machines are getting the attention of new riders, especially women riders. These bikes are finding buyers as OEM’s pour innovation and better quality components into these beginner bikes.

- With motorcycle-riding public ageing, the need for bulky bikes has decreased.

- Smaller bikes are cheaper to buy and own/maintain.

- The bigger the bike, the more effort it takes to ride it

With highway construction on the fast lane and urban wage increasing, it bodes well for Royal Enfield. The company has charted out a new path to focus on the vast Indian hinterland by setting up mini dealerships. Enfield has, thus, managed to be both aspirational and accessible.

2. Technological disruptions:

Relatively tougher transition to Electric – As the world moves off fossil fuels, it’s fair to say that the future of motorcycles is electric. However, the current technological capability for adoption of EV in high-performance bikes – vis-à-vis low displacement (cc) 2W – is at a very nascent stage, with several design and cost challenges – .

- Integrating the (bigger) electric motor and the battery while maintaining the stability of the vehicle is much more complicated.

- Compactness makes it difficult to have big heat management systems implying limited power.

- Bigger batteries and motors add to the weight as well as produce more heat, reducing the overall vehicle performance.

- Integrating electric powertrains into an already economical, lightweight and tightly-packaged machine brings dynamic, ergonomic and aesthetic headaches.

- Motorcycles need more power which means a bigger electric motors as well as battery which pushes up the cost.

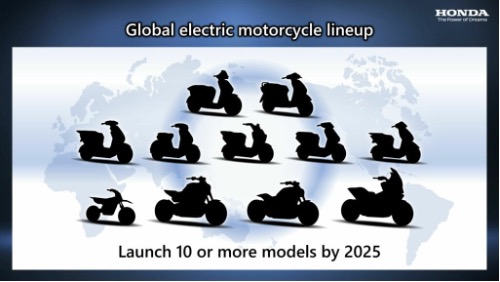

Therefore, scooters have cornered the lion's share of the nascent electric 2W market with >90% of share. As the industry evolves and with more R&D spends, companies will offer more electric motorcycles. Japanese motorcycle brands such as Honda, Suzuki, and Kawasaki etc. have laid out a definitive timescale for introducing electric bikes to their portfolio (Refer Exhibit 15, 16). Harley-Davidson spun off its electric future into an entirely separate company, BMW and Triumph have showcased intriguing concepts that are in pipeline, and Husqvarna is teasing a number of battery-powered vehicles. TVS motor, according to a recent patent document, is also looking at a hydrogen-powered scooter.

Exhibit 15: Honda plans on launching 10 models by 2025

Exhibit 16: Harley-Davidsons has projected 101,000 sales within 5 years for the LiveWire

Source: Company, Ambit Asset Management

Fuel cell electric vehicle (FCEV) – the next gen engine for CV – The CV industry has a higher carbon footprint than the PV industry, and to reach net zero carbon emissions, it would have to keep innovating. Key stakeholders across the value chain of CV’s are increasingly of the view that electrification of CV’s might be through the hydrogen fuel cell route and not the battery EV (BEV) route. They believe:

- CNG and BEV are appropriate for short trips and last-mile travel;

- FCEV and LNG are for cross-country trips;

- Internal combustion (ICE) with blended fuels could be used for areas where no charging stations or hydrogen available. Even H2ICE, in which hydrogen is used in ICE instead of fossil fuels, could be used.

Therefore, combustion might still be required in the CV segment, albeit in a modified form.

Exhibit 17: Despite current limitations, hydrogen is still an environment friendly alternative to fossil fuels

| Pros of Hydrogen Fuel Cells | Cons of Hydrogen Fuel Cells |

|---|---|

| Renewable and readily available: Hydrogen is the most abundant element in the Universe and renewable source of energy, perfect for future zero-carbon needs. | High investment is required: Hydrogen fuel cells needs heavy initial investment to be developed. This will require the political will to incentivize investment in order to improve and mature the technology. |

