As a result, the forward one-year PE across stocks got re-rated from 10x in 2013 to 20x in 2017, reaching a peak of 46x.

However, the sector has seen a significant de-rating in the last couple years led by (a) channel destocking by global players, (b) rising feedstock prices alongside dwindling pricing power due to the destocking, and (c) rising freight costs due to global supply chain imbalances. As a result, the sector valuation multiple has seen a de-rating to 39x the forward one-year PE (an 18% decline to peak multiples) for chemical stocks. Note that the forward PE is on depressed earnings as well.

Our interaction with a few companies and channel partners suggests that the chemical sector is on the cusp of a turnaround led by an improving pricing environment. If this sustains, we may see a repeat of the strong double-digit growth recorded by the companies in FY17-22. Several companies are trading at attractive multiples based on valuations. Few of our portfolio companies like Rossari / PI / Alkyl Amines, among others, are trading at forward FCF yields of more than 2% - 3%.

A few of the drivers leading to improved pricing include (a) low channel inventory, (b) significant deflation in raw material prices, implying better spreads from 2HFY25 onwards, and (c) early signs of a pick-up in global demand.

FY17-22 – Dream run for Indian chemical companies

Undoubtedly, FY17-22 was a golden period for chemical companies characterized by record EBITDA margins, strong revenue growth and robust cash flow generation. Several companies across sub-sectors like agrochemicals, specialty chemicals, amines, and glass lined reactors saw strong performance. For instance, companies like SRF, PI in agrochemicals; Aarti, Deepak Nitrite, Navin Fluorine and Vinati Organics in intermediates and specialty chemicals; Alkyl and Balaji in amines reported average and median 5-year earnings at a CAGR of 31% and 29%, respectively, during this period.

We believe there were four main drivers for this strong performance:

Favorable demand situation:

- Indian companies benefitted materially during the period on account of favorable demand, both in India and abroad, with exports opening up.

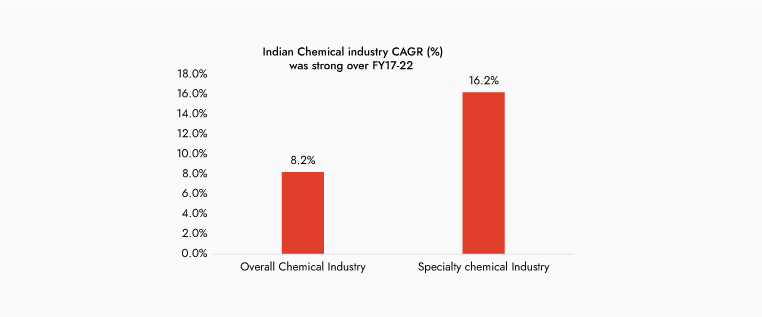

- The Indian chemical Industry grew from Rs 910bn to Rs 1,350bn during FY17-22.

- Specialty chemicals fared materially better than commodities, growing at 2x the size of the total market.

- Both domestic and external demand was fairly robust led by import substitution, outsourcing and the China plus one (C+1) theme.

Exhibit 1: Specialty chemical grew 2x than overall chemical industry during FY17-22

Source: Ambit Asset Management, Company, Crisil

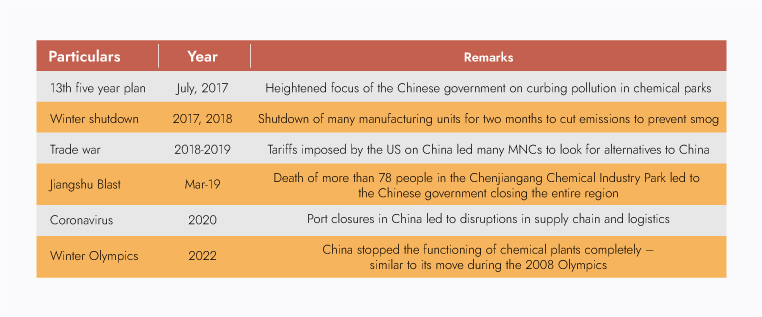

Supply chain challenges in China:

Between 2017 and 2022, Chinese chemical companies faced multiple disruptions as highlighted below. As a result, the world recognized that an alternative to China is the need for the hour.

