This should benefit Ambit Asset Management’s distinctive bottom-up investment style which is marked by low beta, capital protection, commitment to quality and concentrated portfolios. In this newsletter, we discuss:1) Return of Quality Investing Style, 2) Snowball Effect on Investing, and 3) Quality and Longevity aspect of one of our portfolio holdings, Abbott India.

1) Return of Quality

In the ever-evolving landscape of investments, all styles are susceptible to cycles. Over the past three years, we have observed a market characterized by high beta, risk-on sentiment, retail-led participation and a broad-based rally. Recent market move has been primarily characterized by deep cyclicals, asset heavy businesses, low ROE and FCF generators. During such high beta bull cycles, disciplined long-term investing styles and investing principles go out of favour. Short-termism and greed prevail. There is a rush to go down the quality curve and take higher risks. The past few years’ low volatility and shallow drawdowns have pushed investors to take higher risks and a high beta style of investing. This sets the stage for a market shakeout and eventual manifestation of the No.1 risk, permanent capital loss. This investor behaviour is what causes investment style cycles.

Having a quality focused portfolio is the cornerstone of an equity portfolio. As it enables in building resilient portfolios for long term wealth creation. Compounders, which exhibit characteristics such as strong franchise durability, high cash flow generation, low capital intensity, and unleveled balance sheets have delivered superior risk-adjusted returns across economic cycles. The long-term outperformance of the quality style of investing is well documented.

There has been many empirical research, which document the long-term outperformance of quality by Sloan (1996), Novy-Marx (2013) and Fama & French (2014). Even Benjamin Graham, the founding father of value investing, was among the pioneer investors to recognize the importance of investing in high-quality companies (Graham, 1973). By picking stocks that are profitable, growing, safe, and well managed in recent past, one can succeed in picking stocks that display these features in future.

Empirical returns also support Quality investing, with high Quality stocks outperforming low Quality ("Junk") stocks, on average. Both approaches suggest that advantage is nonlinear, with the greatest impact coming from Junk stock underperformance.

Exhibit 1: Rolling 10 Year Annualized Performance of US Factors vs US Equities, since 1990’s

Source: Kenneth French Data Library (2022), Ambit Asset Management

Exhibit2: Global historical Quality Portfolio Returns by Size and Returns

Source: AQR Data Library; US data from 1957, Global data 1987; Quality proxy Wisdom Tree US Quality Growth TRI Index

Exhibit 3: Quality is more resilient and has had lower drawdowns in most of US market crashes

Source: Kenneth French Data Library (2022); Quality proxy Wisdom Tree US Quality Growth TRI Index

While the quality growth investing style outperforms across cycles, during high beta expansion rallies it underperforms, which is what we witnessed from March 22 – May 24. We feel, Quality's relationship with Lottery-ness and Retail investor preferences is critical for understanding its recent underperformance. We expect a sharp revert to quality investing hereon.

Exhibit 4: Quality outperforms across most cycles

Source: Ambit Asset Management/ Reuters

Recent Quality underperformance has been driven by bottom quartile’s high returns

Ambit Capital Research has a proprietary model which ranks all listed companies based on accounting and ESG factors, into Decile 1 (D1) to Decile 10 (D10), wherein D1 is high quality and D10 low quality. These deciles are further divided into three groups – Zone of Safety (D1 to D5); Zone of Pain (D6 to D7) and Zone of Darkness (D8 to D10). The exhibit below plots compound portfolio returns of the same Quality decile-sorted portfolios. The overall underperformance of quality factor is largely due to the bottom quartile’s high returns.

Exhibit 5: Median stocks perf till Dec’21 Exhibit 6: Median perf last 2 Yrs (Jan’22-Jan’24)

Source: Ambit Capital Research; Universe BSE500 (ex BFSI); Jan’24

Exhibit 7: SMID share in total free float market cap is at all time high level of ~33% Exhibit 8: Quality has underperformed in the last 1 yr

Source: Ambit Capital Research; Ambit Asset Management Source: NSE; Ambit Asset Management

Some Behavioral Bias which explains Quality underperformance, over FY21-24

We feel, Quality's relationship with Lottery-ness and Retail investor preferences is critical for understanding its recent underperformance.

