The Messi(ah) of global economy - India

As the dust settles on an enthralling month of soccer, fans were treated to, arguably, one of the greatest ever World Cup finals in the sport’s history. The final had superstar rivalries, classy goals, nail biting penalties, and goalkeeping master-classes, and in the end a pièce de resistance, the iconic image of Lionel Messi – lifted aloft on his teammates’ shoulders – with the World Cup trophy finally in his hands.

The opening 79 minutes were all about La Albiceleste, who led by 2 goals. France (primarily, Mbappé) turned around the game within 97 seconds, taking the game to extra-time. Mbappé – yet again – denied Messi the World Cup winning goal scoring in the final minutes to equalize AGAIN!

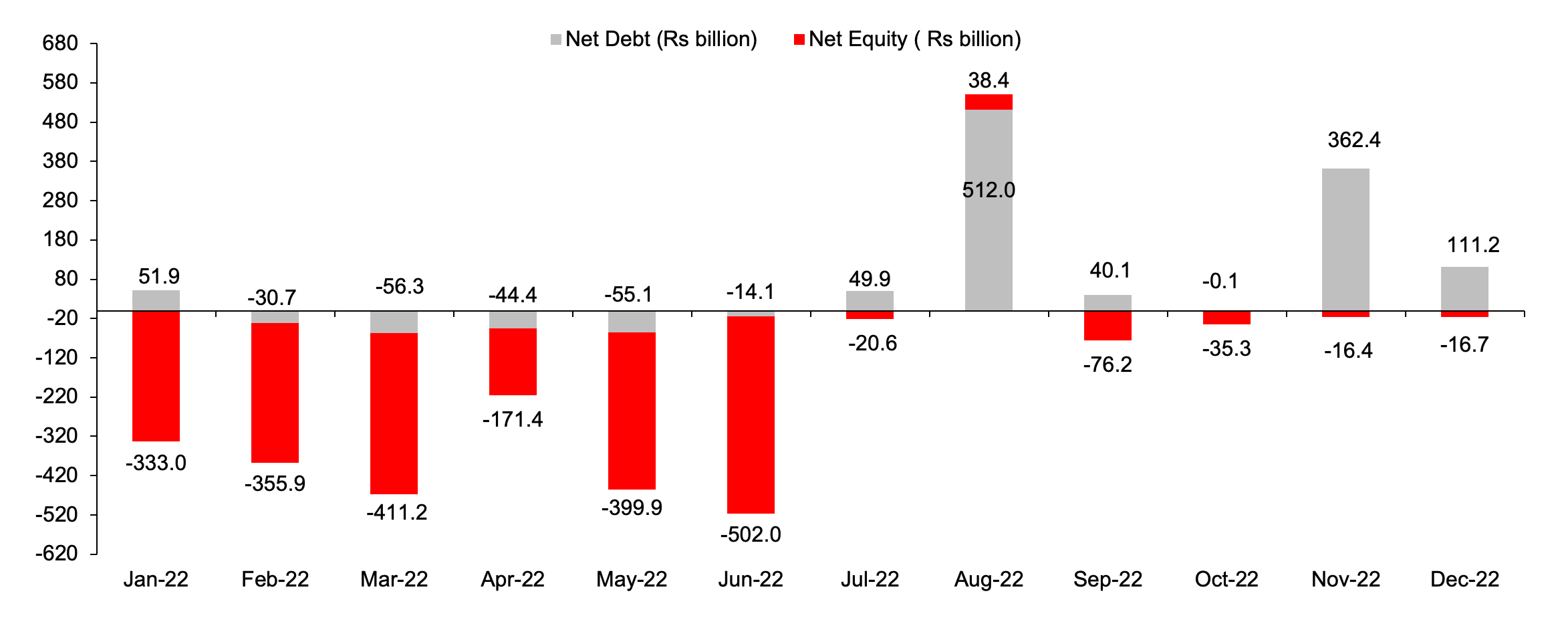

Drawing parallel to the see-saw battle, the Indian equity game (markets!) also saw shifts happening throughout the year (witnessed high volatility!). Capital flows from foreign portfolio investors (FPIs) in 2022 reflect two distinct trends – while the first half of the year witnessed an aggressive sell-off, the second half was about their return to the Indian markets (Refer Exhibit: 1).

Exhibit 1: Net FII flow in CY22 – one of the sharpest outflows which couldn’t deter the markets

Source: FPI flows in 2022, NSDL

The sluggishness in the markets was due to multiple factors: the Russia-Ukraine crisis, which resulted in the highest ever inflation in 40 years in the USA, followed by the steepest rise in interest rates by the US Fed which led to a flight of capital from riskier assets, commodity pressures, and slowing consumption.