| More powerful and energy efficient than fossil fuels: Hydrogen fuel cell technology provides a high-density source of energy with good energy efficiency. Hydrogen has the highest energy content of any other common fuel by weight. | Hydrogen storage: Storage and transportation of hydrogen is more complex than that required for fossil fuels. This would lead to additional costs till scale efficiencies kick in. |

| Faster charging times: While EVs require between 30 minutes and several hours to charge, hydrogen fuel cells can be recharged in <5 mins. | Highly Flammable: Hydrogen is a highly flammable fuel source, which brings understandable safety concerns. Hydrogen gas burns in air at concentrations ranging from 4 to 75%. |

| Long Usage Times: A hydrogen vehicle has the same range as those that use fossil fuels. It is superior to that currently offered by EVs. Hydrogen fuel cells are also not significantly impacted by the outside temperature and do not deteriorate in cold weather. | Infrastructure: Large scale adoption of hydrogen fuel cell technology for automotive applications will require new refueling infrastructure to support it. |

Both H2ICE and FCEV are zero-carbon vehicles, provided the fuel used is green hydrogen (produced by renewable sources of energy).

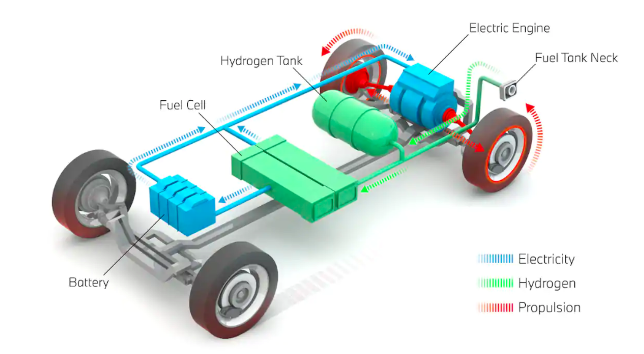

In an FCEV, electricity is produced using a fuel cell powered by hydrogen, rather than drawing electricity from only a battery. Hydrogen and oxygen are combined to produce water and electricity. The electricity is then used to drive the vehicle’s motor and water is the only waste produced. Because electricity is developed by the vehicle, FCEVs don’t need charging support, unlike BEVs (Refer Exhibit 18).

Exhibit 18: The 3 key components: Hydrogen tank, Battery, and Electric Motor work together to power the FCEV

Source: Company, BMW, Asset Management

In H2ICE, hydrogen is burnt inside either the compression ignition engine or the spark ignition engine — two variants of ICE — in the same way as current ICE fuels are burnt. The absence of carbon in hydrogen means that in the exhaust, there are zero carbon-based pollutants such as carbon monoxide, carbon dioxide and hydrocarbons.

At present, H2ICE and hydrogen fuel cell are in the development stage for Eicher motors. With technology evolving faster, there is a risk that any investment in technology could turn obsolete. Early introduction could benefit it with first mover advantage.

3. Key Man risk:

“I just saw it, and I fell in love with it. That motorcycle became my real companion.” - Siddhartha Lal

Siddhartha Lal’s love affair with RE started when he was just 17, when he adored the gleaming chrome red RE motorcycle parked in his garage after returning from his boarding school. At 26, he was entrusted with the responsibilities of reviving the dying company. To spot the gaps, he spent months on the roads, riding and chatting with people, tried to emotionally connect with the customers to understand their feeling, mindset, and the priorities and took some important (hard hitting) steps to bring RE back to its former glory.

- He divested 13 businesses from Eicher and devoted all of his resources and attention to RE motorcycles and trucks.

- Having a master’s in auto engineering helped him be heavily involved in the manufacturing process—right from the development to the testing phases—of RE's new products.

- Brought in much-needed experience in the likes of RL Ravichandran (had worked with TVS, Suzuki and Bajaj Auto) as the CEO of the group for its revival process along with Rudratej Singh from Unilever, realizing that good marketing is as important as engineering. In 2014, RE hired Rod Copes, a 20-year Harley-Davidson employee, as head of the North American Division, and Pierre Terblanche, a motorcycle design stalwart and former Ducati employee.