Summary:

- Investors today are overestimating the success probability of many narrative driven sectors and stocks. We feel, behavioral biases and Quality's relationship with Lottery-ness and Retail investor preferences is critical for understanding recent underperformance of quality investing style. We expect investor focus to shift sharply towards capital protection and quality style of investing.

- Post-election results the likelihood of policy rebalance is high, which could boost overall consumption sentiments and lead to shift towards asset light, high ROE and high FCF generating sectors and stocks.

- While market cycles come and go, our conviction in the merits and effectiveness of this time-tested strategy remains unwavering. At Ambit Asset Management, our primary focus is to be the first choice of portfolio for investors who believe in the quality focus, capital protection first as a motto and have a long-term investment mindset.

2) Snowball effect on investing

We believe adoption of a ‘Quality Investing Focus’ and ‘Long-term Investment Mindset’ can enable investors to have the ‘Wealth Snowball Effect’. The snowball effect, also known as compounding, is a powerful financial concept that relies on the exponential growth of an investment's value over time. At its core, it involves reinvesting the returns generated by an investment to earn even more returns. This cycle repeats, and as time goes by, the investment grows at an accelerating rate, much like a snowball rolling down a hill, picking up more snow as it goes. We at Ambit Asset Management believe that to benefit from the snowball effect on investment, the following three key factors need to be present: a) Quality focus, b) Lindy effect or growth longevity and c) Long-term investment mindset.

a) Quality focus

For the snowball effect on investing to play out, the most important factor is that the underlying ‘company’ has quality and growth longevity. We believe that without quality focus the No. 1 risk of permanent capital loss and high drawdowns increases sharply.

Unlike standard factors like value, momentum and size, quality lacks a commonly accepted definition. Acclaimed researchers Clifford S. Asness, Andrea Frazzini and Lasse H. Pedersen in their research paper, ‘Quality Minus Junk’, define quality security as one that has characteristics that, all-else-equal, an investor should be willing to pay a higher price for stocks that are safe, profitable, growing and well-managed. High-quality stocks do have higher prices on average, but not by a very large margin when adjusted for growth longevity and pricing power, which investors are often not able to ascertain upfront. This largely explains why quality stocks have high risk-adjusted returns.

A research paper by Jason Hsu, Vitali Kalesnik and Engin Kose attributes the ‘Quality Premium’ to profitability, accounting quality, payout/dilution and investments, of which profitability and investment-related characteristics tend to capture most of the quality-related premium. We use a mix of quantitative and qualitative filters to identify such companies. In our view, the result of companies with such characteristics is pricing power.

Exhibit 9: Sample Quantitative and Qualitative Screening for one of the portfolio companies

Source: Ambit Asset Management/ (above analysis for Abbott India)

b) Lindy effect – Longevity of growth

Successful compounders have a few key characteristics and patterns. So, the key variable to focus on for companies is the durability (staying power) of these competitive advantages which makes them enduring. When a company’s competitive advantages are truly enduring it doesn’t change from year to year. In fact, it increases over time, and this is what makes these companies’ business models unique, where growth perpetuates more growth. In this regard, buying companies with the Lindy advantage is key to enabling ‘Wealth snowball effect on investing’.

Lindy's Law was popularized by Nassim Nicholas Taleb, an influential mathematician known for his work in risk management and statistical analysis and a famous author of books such as Black Swan, Antifragile, Skin in the Game and many others. Lindy effect is an observable phenomenon that provides insights into the survivorship of non-perishable, intangible items such as ideas, technologies, companies and cultural works.

"The Lindy effect is a concept that the future life expectancy of some non-perishable things like a technology or an idea is proportional to their current age so that every additional period of survival implies a longer remaining life expectancy. Where the Lindy effect applies, mortality rate decreases with time." — Nassim Taleb. According to this concept, the future life expectancy of such items is proportional to their current age.

