.jpg)

- After nearly a decade of subdued growth, India’s consumption sector is transitioning from a post-Covid, price/product mix-led recovery to a phase of gradual volume normalization.

- Over FY22–25, consumption growth was disproportionately driven by urban and premium cohorts, while mass and rural demand lagged due to weak real income growth. Nonetheless, we are now witnessing early signs of volume recovery across FMCG and select discretionary categories.

- The key catalysts driving this growth are 1) Rural demand recovery led by favorable factors, 2) Key Government initiatives to boost real income and 3) Company wise initiatives to drive higher consumption.

- While premiumization remains a structural feature of Indian consumption. Incremental growth is likely to more broad based, shifting the focus toward execution and portfolio breadth.

- We expect the next phase of consumption growth to be slower than the post-Covid rebound but structurally healthier, driven by a better balance between volume and product mix. This environment favors FMCG leaders and selects discretionary players (jewellery & apparel) with strong brands, scalable distribution and disciplined capital allocation. At the same time, stock-level dispersion within consumption sub segments is likely to widen.

Exhibit 1: Consumption growth robust only in FY06–12; just moderate after that period

1770783666321.jpg)

Source: Company, Ambit Capital research, Ambit Asset Management

We have considered revenues and domestic volume growth of listed FMCG co.

Exhibit 2: Phase-wise revenue & volume CAGR (FY04–08 vs FY20–25)

Source: Company, Ambit Capital research, Ambit Asset Management

Standalone employee expenses growth of NSE 500 companies taken as proxy for urban wage growth

Shift Toward Volume-Led Recovery to Drive Earnings Growth

Over FY22–25, headline consumption revenue growth was primarily price and product mix-driven, masking weak underlying volumes across mass FMCG and value discretionary categories. As inflation pressures ease, the nature of growth is beginning to change. Price increases have moderated, input costs have corrected and volume growth is gradually re-emerging as the primary driver of topline expansion. Early recovery is visible first in staples and daily-use categories, where affordability improves immediately with lower inflation.

This shift is critical for the sector. Volume-led growth is structurally healthier, supporting operating leverage, market share gains and more sustainable earnings. Even a low-single-digit volume recovery has an outsized impact on sector growth, given the large base and high operating leverage inherent in FMCG and scalable discretionary formats.

Investment implication:

As the cycle turns, companies best positioned to sustain growth are those with:

- Strong and diversified distribution networks, enabling consistent reach across channels

- Deep mass-market penetration, supporting volume recovery beyond premium cohorts

- Proven execution capabilities, particularly in pricing, innovation rollout, and cost control

Exhibit 3: FY20-25 saw ~53% of sector revenue growth being driven by price/product mix

Source: Ambit research, Ambit Asset Management

Premiumisation Remains Structural, but Growth Is Broad-based

Premiumisation continues to be the most durable structural driver of India’s consumption story, reflecting income polarisation, urbanisation and aspirational spending. Over the last few years, premium and upper-mass cohorts disproportionately supported sector growth, even as mass consumption remained under pressure.

However, the nature of premiumisation is evolving. After an extended period of above-trend growth, premium categories are now entering a phase of growth normalisation rather than acceleration.

Incremental growth is increasingly dependent on

- Innovation

- Brand strength

- Distribution execution

- Category expansion

Exhibit 4: Premiumisation in detergents has been one of the biggest success stories of a large consumer company in India

1770783677728.jpg)

Source: Ambit Asset Management

Exhibit 5: Portfolio mix of major FMCG players (Premium/Mid/Mass)

Source: Ambit Asset Management

Investment implication:

- Premium exposure alone is no longer sufficient to sustain above-trend growth.

- Clear product ladders are critical to drive both trading-up and volume expansion.

- Scalable adjacencies will differentiate long-term compounders from niche premium plays.

- Disciplined capital allocation becomes key as growth dispersion within premium categories widens.

Channel Shift: A Structural Enabler of Growth and Execution

Channel mix continues to be a structural driver of growth and execution quality within Indian consumption. Over the last decade, market share has steadily shifted from traditional trade toward modern trade, e-commerce and quick commerce, accelerating after COVID.