Exhibit 2: Series of events in China

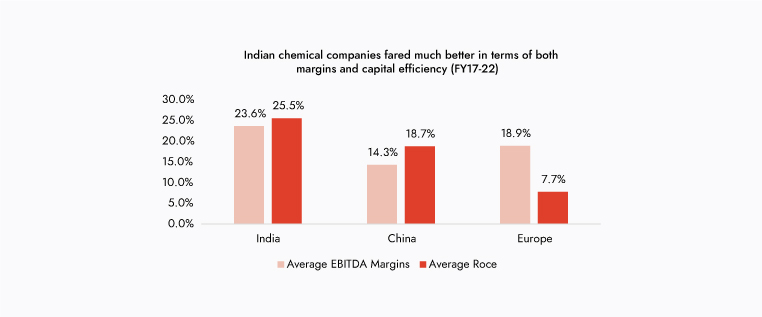

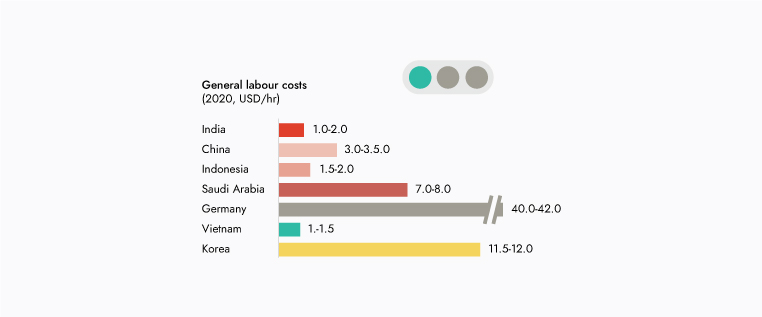

India’s rising competitiveness vs global players:

- Indian chemical companies’ performance was materially favourable compared to their Chinese and European peers on key matrices owing to a focus on capital efficiency, lower labour costs and strong engineering capabilities.

- Indian chemical companies reported higher EBITDA margins of ~23.6% over FY17-22 v/s ~14.3% by Chinese and ~18.7% by European companies.

- ROCE for India companies was at ~25.5% over FY17-22 v/s 18.7% for Chinese and 7.7% for European companies.

- Consequently, India emerged as among the strongest regions both in terms of cost competitiveness and capital efficiency, effectively positioning it among the only reliable alternatives to China while garnering it market share from Europe.

Exhibit 3: India outplays global peers during FY17-22

Source: Ambit Asset Management, Company

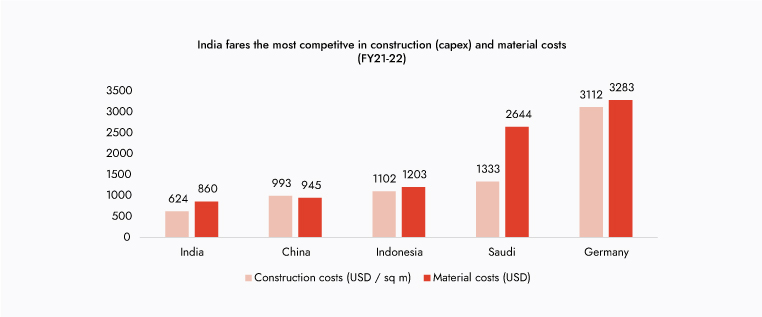

- Indian chemical companies’ industry leading ROCE and EBITDA are not only a function of a cyclical uptick but a structural one. India is better placed in terms of both capex (construction costs) and opex (material costs and labour costs) positioning it to take advantage of the global chemical tailwinds.

Exhibit 4: Construction and material cost across geographies

Source: Ambit Asset Management, company, Mckinsey

Exhibit 5: Labour costs in India are amongst the lowest of major chemical producing countries

Source: Ambit Asset Management, Company, McKenzie

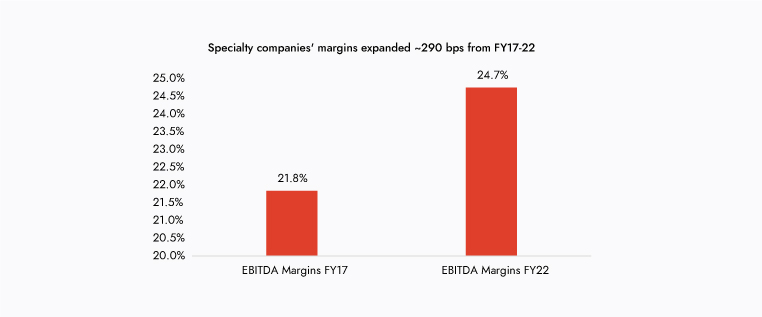

Operating margins are driven by forward and backward integration

- Specialty chemical companies’ operating margins expanded by 290bps over FY17-22 led by forward and backward integration, a foray into higher value-added products and operating efficiencies.