This explains one common anomaly why investors keep underestimating the intrinsic value of established growing enduring companies. Investors in such companies are not able to properly measure the ‘Competitive Advantage Period (CAP)’, as popularized by Michael Mauboussin. Hence they keep underestimating their growth longevity and hence its intrinsic value. A proper understanding of the Lindy Effect helps investors in building a portfolio of companies, with higher resilience and stability across cycles.

Exhibit 10: Lindy effect in play

Source: Ambit Asset Management

The table below shows some of the most consistent and biggest wealth creators in India, most of which benefit significantly from the Lindy advantage. A screening of some of these names, with quantitative filters like Growth, ROE and Reinvestment, throws up a very interesting list of enduring wealth creators, across sectors for further bottom-up fundamental research. Not surprisingly almost ~70% of companies with Lindy effect are large caps, while mid and small account for ~30%.

Exhibit 11: Some of the most consistent and biggest wealth creators benefit from the Lindy effect

Source: Ambit Asset Management/ NSE/ BSE

c) Long-term investment mindset

The cornerstone of successful investing lies in the concept of 'compounding,' a magical force that unfolds its true potential over the long term and necessitates a 'long-term mindset to investing.' Despite this knowledge, numerous behavioral biases and institutional imperatives often hinder investors from fully capitalizing on this opportunity.

A mismatch of time horizons leads some investors to weigh the short term more heavily and de-emphasize sources of “enduring business advantage”. Instead of attempting to determine how the crowd will react this quarter or how the trajectory of the business will fare this year, our focus is on the factors that contribute to determining the ultimate intrinsic value of the company.

We believe the mindset of being on a constant search for compounders is a better use of time than exhausting one’s intellectual capital and time on trading in and out of stocks and segments of the market in a desire to look good in the short term. Hence, our focus is on identifying companies that can successfully increase the duration of their competitive advantage period and growth magnitude.

Our investment strategy is meticulously crafted to navigate these challenges, aiming to achieve our investment objectives while steering clear of common behavioral biases and institutional imperatives.

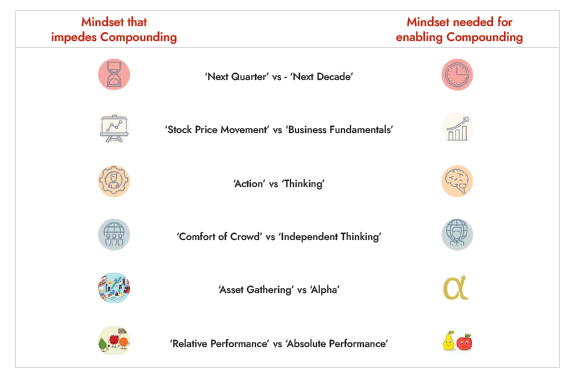

What impedes successful compounding?

Exhibit 12: Short termisn is the bane of successful compounding

Source: Ambit Asset Management

Conclusions:

- We believe the momentum-driven rally in various Junk and speculative SMID stocks has played out and is now ripe for a major reversal (Refer to our recent newsletters). The unwinding of Junk and speculative SMID stocks could be painful. Investment maturity and risk-mitigating measures of marginal new investors remain untested.

- We believe the adoption of Quality Investing and a Long-term Investment Mindset can enable investors to have the ‘Wealth Snowball Effect on Investing’

- While market cycles come and go, our conviction in the merits and effectiveness of this time-tested strategy remains unwavering. At Ambit Asset Management, our primary focus is to be the first choice of portfolio for investors who believe in the quality focus, capital protection first as a motto, and have a long-term investment mindset.

3) Abbott India - A unique play

Abbott India is an innovation-focused MNC healthcare company with a broad portfolio of market-leading products that are well aligned with long-term healthcare trends in India. Its comprehensive portfolio covers multiple therapeutic categories such as women’s health, gastroenterology, neurology, thyroid, pain management, vitamins, and vaccines. We believe the market is yet to fully appreciate the uniqueness of this pharmaceutical company.

Abbott’s consistency and sustained high growth over the last 10 years (sales CAGR of ~11% and PAT CAGR of ~21%), in the midst of muted industry growth and increasing competitive intensity, are noteworthy. If one were to rank high-growth resilient companies across domestic pharmaceutical and consumer staples in terms of growth, consistency and enduring moats, Abbott would emerge as the top-ranking one across both sectors. As such, it is one of the most unique companies under our ‘Established Coffee Can Companies’ bucket.