Despite several headwinds on both global and domestic levels, the Indian equity markets showed resilience and turned out to be one of the top performers across the globe against peers. Relatively strong growth and a healthy corporate earnings cycle acted as positives, making the fundamentals of the Indian economy much more attractive than most EMs. A worrisome current account deficit, tighter liquidity (compared to a year ago) and high inflation are challenges we expect to last for a few more quarters at least.

In this note, we will take you through some of the notable points to summarise the year gone by (including Hits and Misses) and talk about the outlook for CY2023.

Sectorial overview of 2022 and the road ahead for 2023

We take a deep dive into a few key sectors and assess the year gone by and outline the key themes to look out for in CY23

Exhibit 2: We remain bullish on Banks, Auto, IT Services, discretionary consumption in CY23

|

|

CY22 |

CY23 |

|

|

Sector |

Hits |

Misses |

Outlook |

|

Automobiles & Auto-Ancillary |

|

|

|

|

Building Materials |

|

|

|

|

Chemicals |

|

|

|

|

Consumer Discretionary |

|

|

|

|

Consumer Staples |

|

|

|

|

Financials |

|

|

|

|

IT |

|

|

|

|

Pharmaceuticals |

|

|

|

Outlook for 2023 – Will Indian markets outperform in 2023?

2022 witnessed a roller coaster ride and with a meagre ~6% returns in INR terms. The recent resurgence of covid-19 in China is the kind of exogenous disruptions that the global equity markets could likely endure. However, as we usher in 2023, we do expect the Indian equity markets to bounce back and deliver handsome returns. Some of the key reasons that make us optimistic and need to be watched out for are as below:

- End of the tightening cycle: The latest inflation data (for both USA and India) have been quite encouraging and makes us believe that globally inflation has peaked out. In India, with CPI inflation falling to 5.9%, the real policy rates are now in the positive. Thus, RBI rate hike cycle looks to be ending.

- Earnings growth trajectory to pick up: CY23 is expected to witness strong earnings growth acceleration largely on account of margin expansion, softening commodity prices (including oil & gas) and meaningful pricing action (across sectors).

- Rural growth resurgence: Over the last couple of years, a combination of rising WPI inflation and crop damage due to unseasonal rains meant that rural demand remained weak. However, factors such as encouraging early sowing data from Rabi crop, softening WPI inflation and rising rural consumer sentiment are indicative of a turn-around.

- Accelerated government spending: In the run up to the 2024 elections, government spending is expected to accelerate especially now that the fiscal situation is quite better than expected. The upcoming budget could emphasis on rural growth, infrastructure, affordable housing and agriculture. This would ensure that the credit growth remains strong in double digit (even on a high base) in 2023.

So, overall we believe that macro-economy wise the worst is behind us and the situation looks to have stabilized. Softening export demand, depreciating INR, current account deficit problems, are now all behind us. All of this should augur well for Indian Equities heading into 2023.

CONCLUSION

“Argentina's loss to Saudi Arabia in their first World Cup game was a turning point in the changing room”, coach Lionel Scaloni had said, bringing out the grit to recover, winning six consecutive matches on the trot. Argentina's path to glory is a parable for investors, there are quite a few lessons that one can draw from sports despite a tough start.

Time & Patience – more powerful than intelligence and talent

The seeds of Argentina's fortune were sown 4 years back when Lionel Scaloni, Argentina’s coach, was appointed to engineer a turnaround after Argentina’s 2018 World Cup nightmare. Despite losing the first game, his perseverance and calmness of not overreacting and playing to their strengths paid off. The same ought to be mimicked in one’s investing journey. This was aptly explained by Warren Buffet: "Investing is not a game where the guy with the 160 IQ beats the guy with the 130 IQ. Once you have ordinary intelligence, what you need is the temperament to control the urges that get other people into trouble in investing."

Even the best underperform in the short term

Argentina’s loss to Saudi Arabia, France and the well fancied, Denmark, loss to the lowly ranked Tunisia, the end of Belgium’s golden generation, or Vincent Aboubakar's historic goal against Brazil, the tournament saw a lot of major upsets. Even the best underperformed. Similarly, the best of the company or economy will go through near-term blips. What is important is the long-term performance.