- Companies such as Aarti and Atul benefitted due to low-cost manufacturing and backward integration across key products.

- Companies such as PI and SRF had a higher share of value-added products such as Pyroxasulfone and DFMPA.

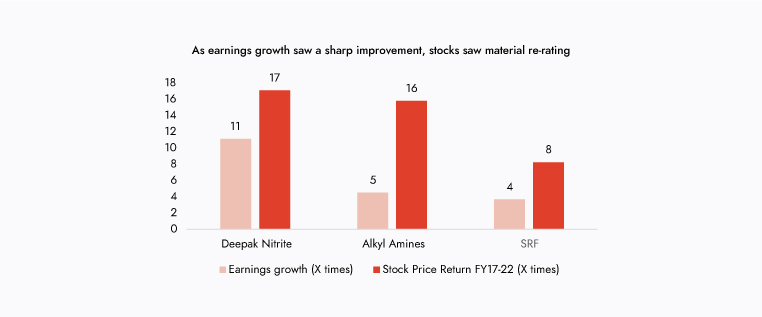

- Consequently, stock prices for chemical companies saw a significant PE re-rating during this period of high earnings growth, leading to much higher stock price returns relative to earnings growth.

Exhibit 6 : Chemical companies demonstrated margin expansion

Source: Ambit Asset Managent , Company

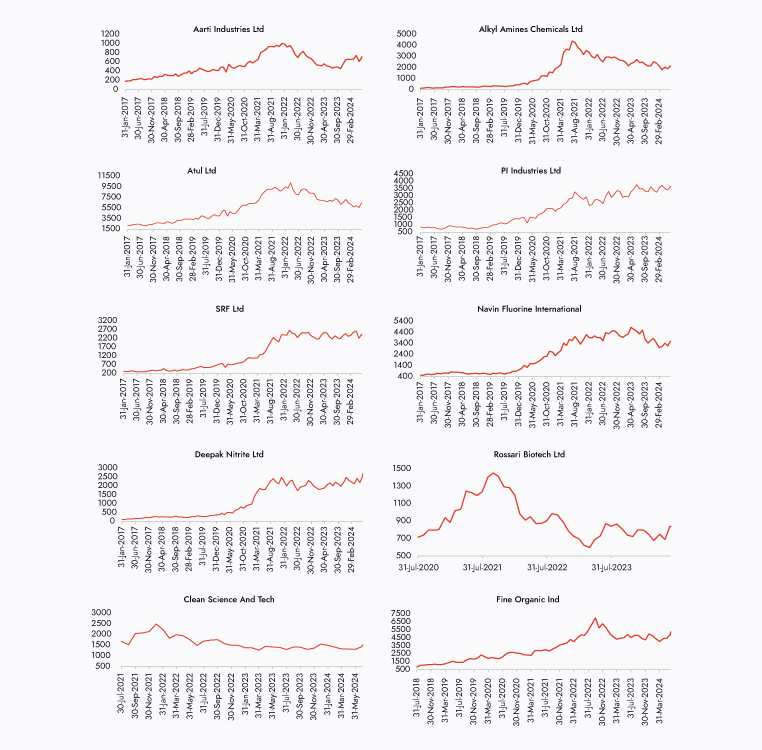

Exhibit 7: Leading to multi-fold growth in sharp earnings and stock price growth

Source: Ambit Asset Management, Company

Post-Covid distress for the sector

Post covid, the chemical sector has seen a significant de-rating, with the valuation multiple correcting by ~18% to 39x the forward one-year PE as compared to the bull period multiple of 46x.