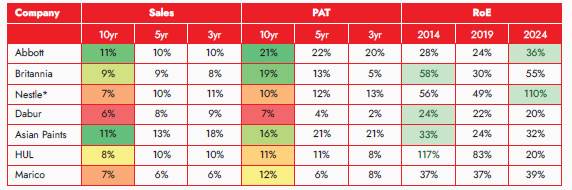

Abbott compares favourably across key consumer staples companies on growth

The Indian Pharmaceutical Market is often compared with consumer staples companies given the nature of the business. This comparison is all the more true for Abbott given single geography focus, strong brand positioning and chronic nature of the portfolio. Its financial footprint resembles that of a consumer company – it has an asset-light model, negative working capital, high OCF/EBITDA and PAT/FCF conversion, ROCE >30%, PAT margin >15% and payout ratio of >75%.

If we compare Abbott’s performance over the last decade to a few leading consumer companies, Abbott stands out on almost all parameters. It had the highest PAT CAGR of 20%+ over the last decade. Moreover, it is one of the very few companies in this cohort that has seen RoE improvement over the last decade. While most consumer companies have benefitted significantly in the last 10 years from increasing their distribution reach; we feel this tailwind is yet to play out for Abbott as it is still primarily an urban-dominated company.

Exhibit 13: Abbott has demonstrated superior growth than key consumer staples companies

Source: Ambit Asset Management, Company

Note * - CY23 end for Nestle

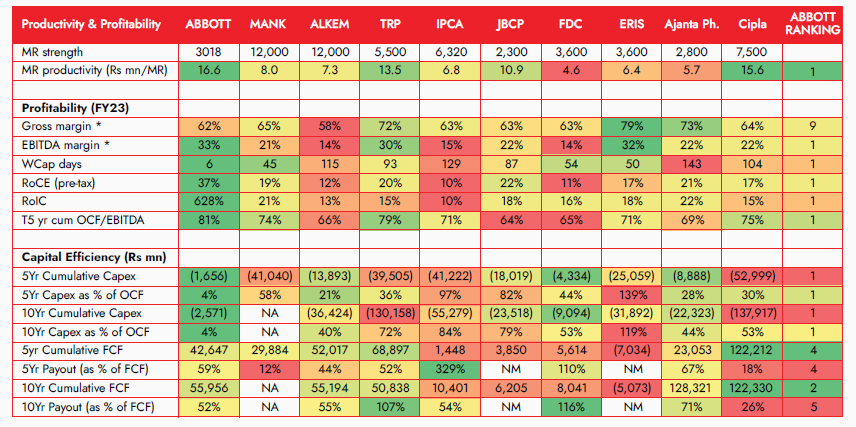

Abbott stands out across domestic pharma companies for its capital efficiency

Abbott India focuses on creating therapies rather than just brands. Abbott is a leader in most of the therapies it operates in. This strong brand recall is visible in its high MR productivity among peers. Furthermore, Abbott trumps other domestic-focused pharma companies across key parameters such as core organic growth, capital efficiency, return ratios, core margins and profitability.

Most of its domestic and MNC peers face issues such as high capex intensity, high R&D spending, dependence on inorganic initiatives for growth, low return ratios, stagnant core growth, margin volatility, high working capital, high regulatory risks and governance issues. Abbott has none of these issues. Over FY14-23, Abbott generated INR47.7b OCF, undertook capex of only INR5b, generated FCF of INR42b and paid out INR29.5b in dividends.

