Auto Sector has outperformed the BSE 500 in 2025 led by the GST cut announced recently

The recent GST cut announced by the Government of India has come as a big demand booster for the auto sector given that the cut has led to savings in the range of 6% to 8% across price points in 2W/4Ws/CV’s. More importantly, the tax savings have been the highest in the auto sector vs other sectors and hence the same is evident in the stock prices of several auto companies that have outperformed the BSE 500 since the announcement of GST cuts.

Autos have seen significant tax savings in the recent GST cut drive

Exhibit 1: Current versus previous tax structure

1768195618117.jpg)

Source: GOI, Ambit Asset Management

Exhibit 2: Resultantly, volumes have revived for both 4W and 2W segments

1767955025540.jpg)

Source: Vahan, Ambit Asset Management

Exhibit 3: Auto has been the disproportionate beneficiary of the GST cut across sectors…

1767955036111.jpg)

*31st December

Source: GOI, Ambit Asset Management

Exhibit 4: …resultantly, the Auto sector has outperformed the BSE 500 index post announcement of GST cut

1767955046140.jpg)

Source: Ambit Asset Management

Empirical evidence suggests that, GST cut led demand frenzy stays for 12-18 months

To assess the impact of price cuts on demand we go back to the early 2000’s where we saw excise duty cut playing out in the PV segment. In FY04 and FY05, car volumes grew 28% and 18%, respectively after excise duty was reduced from 32% to 24% in FY04. Similarly, the industry grew 21% and 12% in FY07 and FY08 when excise duty on small cars was reduced from 24% to 16% in FY07.

Exhibit 5: Empirical evidence suggests that, GST cut led demand frenzy stays for 12-18 months

1767955063771.jpg)

Source: Ambit Asset Management

The 8th pay commission disbursement in FY27 is likely to boost the auto demand. Last time when the 7th pay commission was announced in FY16, the PV and 2W volumes grew by 9% and 7% in FY17 and 8% and 15% in FY18.

Exhibit 6: Auto demand saw strong growth post the disbursement of the seventh pay commission

1767955073423.jpg)

6th pay commission implementation date was Jan’06; however, payout started in Sep’08 with arrears being paid in FY09 and FY10.

Source: Ambit Asset Management

Snowball effect at play in India’s auto sector

Chinese auto penetration increased significantly post its per capita income reaching USD 2,500

We believe the Indian auto sector is at a structural tailwind. India is at a stage where China was in FY07 when its per capita income was at $2.500. The Chinese auto sector saw significant improvement in car penetration when its per capita income crossed USD 2,500; cars owned per 1,000 population increased from 17 in 2007 (per capita income of USD 2,500) to 43 in 2010 (per capita income of USD 4,500) and 153 in 2019 (per capita income of USD 10,000)

Exhibit 7: USD 2,500 GDP per capita was an inflection point in China… for car penetration to increase rapidly

1768195633540.jpg)

Source: News Article, Ambit Asset Management

Exhibit 8: … for car penetration to increase rapidly

1768195643926.jpg)

Source: News Article, Ambit Asset Management

India is seeing a spree of high-speed corridors; the introduction of barrier barrier-free tolling system is an enabler