This shift has materially altered growth dynamics. Modern and digital channels enable faster product discovery, expanded premium assortment, and better price realisation, supporting premiumisation even when mass demand remains constrained. At the same time, traditional trade continues to dominate rural and value-led consumption, making depth of distribution critical for volume recovery.

Importantly, channel shift is also changing competitive intensity. Companies with strong MT relationships, digital readiness, and data-driven execution are gaining disproportionate shelf space and visibility, while those reliant solely on general trade are experiencing slower growth and weaker mix benefits.

Exhibit 6: E-Commerce Contribution to FMCG Sales

1770783688301.jpg)

Source: Ambit Asset Management

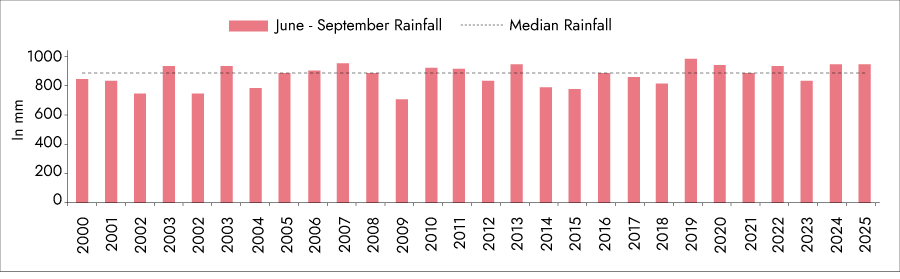

Rural Demand on a Gradual Recovery Path

Rural consumption has been a persistent drag on sector growth over the last several years, impacted by weak real wage growth, elevated food inflation and uneven agri incomes. This prolonged weakness constrained volume growth across staples and mass discretionary categories, even as urban demand remained resilient.

Recent data suggests early signs of stabilisation rather than a sharp rebound. Cooling food inflation has begun to improve real purchasing power, while better agri terms of trade and government support are supporting rural cash flows. Notably, the drag from sustained downtrading appears to be easing.

That said, we do not view rural demand as entering a high-growth phase. Structural constraints—income dispersion, employment quality and limited non-farm job creation—remain intact. However, even a modest improvement from depressed levels can materially influence sector volumes, given rural’s contribution to incremental demand.

Exhibit 7: Real rural wages growth improving

1770783698289.jpg)

Source: CEIC, Ambit Asset Management

Exhibit 8: Above-Average Monsoon Supporting Rural Demand

Source: Open Government Data (OGD), Ambit Asset Management

Exhibit 9: MSP growth in major crops remains in the mid-to-high single digits

1770783706016.jpg)

Source: Ambit Research, Ambit Asset Management

Exhibit 10: CPI Inflation at 20-year lows

Source: Ambit Asset Management

Investment implication:

- Rural exposure shifts to an earnings sustainability driver.

- Deep distribution strength becomes a key advantage in capturing recovery.

- Affordable price points support volume traction in staples and value-led discretionary.

- Strong execution differentiates winners as rural demand normalises.