Exhibit 14: Abbott stands out when compared to domestic companies

Source: Ambit Asset Management, Company

* Adjusted for Novo Nordisk business

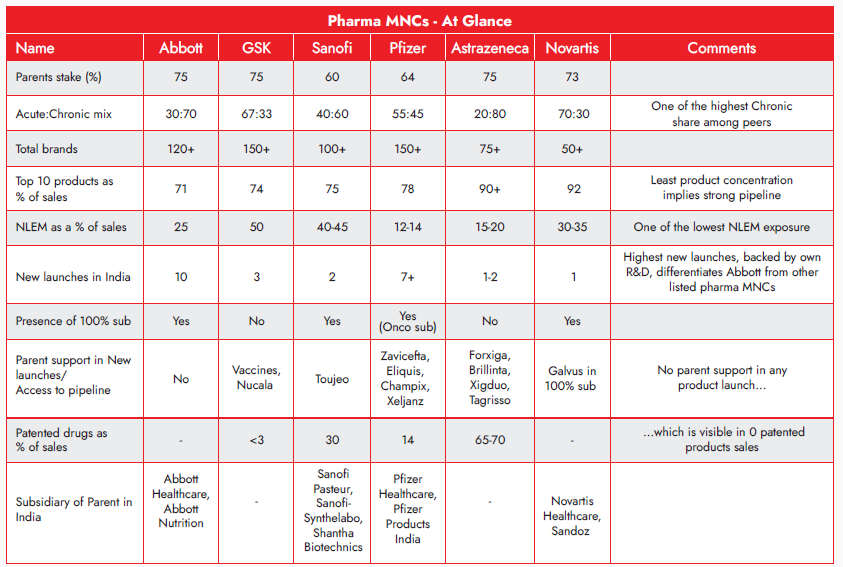

Exhibit 15: Abbott stands out when compared to MNC pharma companies

Source: Ambit Asset Management, Company

Concerns:

- FII ownership restriction – Currently, foreign investment in a company engaged in the brownfield pharmaceutical sector in India is permitted up to 74% via automatic route, beyond which one would require additional approval from various government agencies. This restricts FII/FPI participation in MNC stocks such as Abbott where the promoters hold >70%. In addition to this, such restriction also negates any future scope of domestic or overseas (MSCI etc.) index inclusion, thus invariably playing down on valuations. While any change in FDI norms in this account can be a key trigger for Abbott, we feel, for companies with strong fundamentals like Abbott such technical factors are not necessary.

- Parent has unlisted entities – Most pharma MNCs in India have been operating since the 1960s. Government regulation in the 1970s and the subsequent amendment of the Foreign Exchange Regulation Act (FERA) capped foreign ownership in Indian companies to 40%. This necessitated some of the highest quality businesses to either get listed or exit from India. Nonetheless, in case of Abbott: 1) The parent, Abbott Labs, does not have any pipeline of high-margin, lucrative, innovative products which makes Abbott one of the only listed pharma MNCs in India that does not get any support from the parent in terms of new launches or innovative products. 2) Even though Abbott Labs has multiple subsidiaries in India, there is no conflict of interest among these as the therapy areas for each are clearly defined and there’s no patent product to be launched by the parent.

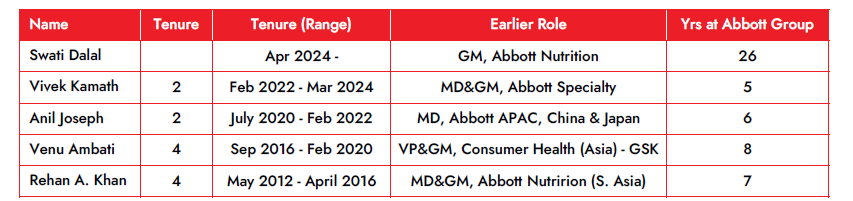

- Top management volatility – Abbott’s rise as a strong pharmaceutical brand in India was led by Mr Rehan Khan in the 2010s, which was pushed forward by Mr Venu Ambati when he took over in 2016. However, in the ensuing 4 years, ever since Mr Venu was promoted to global role within Abbot Group in 2020. Abbott India has seen three different MDs at the helm. Though this churn does not seem to have impacted the company’s performance adversely, it is a cause of concern. While we would have certainly loved more certainty at the helm, we are reminded of a famous quote by Peter Lynch – "invest in businesses any idiot could run because someday one will." The new CEO is an old-timer at Abbott Group and hopefully will have a longer stable stint and provide the much needed growth impetus.