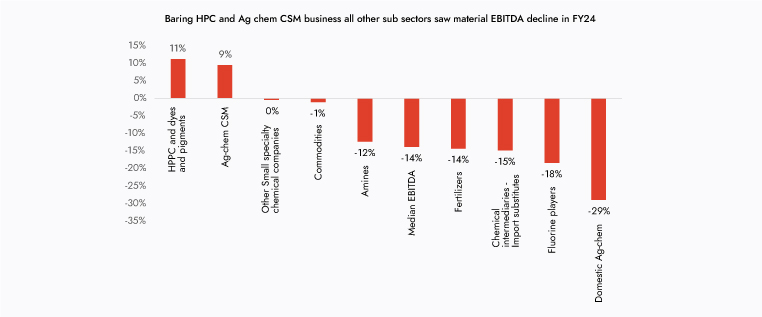

One of the key reasons for the sharp correction has been the significant correction in EBITDA margins and ROCE during this period which caused analysts to cut their estimates across companies. These, coupled with higher depreciation and interest costs, resulted in profits declining on a YoY basis.

Exhibit 8: Majority of segments witnessed a sharp decline

Source: Ambit Asset Management, Company

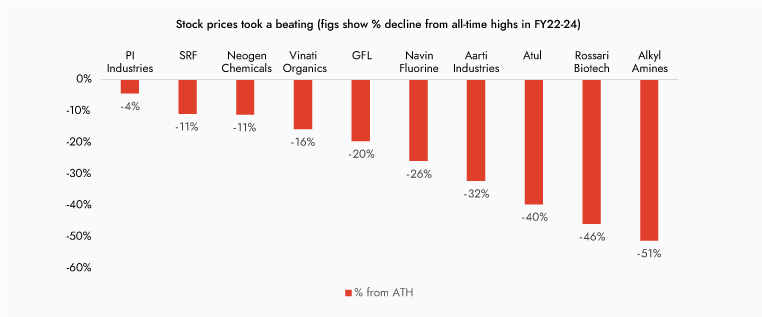

Exhibit 9: Due to drop in profits, we saw correction in stock prices from ATH

Source: Ambit Asset Management, Company

We believe there were three main drivers for this weak performance:

Agro-chemical destocking:

- During Covid, distributors stocked up on inventory given the supply chain challenges.

- Rising interest costs during this period caused inventory finance costs to go up. There was, therefore, no option but to correct inventory, leading to a ~17% decline in volumes.

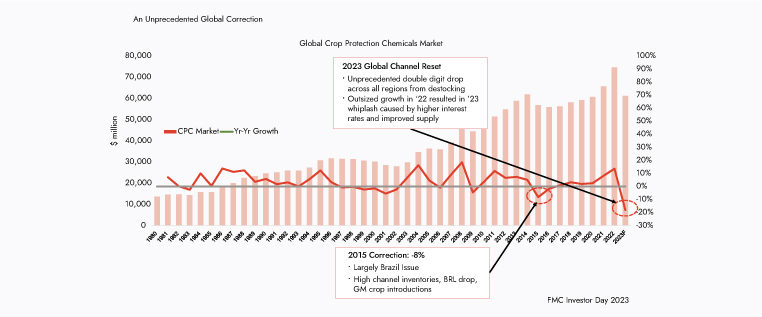

Exhibit 10: Global ag-chem saw the sharpest correction in 2023 in the last 40 years due to destocking

Source: Agbioinvestor FMC

Rising feedstock prices alongside dwindling pricing power given destocking:

- Due to post-covid supply-led challenges, the pricing of key RMs shot up materially, causing the operating margins of chemical companies to be hit.

- Logistics costs also shot up during this period due to rising freight costs owing to the Russia-Ukraine war.

- Passing on rising raw material costs was not possible due to weak global demand in Europe.

Exhibit 11 : Consequently, Chemical margins declined 510 bps from FY22-24

Source: Ambit Asset Management, Company

Domestic industry slowdown:

The domestic user industry also went through a consolidation in this period due to pent up demand during the pandemic – especially for pharma companies. Even the agriculture sector saw margin pressures and sluggish demand led by two years of weak rainfall due to EL-Nino. As a result, stock prices saw a significant correction.

Exhibit 12: Stock prices have corrected from their peak

Source: Ambit Asset Management, Bloomberg

We believe time is ripe for a re-look at the chemical sector

Our interaction with a few companies and channel partners suggests that the chemical sector is on the cusp of a turnaround led by an improving pricing environment. If this sustains, we may see a repeat of the strong double-digit growth recorded by the companies in FY17-22. Several companies are trading at attractive multiples based on valuations; Rossari / PI / Alkyl Amines, among others, are trading at FCF yields of more than 2% - 3%.