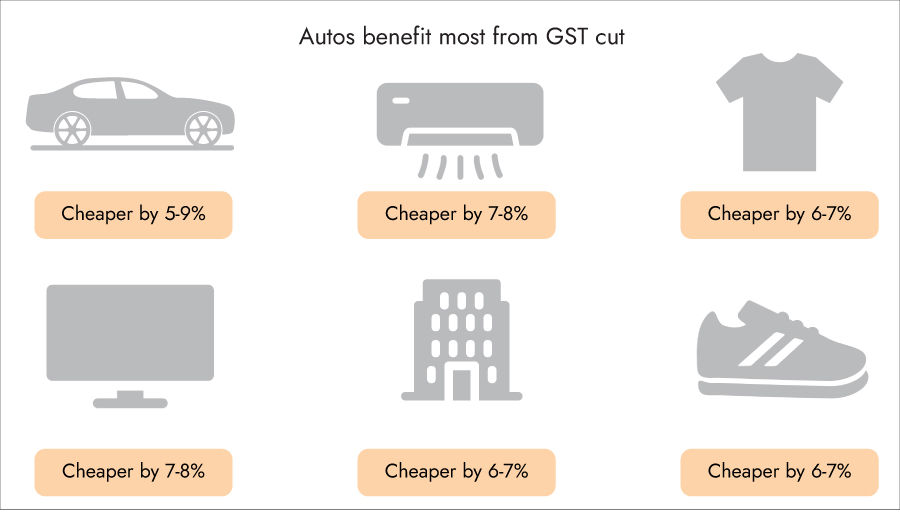

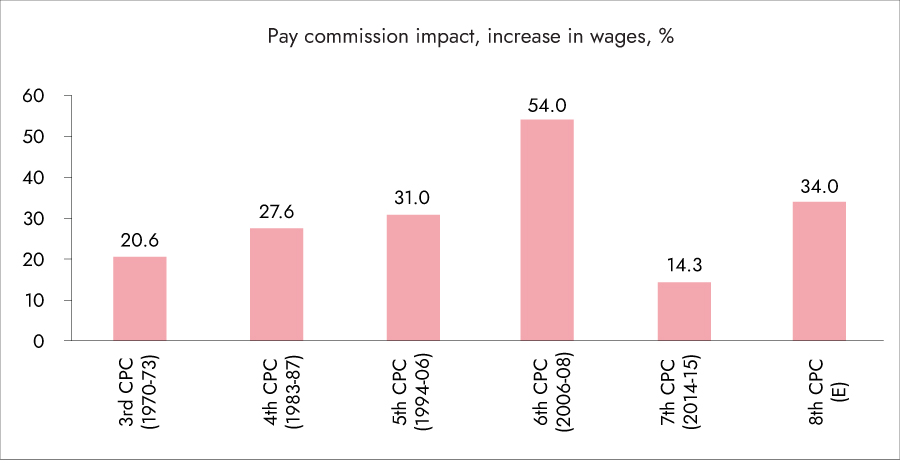

Government Initiatives to Drive Consumption

Government initiatives are increasingly supporting real income growth and consumption. State governments have rolled out targeted cash transfers and welfare schemes to boost disposable incomes, while policy measures such as GST rate rationalisation, the proposed 8th Pay Commission, and other fiscal interventions are expected to provide incremental tailwinds to household spending.

Source: Ambit Asset Management

Source: Ambit Asset Management

States have provided cash support to boost disposable incomes

Source: PRS, State Budgets, HCES (FY24), Ambit Capital Research, Ambit Asset Management

Investment implications:

- Lower downside risk to consumption demand

- Improved earnings visibility for consumer sectors

- Organised players better positioned to benefit

Select Discretionary – Growth broad based with Structural Tailwinds

After a strong post-Covid rebound, discretionary consumption is entering a phase of growth normalisation rather than a slowdown. Elevated inflation and higher ticket sensitivity over the last year have moderated near-term demand, particularly in urban categories. However, underlying structural drivers across select discretionary segments remain intact.

Rather than being macro-led, growth outcomes in discretionary consumption are increasingly execution-dependent, with sharp divergence across formats, brands and price points.

Jewellery: Formalisation continues to drive share gains

Jewellery remains one of the most structurally attractive discretionary categories, benefiting from organised share gains, brand trust and balance sheet strength. While near-term growth can be influenced by gold price volatility, formalisation and premiumisation continue to support steady market share gains for organised players.

This makes jewellery consumption less cyclical than perceived, with growth driven more by trust and replacement demand than discretionary impulses alone.

Exhibit 11: Robust Growth in Revenue and Stores for Organised Segment

Source: Technopak, Ambit Asset Management

1770783745859.jpg)