c. Top management volatility - Abbott’s rise as a strong Pharmaceutical brand in India was led by Mr Rehan Khan in the 2010s, which was pushed forward by Mr Venu Ambati when he took over in 2016. However, in the ensuing 4 years since Mr Venu was promoted to global role within Abbot Group in 2020. Abbott has seen three different MDs at the helm. Though this churn does not seem to have impacted the company’s performance adversely, it is a cause of concern. While we would have certainly loved more certainty at the helm, we are reminded of a famous quote by Peter Lynch which Buffett seconds – "invest in businesses any idiot could run because someday one will.”The new CEO is an old-timer at Abbott Group and hopefully will have a longer stable stint and provide the much needed growth impetus.

Exhibit 16: Top management changes

Source: Ambit Asset Management, Company

Fixed Income - The place to be!

Whilst the environment seems to be conducive to growth, there has been a series of policy-tightening measures taken by central banks globally to keep inflation in check. Seeing fixed income revert to its traditional role in portfolio diversification would be welcome after two years in which aggressive Fed policy created a challenging path for bond investors.

There have been significant changes brewing for the Indian fixed income markets witnessing momentous long-awaited positive changes playing out. One example is the inclusion of Indian Bonds in the MSCI Bond Index and other indices that will follow the latest positive of the upgrade of India’s sovereign rating by S&P to “Positive”. Furthermore, with the wealth effect playing out and corporate treasuries from medium to small turning cash surplus, and Ultra HNW having generated great wealth, the time is now ripe for investors to look at managed debt portfolios.

Global debt markets and more so the Indian debt market tend to be more difficult to navigate and need a Fund/Portfolio Manager given the heterogeneous nature of instruments and complexities of the asset class.

From an Asset Manager perspective, too, our commitment at Ambit Asset Management has always been to augment our offering to fulfill overall financial and asset allocation requirements. With this viewpoint, we are happy to bring to you the debt (Fixed Income) side - Ambit Debt Edge Portfolio, with the endeavor to deliver a 3% to 6% return over the rate of inflation without risking safety.

AMBIT COFFEE CAN PORTFOLIO

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has an unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced with disruptions at regular intervals. As the industry evolves or is faced with disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

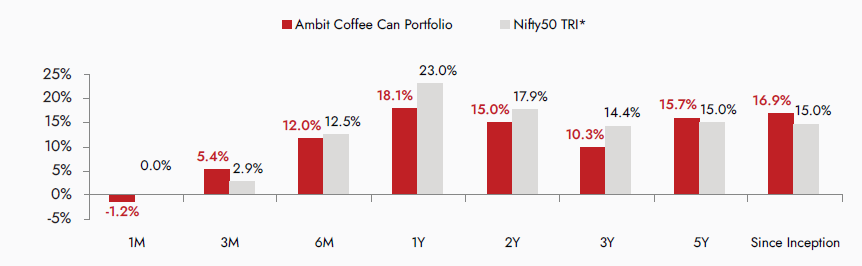

Exhibit 17: Ambit’s Coffee Can Portfolio point to point performance

Source: ##Ambit Coffee Can Portfolio inception date is Mar 6, 2017. **1M Return: 1st-31st May 24; 3M Return: 1st Mar'24 – 31st May 24; 6M Return: 1st Dec'23 – 31st May 24; 1Y

Return: 1st Jun'23 – 31st May 24. #Returns are net of all fees and expenses; Returns above 1yr are annualized

*Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio and the same is reported to SEBI.

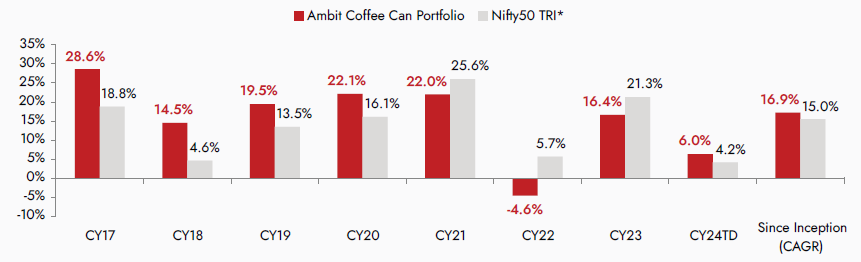

Exhibit 18: Ambit’s Coffee Can Portfolio calendar year performance

Source: ##Ambit Coffee Can Portfolio inception date is Mar 6, 2017. #Returns are net of all fees and expenses; Returns above 1yr are annualized

*Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio same is reported to SEBI.