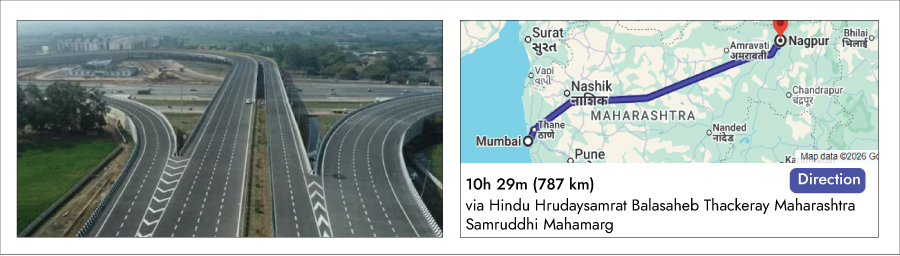

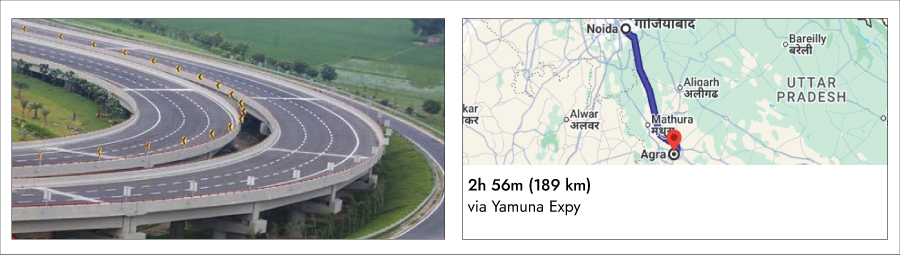

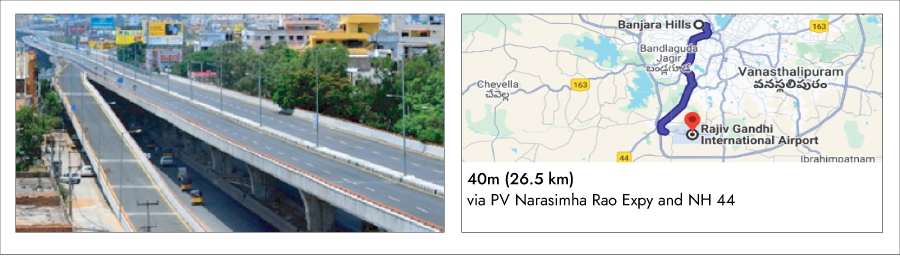

- New expressways and upgraded corridors are raising driving speed and comfort which will encourage people to own high-speed cars. Stretches such as Mumbai-Nagpur Samruddhi Expressway (can cover ~800 kms in 10 hrs) and Dahej-Ahmedabad corridor have demonstrated such shifts with consistently higher cruising speeds, lower travel times, and better mileage outcomes for consumers. This, alongside road infrastructure upgrades in major cities, can also add fuel to the increasing demand for high-speed cars.

Exhibit 9: Mumbai to Nagpur now in 10 hours – show 2 frames

Source: Google Maps, Ambit Asset Management

Exhibit 10: Noida to Agra now in 3hours

Source: Google Maps, Ambit Asset Management

Exhibit 11: Bandra to Colaba now in 19 mins

1767955233163.jpg)

Source: Google Maps, Ambit Asset Management

Exhibit 12: Banjara Hills to Rajiv Gandhi International Airport now in 48 mins

Source: Google Maps, Ambit Asset Management

- The upcoming rollout of barrier-free tolling systems will further enhance this trend by enabling seamless, high-speed toll collection without stopping at booths, reducing congestion, fuel wastage, and transit time. Several countries like China, Taiwan, Australia and France extensively use this technology

- China has one of the largest electronic toll collection networks in the world, with extensive free-flow ETC lanes on highways. This has helped reduce stop-and-go congestion on major routes and improve long-distance travel efficiency.

-

- Australia’s e-TAG system operates free-flow tolling on its toll roads, bridges and tunnels, allowing vehicles to pass without stopping and reducing travel time and congestion.

- France has started deploying barrier-free tolling on selected highways like the A79, where motorists no longer need to slow down or stop at toll plazas, helping improve traffic flow and reduce emissions.

Rising localization a big enabler of success - Availability of components improves and reduces costs

- Success of Vande Bharat is a case study: Indian consumers are extremely value-oriented. If they get convenience at an affordable cost, then demand explodes. The rising popularity of Vande Bharat is a classical case study; despite ticket prices for Vande Bharat being higher by ~20-30% vs express trains the demand is rising consistently as the travel experience is superlative vs the increase in ticket price and time savings of ~20% is icing on the cake. The secret sauce of ticket prices being affordable is 75-80% of localization (As per media articles) in building this train; ticket prices for similar trains in other countries like Europe are ~8x higher.