Source: Ambit Capital Research, Ambit Asset Management

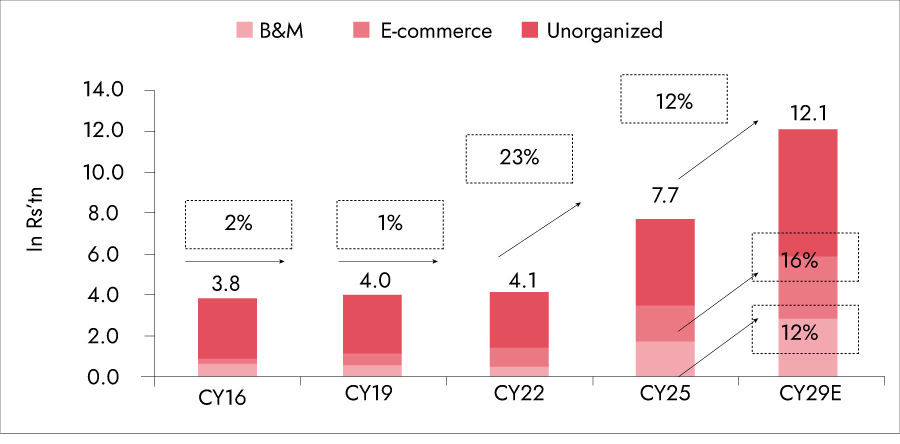

Apparel: Strong recovery, with faster shift from unorganised to organised players

Organised apparel is seeing a strong recovery, led by premium, occasion-led and branded segments, accelerating share gains over the unorganised market. Inventory discipline, faster design-to-shelf cycles and omni-channel reach are emerging as key differentiators. Growth is increasingly concentrated among players with strong brand recall and supply-chain agility, rather than a broad-based category rebound.

Exhibit 12: Apparel & Accessories market has grown at 23% CAGR over CY22-25 and is expected to grow at 12% CAGR over CY25-29

Source: Ambit Asset Management

Improving Earnings Quality for Staples company

The sharp input cost pressures that characterised FY22–23 have eased meaningfully, allowing companies to rebalance pricing, margins and brand investments. As price hikes taper and select price corrections are undertaken, the earnings cycle is transitioning toward operating leverage and mix-led growth.

This phase is marked by improving earnings visibility, cash flow generation and return ratios, particularly for companies that combine volume recovery with disciplined cost structures. Importantly, margin normalisation also enables higher, more consistent investments in advertising, innovation, and distribution, thereby reinforcing competitive moats.

While near-term margin expansion may moderate from recent peaks, earnings quality is structurally improving, with growth driven less by pricing and more by sustainable demand and execution.

1770783761831.jpg)

Source: Company, Ambit Capital research, Ambit Asset Management

Conclusion: The Next Phase of Consumption Growth

India’s consumption cycle is entering a phase of structural normalisation after an extended period of price-led growth and an uneven demand recovery. With inflation easing and input costs stabilising, the growth mix is gradually shifting toward volume recovery, improving the quality and sustainability of earnings across FMCG and select discretionary categories.

Premiumisation remains a durable long-term driver, but its contribution to incremental growth is normalising, making execution, portfolio depth and distribution strength increasingly important. At the same time, rural demand is transitioning from a structural drag to a cyclical stabiliser, offering downside protection rather than a sharp growth impulse.

Within discretionary consumption, growth outcomes are becoming more format- and company-specific, reflecting differences in execution, cost discipline and brand strength, rather than broad macro tailwinds.

Overall, the next phase of India’s consumption story is likely to be slower than the post-Covid rebound but more balanced and predictable, with greater dispersion in outcomes. For investors, this marks a shift from macro-driven optimism to a cycle where earnings quality and execution consistency will define long-term winners.

Ambit Coffee Can Portfolio

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has an unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced with disruptions at regular intervals. As the industry evolves or is faced with disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

Exhibit 13: Ambit Coffee Can Portfolio point-to-point performance

Source: Ambit Coffee Can Portfolio inception date is Jun 20, 2017;

**1M Return: 1st - 31st Jan'26; 3M Return: 1st Nov'25 – 31st Jan'26; 6M Return: 1st Aug'25 – 31st Jan'26; 1Y Return: 1st Feb'25 –31st Jan'26

*Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The performance related information provided herein is not verified by SEBI.

Exhibit 14: Ambit Coffee Can Portfolio calendar year performance

Source: Ambit Coffee Can Portfolio inception date is June 20, 2017;

*Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The performance related information provided herein is not verified by SEBI.