A few of the drivers leading to improved pricing include (a) low channel inventory, (b) significant deflation in raw material prices, implying better spreads from 2HFY25 onwards, and (c) early signs of a pick-up in global demand.

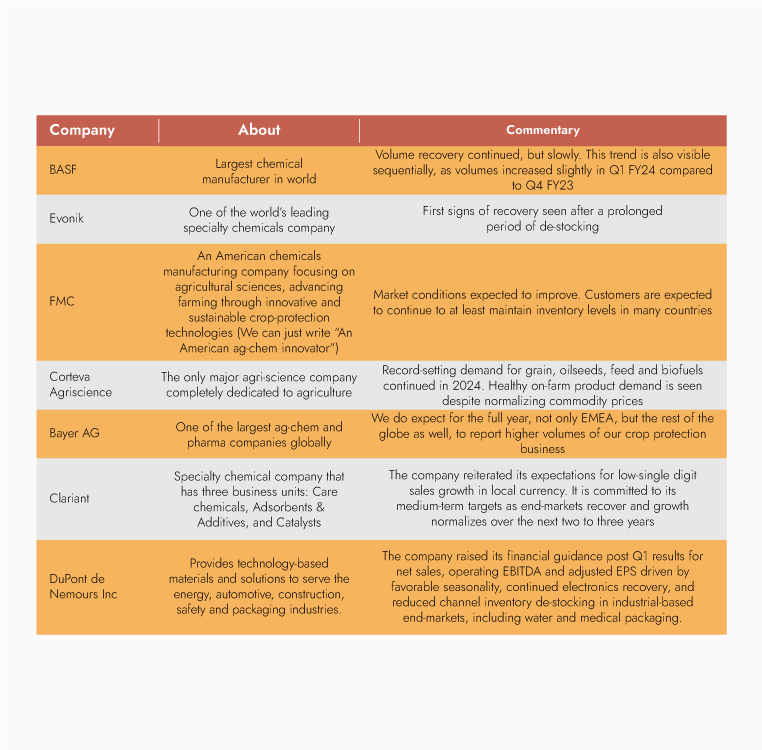

Visible green shoots:

The management commentaries of global companies show that they have started turning positive on the chemical sector across all sub-segments in general and Ag-chem, Home and Personal Care in particular

Resurgence in domestic agrochemical demand led by better monsoon; good sowing this year:

- After a difficult couple of years, the Indian Meteorological Department predicts above-average rainfall in 2024, estimated at 106% of the long-term average. The weakening El Nino is expected to transition to a neutral phase by the onset of the monsoon, while La Nina conditions may develop later. This bodes well for domestic ag-chem players and should result in the sector coming back strongly this year.

Improving spreads led by significant deflation in raw material prices and stable finished goods prices:

- We have seen spreads and prices inching up from lows and getting closer to historic levels in subsequent months, signifying a return to normalcy.

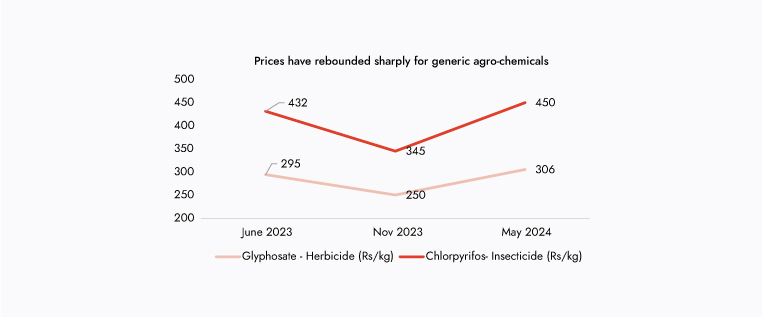

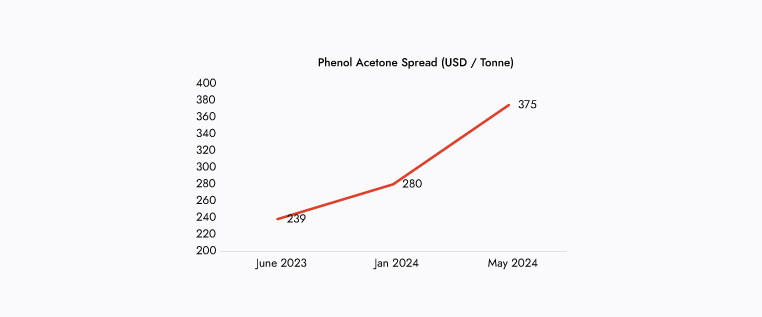

- Phenol – Acetone spreads have inched up over the past few months, though they are still below historic lows. Generic ag-chem pricing has seen a sharp rebound.