- India auto sector at the cusp of rising localization: In the last 5 years, we have seen several luxury/premium brands increasing investments in manufacturing in India. We believe this is very critical in increasing their share as local manufacturing not only helps with making the car more affordable but also boosts the availability of both new vehicles and components (critical for the timely servicing of vehicles).

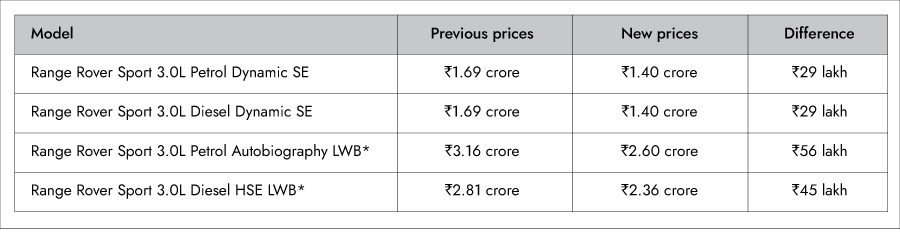

Jaguar Land Rover announced local assembly of Range Rover and Range Rover Sport SUVs in 2024 to cater exclusively to local demand. This helped buyers enjoy significant (>15%) savings on these luxury SUVs and resultant sales jumped from 3,800 units in FY24 to 5,400 units in FY25 (up 40%)

Exhibit 13: Range Rover sales jumped by ~50% post-increase in localization

Source: Ambit Asset Management

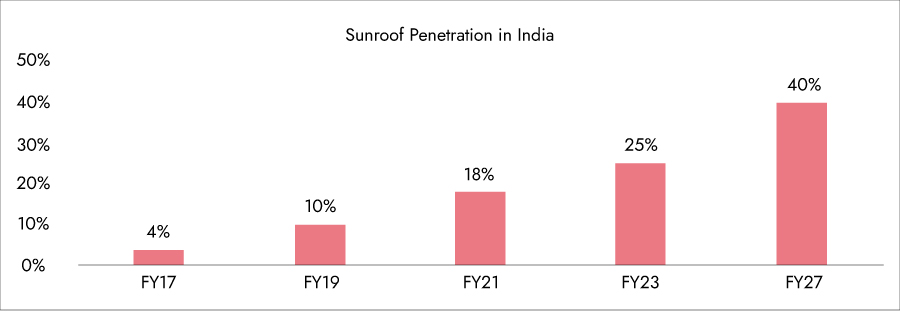

- Several existing cars have seen significant upgrades post rise in localization: Indian car customers have shifted significantly from prioritizing only fuel efficiency (“Kitna deti hai?”) to demanding advanced technology and features (“Features kya hai?”) along with increasing focus on safety. There are several case studies of existing cars seeing a significant upgrade in features post their rising localization. Post the localization in sunroof manufacturing and components for ADAS, we have seen several existing cars getting re-launched with embedded ADAS technology and sunroof. Sunroofs started getting manufactured in India in FY22 by companies like Webasto and Gabriel India and this became the inflection point for the rise in penetration of cars with sunroofs.