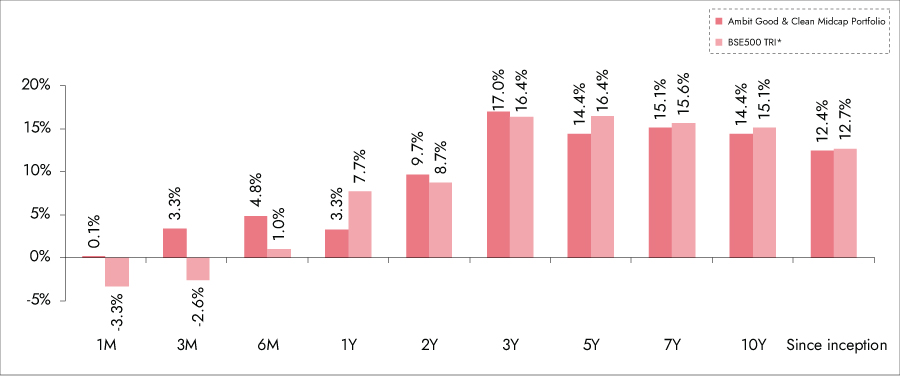

Ambit Good & Clean Midcap Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

1. Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

2. Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longerwith annual churn not exceeding20-25% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with these compounding earnings acting as the primary driver of investment returns over long periods.

3. Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

Exhibit 15: Ambit Good & Clean Midcap Portfolio point-to-point performance

Source: Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015;

**1M Return: 1st - 31st Jan'26; 3M Return: 1st Nov'25 – 31st Jan'26; 6M Return: 1st Aug'25 – 31st Jan'26; 1Y Return: 1st Feb'25 –31st Jan'26

*BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Midcap. The performance related information provided herein is not verified by SEBI.

Exhibit 16: Ambit Good & Clean Midcap Portfolio calendar year performance

Source:Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015;

*BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Midcap. The performance related information provided herein is not verified by SEBI.

Ambit Micro Marvels Portfolio

We aim to create a portfolio that invests predominantly in micro-cap companies with the potential of delivering superior earnings growth and generating relatively better risk-adjusted performance over a long period of time.

Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts while our proprietary ‘greatness’ framework helps identify efficient capital allocators. The result is a concentrated portfolio of 20-25 stocks that draws down less than the market in corrections and has low churn.

Key Features of Portfolio Companies:

1. High earnings growth companies with low leverage,

2. Market leaders or challengers with strong moat around brand, distribution, technology, and innovation,

3. Strong corporate governance coupled with apt capital allocation.

Exhibit 17: Ambit Micro Marvels Portfolio point-to-point performance

Source: Ambit Micro Marvels Portfolio inception date is Jul 29, 2024;

***1M Return: 1st - 31st Jan'26; 3M Return: 1st Nov'25 – 31st Jan'26; 6M Return: 1st Aug'25 – 31st Jan'26; 1Y Return: 1st Feb'25 –31st Jan'26

**BSE 500 TRI is the selected benchmark for the Ambit Micro Marvels Portfolio. The performance related information provided herein is not verified by SEBI.

*Nifty Smallcap 250 TRI is the secondary benchmark, being provided solely for additional reference and comparison. For details refer disclaimer clause.

Exhibit 18: Ambit Micro Marvels Portfolio calendar year performance

Source: Ambit Micro Marvels Portfolio inception date is Jul 29, 2024;

**BSE 500 TRI is the selected benchmark for the Ambit Micro Marvels Portfolio. The performance related information provided herein is not verified by SEBI.

*Nifty Smallcap 250 TRI is the secondary benchmark, being provided solely for additional reference and comparison. For details refer disclaimer clause.