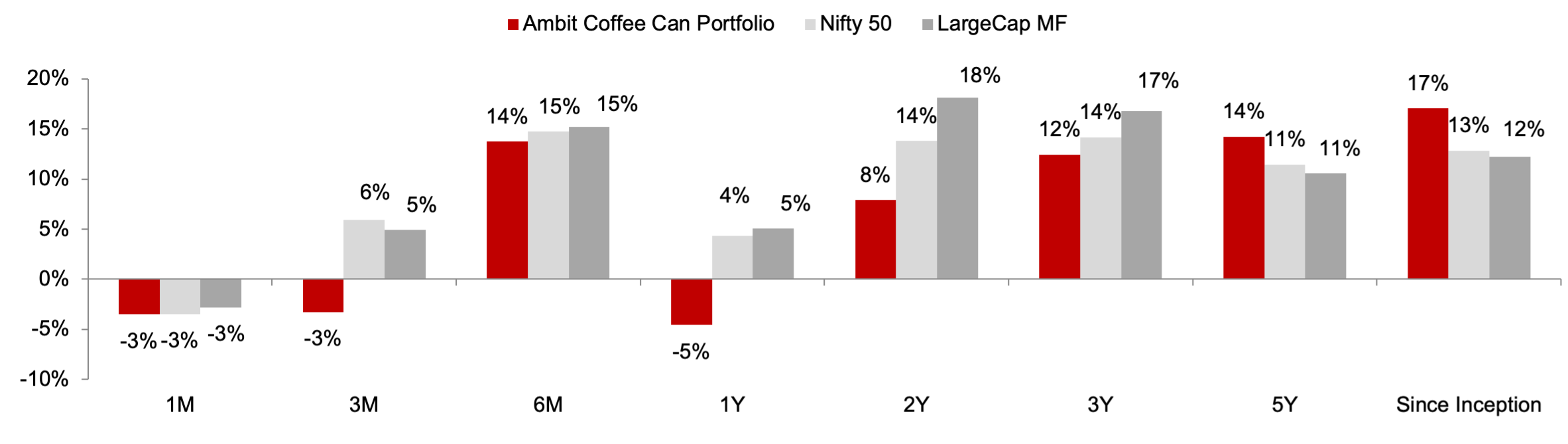

Ambit Coffee Can Portfolio

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced by disruptions at regular intervals. As the industry evolves or is faced by disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

Exhibit 3: Ambit’s Coffee Can Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of 31st Dec, 2022; All returns are post fees and expenses; Returns above 1-year are annualized; Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts.

Exhibit 4: Ambit’s Coffee Can Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of 31st Dec, 2022; All returns are post fees and expenses. Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts.

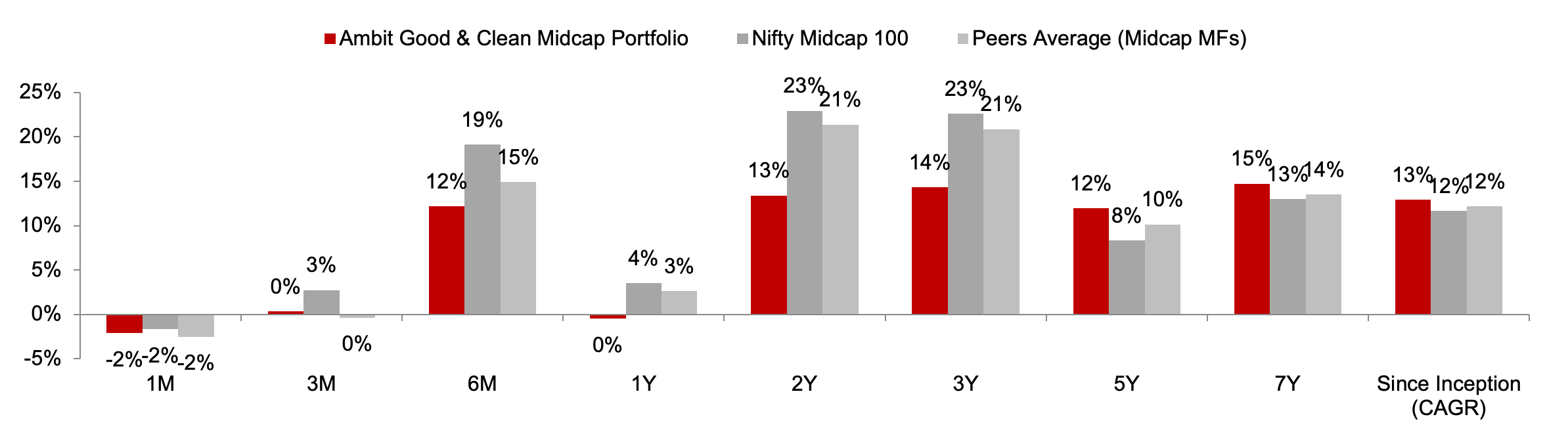

Ambit Good & Clean Midcap Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver superior risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

- Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

- Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longer with annual churn not exceeding 15-20% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with this compounding earnings acting as the primary driver of investment returns over long periods.

- Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

Exhibit 5: Ambit’s Good & Clean Midcap Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of 31st Dec, 2022; All returns above 1 year are annualized. Returns are net of all fees and expenses

Exhibit 6: Ambit’s Good & Clean Midcap Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of 31st Dec, 2022. Returns are net of all fees and expenses

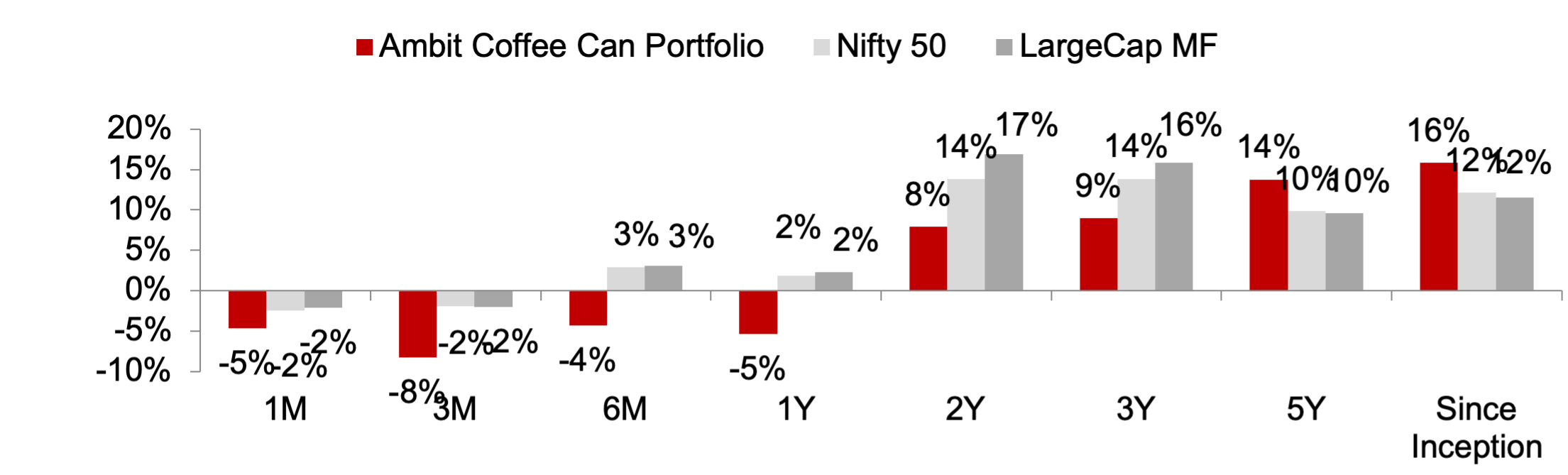

Ambit Emerging Giants Portfolio

Small caps with secular growth, superior return ratios and no leverage –Ambit's Emerging Giants portfolio aims to invest in small-cap companies with market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than Rs4,000cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt) and ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence lead us to a concentrated portfolio of 15-16 emerging giants.

Exhibit 7: Ambit Emerging Giants Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of 31stDec, 2022; All returns above 1 year are annualized. Returns are net of all fees and expenses

Exhibit 8: Ambit Emerging Giants Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of 31stDec, 2022. Returns are net of all fees and expenses

Ambit TenX Portfolio

Ambit TenX Portfolio gives investors an opportunity to participate in the India growth story as the Indian GDP heads towards a US$10tn mark over the next 12-15 years. Mid and Small corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that can grow their earnings 10x over the same period implying 18-21% CAGR. Key features of this portfolio would be as follow:

- Longer-term approach with a concentrated portfolio: Ideal investment duration of >5 years with 15-20 stocks.

- Key driving factors: Low penetration, strong leadership, light balance sheet

- Forward-looking approach: Relying less on historical performance and more on future potential while not deviating away from the Good & Clean philosophy.