Exhibit 14: Share of cars with sunroofs has been rising consistently

Source: News Article, Ambit Asset Management

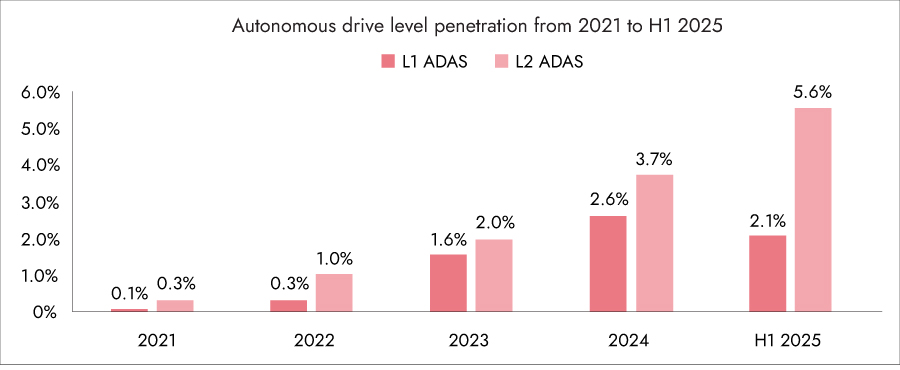

Likewise, Advanced Driver Assistance Systems (ADAS) technology is being developed, tested, and partially manufactured in India, though much of the core hardware (like sensors and chips) is still supplied by global companies. The Automotive Research Association of India (ARAI) has built a dedicated testing facility in Pune to help develop and validate ADAS technology suited to Indian road conditions. Indian companies like VVDN Technologies are working to localize ADAS components and related electronics. Partnerships such as Mobileye + VVDN aim to bring more ADAS manufacturing capacity into India. India is targeting more indigenous development and localization of the ADAS stack — including software and some hardware adaptation — partly through local R&D and partnerships (e.g., Qualcomm reportedly working on an India-specific ADAS stack)

Exhibit 15: Share of cars with ADAS has been rising…

Source: JATO Dynamic, Ambit Asset Management

Several OEMs have also given positive commentary around the Indian auto sector being at an inflection point

- Maruti Suzuki: "I believe the government will recognize that lowering tax rates does a substantial amount of good in respect of production increase, in terms of people getting more convenient means of transport, and ultimately in raising the tax collections of the government also."

- Mahindra and Mahindra: “Overall, I think this is a very, very good move by the government because for the longer term, it simplifies things as well as reduces GST. And there will be, in our view, a fairly strong multi-year benefit from this move” (Q2 FY26 Result Commentary)

- TVS Motor Company: “And I'm very sure these GST reforms are going to help rural and the connectivity -- the road connectivity infrastructure investments in India have been brilliant. So I'm pretty confident that -- and I always believe that mobility needs in India, with a lot of self-employed people, 2-wheeler is the best mobility solution. And rural is the most important driver.”

- Hero MotoCorp: “We expect the momentum in growth to continue, supported by benefits flowing in from the GST reforms, healthy macroeconomic parameters and a robust product portfolio. Moving forward, our journey of investment behind growth will continue. This timely intervention significantly uplifted the consumer sentiment and revitalized retail momentum across the markets.

- Hyundai India: “GST 2.0 marks a transformative milestone and brings renewed wave of optimism – one that fuels growth, enhances ease of doing business and strengthens consumer confidence. It is a reform that sets the tone for sustained industry momentum, including empowering millions of customers by making personal mobility more affordable and accessible. Following the implementation of GST 2.0 reforms, the Indian automobile industry witnessed a strong wave of demand momentum."

To conclude, we believe India’s auto sector growth story is underpinned by a powerful mix of structural, cyclical and policy-driven tailwinds. Rising per capita income, rapid urbanization and improving road infrastructure are expanding personal mobility aspirations, while a young demographic and low vehicle penetration versus global peers provide a long runway for demand. Government's focus on road infrastructure is improving average driving speeds and fuel efficiency. On the supply side, India is emerging as a global manufacturing hub, supported by high localization, competitive cost structures and increasing integration into global OEM supply chains. Technology shifts—such as premiumization, higher safety and emission norms, electronics content, and the gradual transition to EVs—are driving higher value addition per vehicle, benefiting both OEMs and auto ancillaries. Together, these factors position the Indian auto sector not just as a cyclical play, but as a long-term compounding growth story with increasing global relevance.