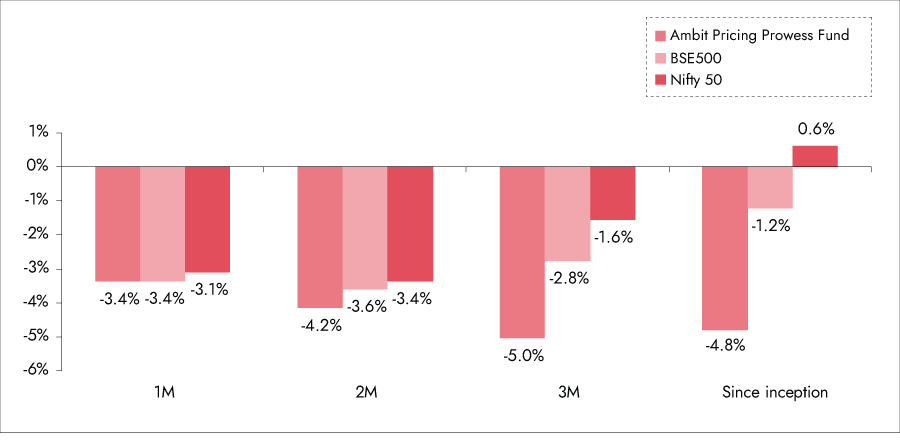

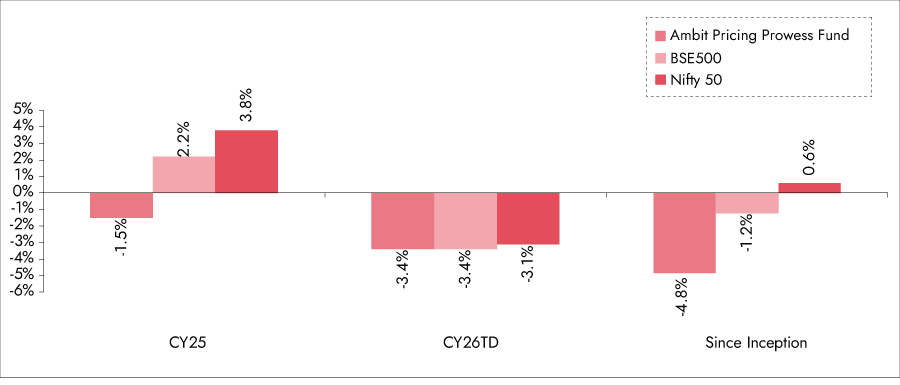

Ambit Pricing Prowess Fund

Ambit Pricing Prowess Fund is an All-weather, Open-ended, Long-only, Category III, Flexi-cap AIF – a meticulously crafted opportunity for long-term investors seeking:

- Accelerated Portfolio Returns: The ability to raise selling prices faster than input costs (inflation) directly increases profit margins and accelerates Free Cash Flow (FCF) growth.

- Unrivaled Portfolio Resilience: Pricing Power acts as a structural defense mechanism, stabilizing margins even during periods of macro pressure, supply shocks, or weaker demand.

- Maximum Long-Term Value Creation: Pricing Power is a proxy for an irrefutable competitive advantage (deep moat).

In a market of highly varied valuations, Ambit Pricing Prowess Fund is not constrained by a single market segment. We are designed to seek the most attractive combination of Quality and Price across the entire investment universe.

We can shift capital fluidly between Large, Mid, Small, and even a select number of carefully vetted unlisted businesses. This broad mandate allows us to find and capitalize on unique opportunities that align with our core framework.

Investing in businesses with Pricing Prowess offers compelling advantages, as below:

- Proven Inflation Hedge

- Maximized Profit Margins

- Stable, Quality Compounding (non-Glamorous)

- Formidable Entry Barriers

- Long-term Value Creation

Exhibit 19: Ambit Pricing Prowess Fund point-to-point performance

**1M Return: 1st - 31st Jan'26;2M Return: 1st Dec'25 - 31st Jan'26; 3M Return: 1st Nov'25 – 31st Jan'26

Note: First close for Ambit Pricing Prowess Fund was done on 24th Sept 2025; Returns are computed at Fund level and are pre fees and on pre-tax basis. Returns of BSE 500 and Nifty 50 is being provided solely for additional reference and comparison. The performance related information provided herein is not verified by SEBI.

Exhibit 20 - Ambit Pricing Prowess Fund calendar year performance

Note: Data as on 31st Jan 2026; First close for Ambit Pricing Prowess Fund was done on 24th Sept 2025; Returns are computed at Fund level and are pre fees and on pre-tax basis. Returns of BSE 500 and Nifty 50 is being provided solely for additional reference and comparison. The performance related information provided herein is not verified by SEBI.