Exhibit 13: Prices have rebounded sharply for generic agro-chemicals

Source: Ambit Asset Management, Company

Exhibit 14: Similarly spreads for Phenol Acetone have seen uptick

Source: Ambit Asset Management, Company

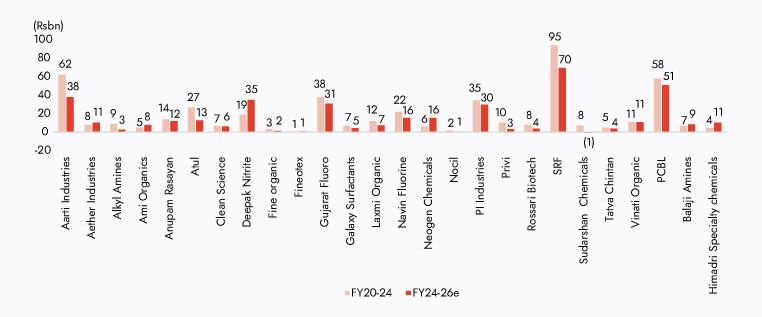

Gross block addition has not been utilised:

- Robust capex over FY20-24, coupled with low demand, has led to low utilization for most companies – which means capex over the next four years is likely to remain mute

Exhibit 15: Capex intensity to reduce

Source: Ambit Asset Management, Company

- With ample capacities already in place, future capex as a percentage of OCF will come down materially as operating profits shoot up due to better demand, better pricing, and the play out of operating leverage. This triple engine will result in exponential growth across the sector.

We have increased weightage for the chemical sector across portfolios

We have increased weightage for the chemical sector across schemes. The new names we have added to our portfolio in the last six months include Rossari Biotech and Alkyl Amines.

Conclusion:

- We believe Indian chemicals and particularly sub-segments i.e. - Ag chem contract manufacturing, import substitution, and HPC are poised for a structural recovery, and our portfolio is well placed to take advantage of the same.

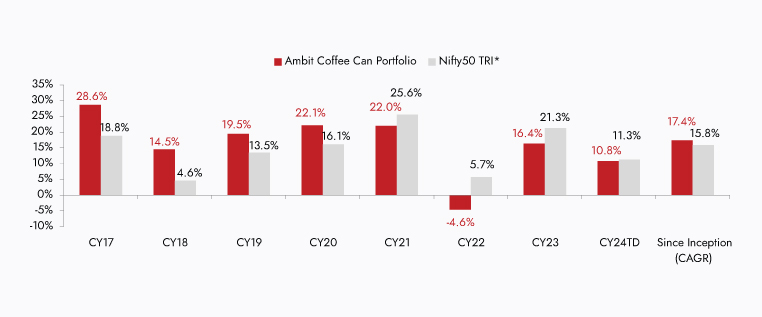

AMBIT COFFEE CAN PORTFOLIO

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has an unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced with disruptions at regular intervals. As the industry evolves or is faced with disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

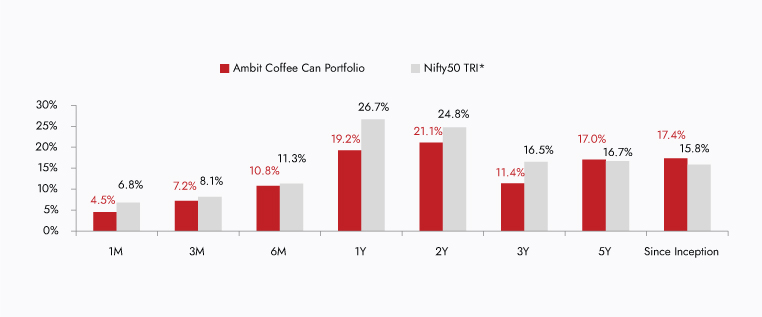

Exhibit 16: Ambit Coffee Can Portfolio point-to-point performance

Source: ##Ambit Coffee Can Portfolio inception date is Mar 6, 2017. **1M Return: 1st-30th Jun 24; 3M Return: 1st Apr'24 – 30th Jun 24; 6M Return: 1st Jan'24 – 30th Jun 24; 1Y Return: 1st Jul'23 – 30th Jun 24. #Returns are net of all fees and expenses; Returns above 1yr are annualized.*Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio and the same is reported to SEBI.