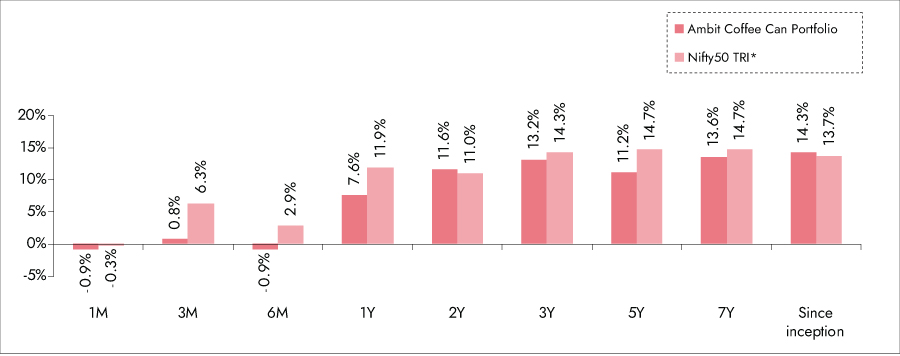

Ambit Coffee Can Portfolio

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has an unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced with disruptions at regular intervals. As the industry evolves or is faced with disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

Exhibit 16: Ambit Coffee Can Portfolio point-to-point performance

Source: Ambit Coffee Can Portfolio inception date is Jun 20, 2017;

**1M Return: 1st - 31st Dec'25; 3M Return: 1st Oct'25 – 31st Dec'25; 6M Return: 1st Jul'25 – 31st Dec'25; 1Y Return: 1st Jan'25 –31st Dec'25

*Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The performance related information provided herein is not verified by SEBI.

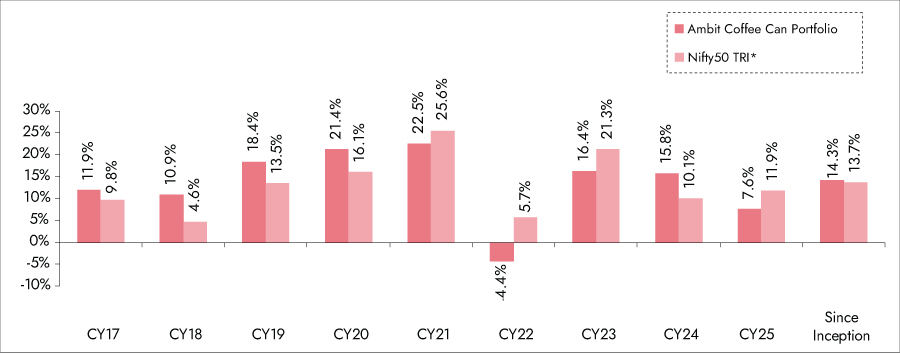

Exhibit 17: Ambit Coffee Can Portfolio calendar year performance

Source: Ambit Coffee Can Portfolio inception date is June 20, 2017;

*Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The performance related information provided herein is not verified by SEBI.

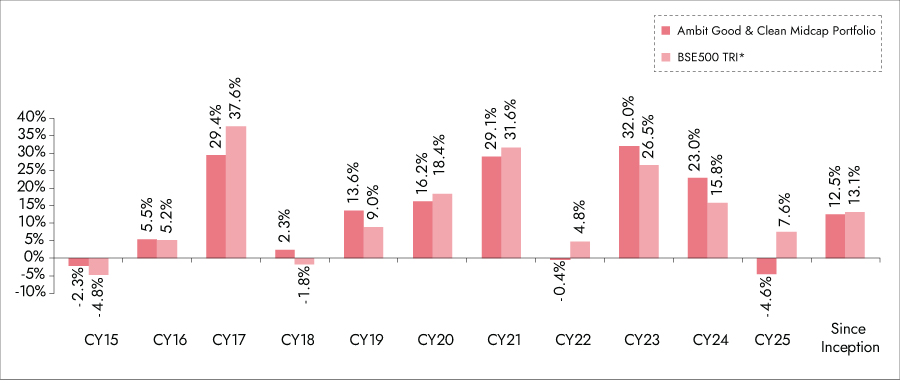

Ambit Good & Clean Midcap Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

1. Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

2. Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longerwith annual churn not exceeding20-25% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with these compounding earnings acting as the primary driver of investment returns over long periods.

3. Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

Exhibit 18: Ambit Good & Clean Midcap Portfolio point-to-point performance

Source: Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015;

**1M Return: 1st - 31st Dec'25; 3M Return: 1st Oct'25 – 31st Dec'25; 6M Return: 1st Jul'25 – 31st Dec'25; 1Y Return: 1st Jan'25 –31st Dec'25

*BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Mid cap. The performance related information provided herein is not verified by SEBI.

Exhibit 19: Ambit Good & Clean Midcap Portfolio calendar year performance

Source: Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015;

*BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Mid cap. The performance related information provided herein is not verified by SEBI

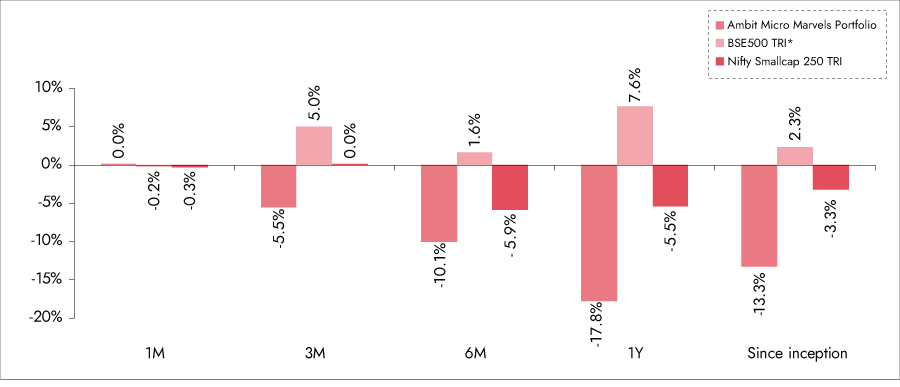

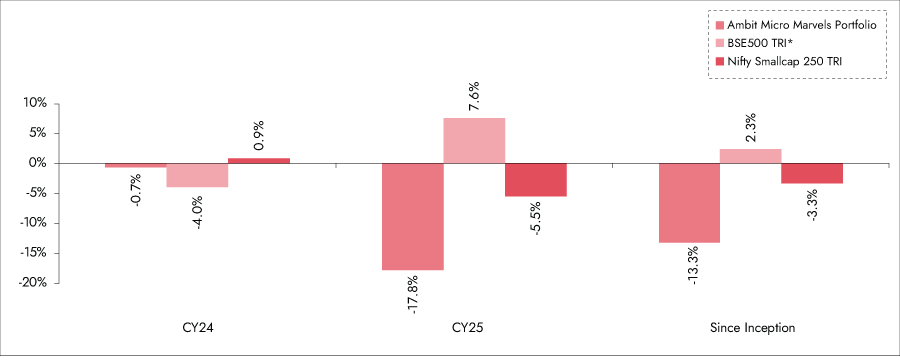

Ambit Micro Marvels Portfolio

We aim to create a portfolio that invests predominantly in micro-cap companies with the potential of delivering superior earnings growth and generating relatively better risk-adjusted performance over a long period of time.

Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts while our proprietary ‘greatness’ framework helps identify efficient capital allocators. The result is a concentrated portfolio of 20-25 stocks that draws down less than the market in corrections and has low churn.

Key Features of Portfolio Companies:

1. High earnings growth companies with low leverage,

2. Market leaders or challengers with strong moat around brand, distribution, technology, and innovation,

3. Strong corporate governance coupled with apt capital allocation.

Exhibit 20: Ambit Micro Marvels Portfolio point-to-point performance

Source: Ambit Micro Marvels Portfolio inception date is Jul 29, 2024;

***1M Return: 1st - 31st Dec'25; 3M Return: 1st Oct'25 – 31st Dec'25; 6M Return: 1st Jul'25 – 31st Dec'25; 1Y Return: 1st Jan'25 –31st Dec'25

**BSE 500 TRI is the selected benchmark for the Ambit Micro Marvels Portfolio. The performance related information provided herein is not verified by SEBI.