- Kept the appearance and feel of previous generations of motorcycles while incorporating modern technology, engine, and better gearbox.

- Spent 700-odd days setting up the process and systems to leverage the complementary strengths of the JV between Eicher Motors and the Volvo Group before handing it over to domain experts to take on a more active role.

Over the last 2 decades, Siddhartha has been building a team to manage the businesses as they grow. However, there have been some high profile exits over the recent years. These have the potential to slow down the strengthening of the 2nd line management. CXOs across functions including Vinod Dasari (CEO – RE), Lalit Malik (CCO), Jayapradeep Vasudevan (National sales head – RE) Shubranshu Singh (Global Head – Marketing), Vimal Sumbly (APAC head) and Manhar Kapoor (Chief Legal Officer), amongst others have left for other opportunities.

4. Future Split:

The VECV JV (majority-owned by EML and equally managed by both partners) has created a strong foundation by modernizing the product range, the manufacturing footprint and well defined processes through Volvo’s technology and Eicher’s competence in frugal engineering. Volvo was able to enter the mass market business in India; it needed a strong local partner, while Eicher was in need of superior technologies and know-hows to spruce up its business. The partnership has helped VECV to be the third largest CV maker in the country. That said, there are risks associated with it (Refer Exhibit 19).

Over the last two decades, with globalization seeping into the Indian system and regulatory framework turning favorable to foreign investments, foreign companies feel a lesser need to have partners and share profit and control esp. when they wish to expand faster than their Indian partners. In the event of a split in the JV, Eicher will find it difficult to access technology, utilize its financial resources, and build a larger presence in the global commercial vehicle business. Also, in case Eicher exits from the JV, it would be interesting to see how the cash will be utilized.

Exhibit 19: In the automotive market, 4 such JVs that didn’t see the daylight for long

| JV - Objective | Why was it called off? |

|---|---|

| Ford Motor Co - Mahindra & Mahindra JV: to develop, market and distribute Ford vehicles in India along with Ford and Mahindra vehicles in high-growth emerging markets overseas. | Driven by fundamental changes in global economic and business conditions due to COVID. The events made both reassess their respective capital allocation priorities. |

| Hero Group – Honda Motor Co JV: Hero with its in-depth knowledge of the Indian market produced and sold motorcycles in India with Honda’s fuel efficient and technologically superior bikes. | Disagreement over exports as JV agreement restricted Hero Honda’s exports to just four markets—Sri Lanka, Nepal, Bangladesh and Colombia. |

| TVS Group – Suzuki Motor Corporation JV: focus was on technology transfer for design and manufacture of two-wheelers specifically for the Indian market. | Differences over the issues of management control and ownership. Also, there were disagreements on funds and technology for new models. |

| Mahindra & Mahindra - Renault JV: to produce and sell the latter's car, Logan, in India. Separately, discussions were on between the two parties to sell M&M SUVs abroad through the French auto major's distribution channel. | Dissolved JV post limited sales offtake owing to high prices and uninspiring design. |

5. Futuristic disruptions:

Motorcycle of the future – Since the very first motorcycle, ~150 years ago, two-wheelers have gone through great innovation, improving every decade. Inspired by the “Star Wars” movie series, a Japanese start-up AERWINS Technologies debuted a flying hover bike (Refer Exhibit 20) at the Detroit Auto Show, 2022. The bike is designed to fly at some 3m above the ground using six propellers and flies at speeds of up to around 80 to 100 kmph.

Efforts are in progress in Japan to put into practical use these “flying bikes”. They are expected to be used in rescue operations and supplies transportation in disaster-hit areas. In fact, they could be used as a substitute for rescue helicopters, whose prices and maintenance costs are high. According to ALI Technologies, it has been receiving many inquiries about its hover bike from the entertainment sector, as well as from police and firefighting authorities abroad, mainly in the Middle East and North America, both of which have many deserts.

While the whole concept of Flying hover bike may seem slightly far-fetched over the medium term, innovations similar to these, do pose a great disruption to Motorcycles.