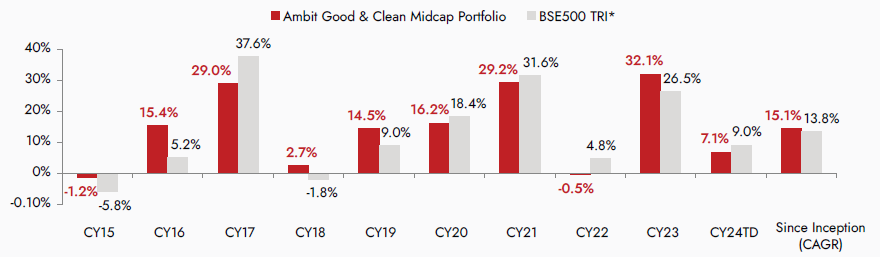

AMBIT GOOD & CLEAN MIDCAP PORTFOLIO

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver superior risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

- Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

- Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longer with annual churn not exceeding 15-20% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with these compounding earnings acting as the primary driver of investment returns over long periods.

- Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

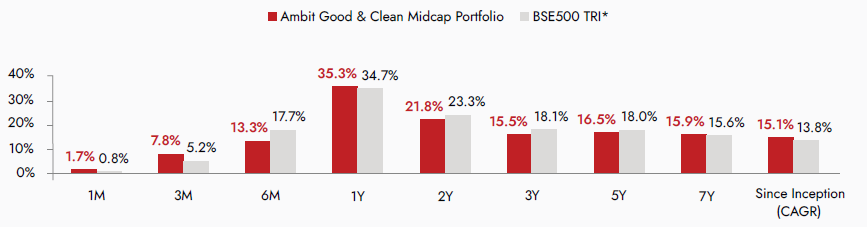

Exhibit 19: Ambit’s Good Clean Midcap Portfolio point to point performance

Source: ##Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015. **1M Return: 1st-31st May 24; 3M Return: 1st Mar'24 – 31st May 24; 6M Return: 1st Dec'23 –

31st May 24; 1Y Return: 1st Jun'23 – 31st May 24. #Returns are net of all fees and expenses; Returns above 1yr are annualized

*BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Mid cap Portfolio and the same is reported to SEBI.

Exhibit 20: Ambit’s Good Clean Midcap Portfolio calendar year performance

Source: ##Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015. #Returns are net of all fees and expenses; Returns above 1yr are annualized

*BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Mid cap Portfolio and the same is reported to SEBI.

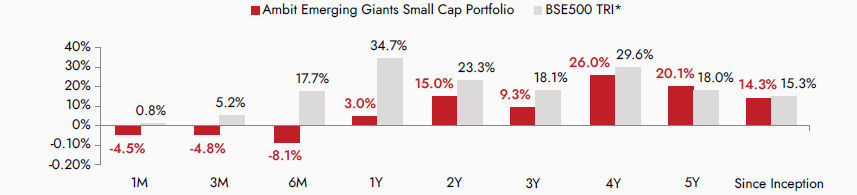

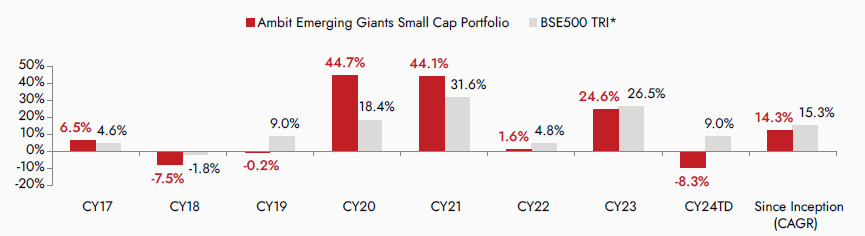

AMBIT EMERGING GIANTS SMALL CAP PORTFOLIO

Small caps with secular growth, superior return ratios and no leverage – Ambit's Emerging Giants portfolio aims to invest in small-cap companies with market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than Rs4,000cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt), and the ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence led us to a concentrated portfolio of 15-16 emerging giants.