Exhibit 17: Ambit Coffee Can Portfolio calendar year performance

Source: ##Ambit Coffee Can Portfolio inception date is Mar 6, 2017. #Returns are net of all fees and expenses; Returns above 1yr are annualized.*Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio same is reported to SEBI.

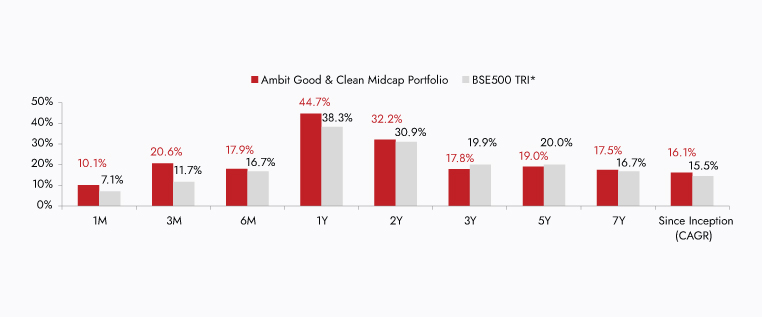

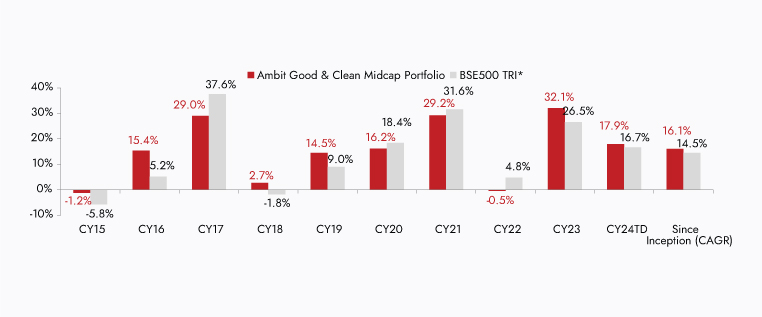

AMBIT GOOD & CLEAN MIDCAP PORTFOLIO

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver superior risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

Exhibit 18: Ambit Good & Clean Midcap Portfolio point-to-point performance

Source: ##Ambit Good & Clean Mid cap Portfolio inception date is Mar 6, 2017. **1M Return: 1st-30th Jun 24; 3M Return: 1st Apr'24 – 30th Jun 24; 6M Return: 1st Jan'24 – 30th Jun 24; 1Y, Return: 1st Jul'23 – 30th Jun 24. #Returns are net of all fees and expenses; Returns above 1yr are annualiz*BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Mid cap Portfolio and the same is reported to SEBI.

Exhibit 19: Ambit Good & Clean Midcap Portfolio calendar year performance

Source: ##Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015. #Returns are net of all fees and expenses; Returns above 1yr are annualized. *BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Mid cap Portfolio and the same is reported to SEBI.