*Nifty Smallcap 250 TRI is the secondary benchmark, being provided solely for additional reference and comparison. For details refer disclaimer clause.

Exhibit 21: Ambit Micro Marvels Portfolio calendar year performance

Source: Ambit Micro Marvels Portfolio inception date is Jul 29, 2024;

**BSE 500 TRI is the selected benchmark for the Ambit Micro Marvels Portfolio. The performance related information provided herein is not verified by SEBI.

*Nifty Smallcap 250 TRI is the secondary benchmark, being provided solely for additional reference and comparison. For details refer disclaimer clause.

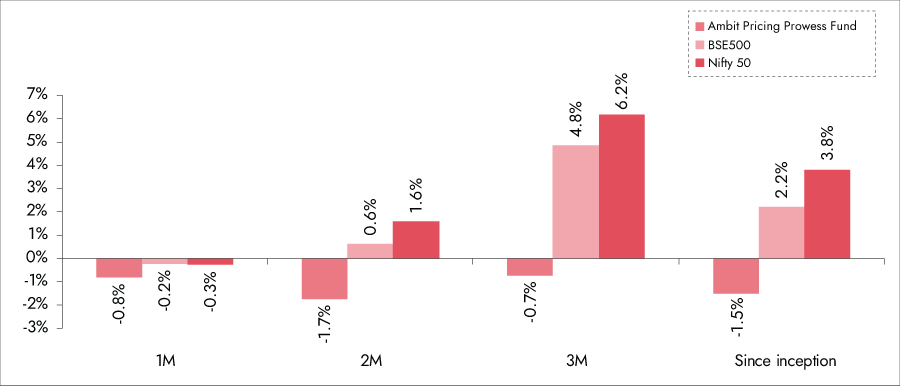

Ambit Pricing Prowess Fund

Ambit Pricing Prowess Fund is an All-weather, Open-ended, Long-only, Category III, Flexi-cap AIF – a meticulously crafted opportunity for long-term investors seeking:

- Accelerated Portfolio Returns: The ability to raise selling prices faster than input costs (inflation) directly increases profit margins and accelerates Free Cash Flow (FCF) growth.

- Unrivaled Portfolio Resilience: Pricing Power acts as a structural defense mechanism, stabilizing margins even during periods of macro pressure, supply shocks, or weaker demand.

- Maximum Long-Term Value Creation: Pricing Power is a proxy for an irrefutable competitive advantage (deep moat).

In a market of highly varied valuations, Ambit Pricing Prowess Fund is not constrained by a single market segment. We are designed to seek the most attractive combination of Quality and Price across the entire investment universe.

We can shift capital fluidly between Large, Mid, Small, and even a select number of carefully vetted unlisted businesses. This broad mandate allows us to find and capitalize on unique opportunities that align with our core framework.

Our focus is more on business fundamentals, rather than stock price movements. We do not seek comfort of the crowd and seek exposure to companies that are "unrecognized" because the market either misprices the longevity of their growth or fails to fully appreciate the structural defense their pricing power provides.

The framework's final structure—blending Established (proven track record, mature moats) and Emerging (new, rapidly widening moats, higher growth potential) Pricing Power plays—provides a balanced approach to capture both resilience and accelerated return potential within the portfolio.

Investing in businesses with Pricing Prowess offers compelling advantages, as below:

- Proven Inflation Hedge

- Maximized Profit Margins

- Stable, Quality Compounding (non-Glamorous)

- Formidable Entry Barriers

- Long-term Value Creation

Exhibit 22: Ambit Pricing Prowess Fund

**1M Return: 1st - 31st Dec'25; 2M Return: 1st Nov'25 – 31st Dec'25; 3M Return: 1st Oct'25 – 31st Dec'25

Note: First close for Ambit Pricing Prowess Fund was done on 24th Sept 2025; Returns are computed at Fund level and are pre fees and on pre-tax basis. Returns of BSE 500 and Nifty 50 is being provided solely for additional reference and comparison. The performance related information provided herein is not verified by SEBI.