Exhibit 21: Ambit Emerging Giants Small Cap Portfolio point to point performance

Source: ##Ambit Emerging Giants inception date is Dec 1, 2017. **1M Return: 1st-31st May 24; 3M Return: 1st Mar'24 – 31st May 24; 6M Return: 1st Dec'23 – 31st May 24; 1Y

Return: 1st Jun'23 – 31st May 24. #Returns are net of all fees and expenses; Returns above 1yr are annualized

*BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants Portfolio and the same is reported to SEBI.

Exhibit 22: Ambit Emerging Giants Small Cap Portfolio calendar year performance

Source: ##Ambit Emerging Giants Small cap Portfolio inception date is Dec 1, 2017. #Returns are net of all fees and expenses; Returns above 1yr annualized

*BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants Small Cap Portfolio and the same is reported to SEBI.

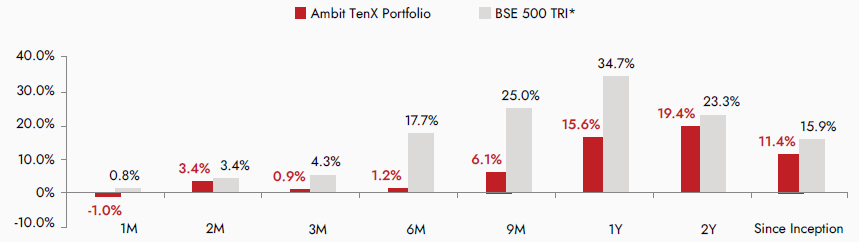

AMBIT TenX PORTFOLIO

Ambit TenX Portfolio gives investors an opportunity to participate in the India growth story as the Indian GDP heads towards a US$10tn mark over the next 12-15 years. Mid and Small corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that can grow their earnings 10x over the same period implying 18-21% CAGR. Key features of this portfolio would be as follows:

- Longer-term approach with a concentrated portfolio: Ideal investment duration of >5 years with 15-20 stock.

- Key driving factors: Low penetration, strong leadership, light balance sheet

- Forward-looking approach: Relying less on historical performance and more on future potential while not deviating away from the Good & Clean philosophy.

- No Key-man risk: Process is the Fund Manager

Exhibit 23: Ambit TenX Portfolio point to point performance

Source: ##Ambit TenX Portfolio inception date is Dec 13, 2021. **1M Return: 1st-31st May 24; 3M Return: 1st Mar'24 – 31st May 24; 6M Return: 1st Dec'23 – 31st May 24; 1Y Return:

1st Jun'23 – 31st May 24. #Returns are net of all fees and expenses; Returns above 1yr are annualized

*BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio and the same is reported to SEBI.

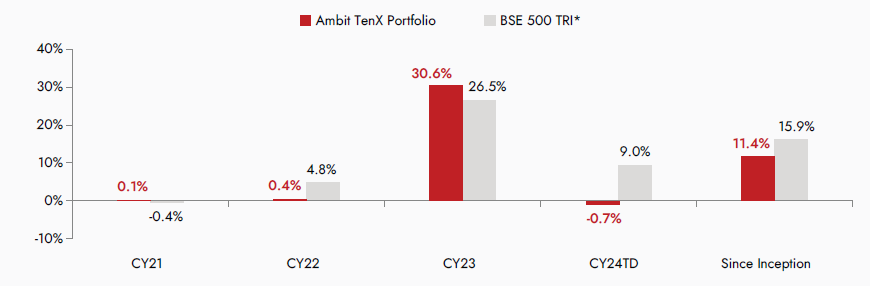

Exhibit 24: Ambit TenX Portfolio calendar year performance

Source: ##Ambit TenX Portfolio inception date is Dec 13, 2021. #Returns are net of all fees and expenses; Returns above 1yr are annualized

*BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio and the same is reported to SEBI.