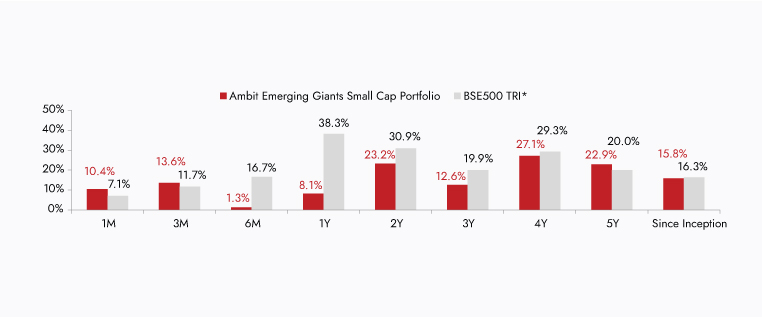

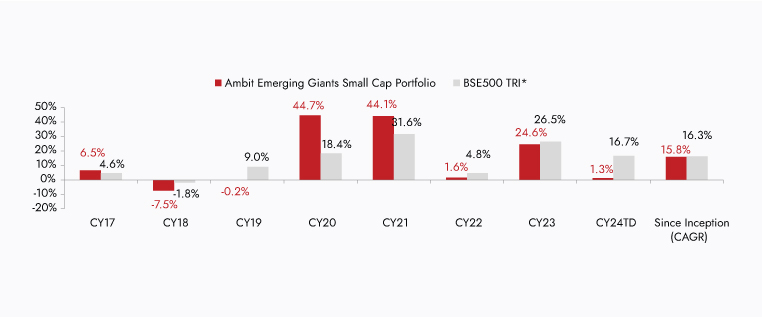

AMBIT EMERGING GIANTS SMALL CAP PORTFOLIO

Small caps with secular growth, superior return ratios and no leverage – Ambit's Emerging Giants portfolio aims to invest in small-cap companies with market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than INR 4,000cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt), and the ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence led us to a concentrated portfolio of 15-16 emerging giants.

Exhibit 20: Ambit Emerging Giants Small Cap Portfolio point-to-point performance

Source: ##Ambit Emerging Giants Small cap Portfolio inception date is Dec 1, 2017. *1M Return: 1st-30th Jun 24; 3M Return: 1st Apr'24 – 30th Jun 24; 6M Return: 1st Jan'24 – 30th Jun 24; 1Y, Return: 1st Jul'23 – 30th Jun 24. #Returns are net of all fees and expenses; Returns above 1yr are annualized*BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Mid cap Portfolio and the same is reported to SEBI.

Exhibit 21: Ambit Emerging Giants Small Cap Portfolio calendar year performance

Source: ##Ambit Emerging Giants Small cap Portfolio inception date is Dec 1, 2017. #Returns are net of all fees and expenses; Returns above 1yr annualized. *BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants Small Cap Portfolio and the same is reported to SEBI.

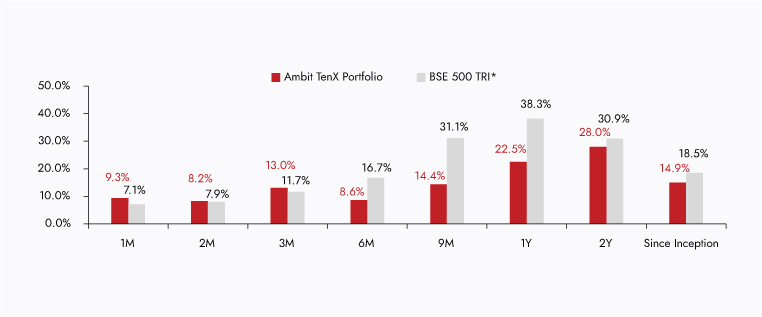

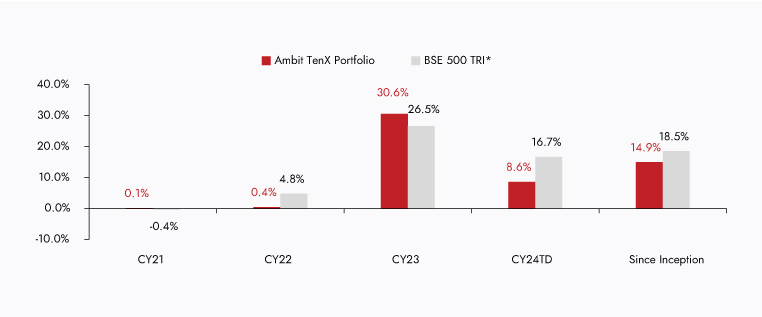

AMBIT TenX PORTFOLIO

Ambit TenX Portfolio gives investors an opportunity to participate in the India growth story as the Indian GDP heads towards a US$10tn mark over the next 12-15 years. Mid and Small corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that can grow their earnings 10x over the same period implying 18-21% CAGR. Key features of this portfolio would be as follows:

Exhibit 22: Ambit TenX Portfolio point-to-point performance

Source: ##Ambit TenX Portfolio inception date is Mar 6, 2017. *1M Return: 1st-30th Jun 24; 3M Return: 1st Apr'24 – 30th Jun 24; 6M Return: 1st Jan'24 – 30th Jun 24; 1Y, Return: 1st Jul'23 – 30th Jun 24. #Returns are net of all fees and expenses; Returns above 1yr are annualized*BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio and the same is reported to SEBI.

Exhibit 23: Ambit TenX Portfolio calendar year performance

Source: ##Ambit TenX Portfolio inception date is Dec 13, 2021. #Returns are net of all fees and expenses; Returns above 1yr are annualized. *BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio and the same is reported to SEBI.