Exhibit 20: World’s first flying bike (The XTURISMO hover bike) makes its debut at Detroit Auto Show

Source: Company, News articles

6. Capital Allocation:

When it comes to successful business execution, it is paramount to play to one’s strength while at the same time not foregoing market opportunities. We are reminded of Bajaj Auto in this instance. The company transitioned from scooters to Motorcycles under the MD Rajiv Bajaj with no intention of getting back to the Indian scooter segment. The aim was to go for a bigger share in the global motorcycle market. However, considering the changing market dynamics, Bajaj Auto re-entered the scooter segment with its electric scooter designed along the lines of the original Chetak.

Eicher Motors is a leading Motorcycle player and plans to crack it on a global scale. The company currently does not have any plans of diversifying into other segments like scooters or 4-wheelers. But should the company decide to change course and tap the market, it would entail significant capital investment and management bandwidth. Without the requisite experience of running these segments – which Bajaj Auto had in earlier example – Eicher would be risking a lot at stake.

7. Competitive Intensity:

Increasing competition in the premium segment – As the GDP per capita income of India gets better, the demand for superbikes have increased in India. These segments are less sensitive towards price and the customers wish to make a statement, follow their passion.

The shift in consumer choice to bigger engine capacity 2W’s has prompted two Japanese heavyweights, Suzuki Motorcycle and Yamaha, to exit the budget category segment entirely and focus on the premium segment. India has developed good R&D capability and a lot of motorcycles are getting designed in India. With low cost and a highly capable talent pool, it makes a lot of sense to manufacture low-volume, mid-size motorcycle here. BMW, KTM, Triumph, etc. have tied up with Indian manufacturers for just that. Harley-Davidson has made a comeback in India through Hero MotoCorp's retail outlets (Refer Exhibit 21).

Exhibit 21: Harley Davison X350; Triumph-Bajaj Scrambler are some of the bikes in competition with RE

Source: Company, News articles, rushlane.com; * to be launched

Bicycle to Bikes transition – In order to attract new riders, motorcycle makers have started selling electric bicycles. Electrified bicycles are low-powered motorcycles that allow for motion without pedaling (most are regulated to 20 miles an hour, some can go far faster).

They believe that it would be a natural progression for bicycle riders to migrate to motorcycle in the future. It would act as a bridge product as time spent on an electric bicycle will lead to some riders to wonder: What would it be like to level up to a motorcycle? With companies adopting a DTC approach to marketing and delivery of electric bicycles, the segment, along with regular bicycle sales, has seen double digit growth during the pandemic.

Indian/Polaris has just introduced an electric FTR model for kids and Harley-Davidson actually sells electric balance bikes for kids on their website (Refer Exhibit 22, 23). Other motorcycle makers, such as Ducati and Yamaha, are clearly pushing forward with electric bicycle offerings. E-bikes and electric motorcycles are becoming a regular part at the International Motorcycle Shows, where attendees get to ride them on short test tracks as part of the Discover the Ride programs.

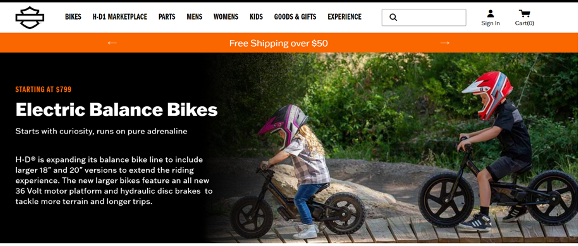

Exhibit 22: Harley-Davidson is looking at ways to expand into electric balance bikes for kids

Source: Company, Ambit Asset Management

Exhibit 23: The eFTR Jr is a mini-replica of the Indian FTR 750 targeting children/teenagers

Source: Company, Ambit Asset Management

Conclusion

Eicher Motors stands out as one of the few Indian auto companies that stand out in the minds of the customers domestically and abroad because of the legacy and heritage of RE. Growth in volumes because of new product launches, a rise in export volume by diversifying its presence across the international regions and market share gains will help it in future growth. While there are several short term disruptions which may impact the company, the company has all the ingredients to address the huge addressable market size.