- No Key-man risk: Process is the Fund Manager

Exhibit 9: Ambit TenX Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of 31stDec, 2022; Returns are net of all fees and expenses

Exhibit 10: Ambit TenX Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of 31stDec, 2022. Returns are net of all fees and expenses

For any queries, please contact:

Umang Shah- Phone: +91 22 6623 3281, Email - [email protected]

Ambit Investment Advisors Private Limited -

Ambit House, 449, Senapati Bapat Marg,

Lower Parel, Mumbai - 400 013

Risk Disclosure & Disclaimer

The performance of the Portfolio Manager has not been approved or recommended by SEBI nor SEBI certifies the accuracy or adequacy of the performance related information contained therein.

Ambit Investment Advisors Private Limited (“Ambit”), is a registered Portfolio Manager with Securities and Exchange Board of India vide registration number INP000005059.

This presentation / newsletter / report is strictly for information and illustrative purposes only and should not be considered to be an offer, or solicitation of an offer, to buy or sell any securities or to enter into any Portfolio Management agreements. This presentation / newsletter / report is prepared by Ambit strictly for the specified audience and is not intended for distribution to public and is not to be disseminated or circulated to any other party outside of the intended purpose. This presentation / newsletter / report may contain confidential or proprietary information and no part of this presentation / newsletter / report may be reproduced in any form without its prior written consent to Ambit. All opinions, figures, charts/graphs, estimates and data included in this presentation / newsletter / report is subject to change without notice. This document is not for public distribution and if you receive a copy of this presentation / newsletter / report and you are not the intended recipient, you should destroy this immediately. Any dissemination, copying or circulation of this communication in any form is strictly prohibited. This material should not be circulated in countries where restrictions exist on soliciting business from potential clients residing in such countries. Recipients of this material should inform themselves about and observe any such restrictions. Recipients shall be solely liable for any liability incurred by them in this regard and will indemnify Ambit for any liability it may incur in this respect.

Neither Ambit nor any of their respective affiliates or representatives make any express or implied representation or warranty as to the adequacy or accuracy of the statistical data or factual statement concerning India or its economy or make any representation as to the accuracy, completeness, reasonableness or sufficiency of any of the information contained in the presentation / newsletter / report herein, or in the case of projections, as to their attainability or the accuracy or completeness of the assumptions from which they are derived, and it is expected each prospective investor will pursue its own independent due diligence. In preparing this presentation / newsletter / report, Ambit has relied upon and assumed, without independent verification, the accuracy and completeness of information available from public sources. Accordingly, neither Ambit nor any of its affiliates, shareholders, directors, employees, agents or advisors shall be liable for any loss or damage (direct or indirect) suffered as a result of reliance upon any statements contained in, or any omission from this presentation / newsletter / report and any such liability is expressly disclaimed. Further, the information contained in this presentation / newsletter / report has not been verified by SEBI.

You are expected to take into consideration all the risk factors including financial conditions, risk-return profile, tax consequences, etc. You understand that the past performance or name of the portfolio or any similar product do not in any manner indicate surety of performance of such product or portfolio in future. You further understand that all such products are subject to various market risks, settlement risks, economical risks, political risks, business risks, and financial risks etc. and there is no assurance or guarantee that the objectives of any of the strategies of such product or portfolio will be achieved. You are expected to thoroughly go through the terms of the arrangements / agreements and understand in detail the risk-return profile of any security or product of Ambit or any other service provider before making any investment. You should also take professional / legal /tax advice before making any decision of investing or disinvesting. The investment relating to any products of Ambit may not be suited to all categories of investors. Ambit or Ambit associates may have financial or other business interests that may adversely affect the objectivity of the views contained in this presentation / newsletter / report.

Ambit does not guarantee the future performance or any level of performance relating to any products of Ambit or any other third party service provider. Investment in any product including mutual fund or in the product of third party service provider does not provide any assurance or guarantee that the objectives of the product are specifically achieved. Ambit shall not be liable for any losses that you may suffer on account of any investment or disinvestment decision based on the communication or information or recommendation received from Ambit on any product. Further Ambit shall not be liable for any loss which may have arisen by wrong or misleading instructions given by you whether orally or in writing. The name of the product does not in any manner indicate their prospects or return.

The product ‘Ambit Coffee Can Portfolio’ has been migrated from Ambit Capital Private Limited to Ambit Investments Advisors Private Limited. Hence some of the information in this presentation may belong to the period when this product was managed by Ambit Capital Private Limited.

You may contact your Relationship Manager for any queries.

The performance data for coffee can product between 6th march 2017 - 19th June 2017 represents model portfolio returns. First client was on boarded on 20th June 2017. The performance data for G&C product between 1st June 2016 to 1st April 2018 also includes returns for funds managed for an advisory offshore client. Returns are calculated using TWRR method as prescribed under revised SEBI (Portfolio Managers) Regulations, 2020.