.jpg)

Typically, CAPEX generates a positive feedback loop: government investments spur private sector activity, encouraging businesses to undertake their own capital projects. This collective momentum fosters structural improvements in the economy, paving the way for sustainable long-term growth and enhanced efficiency. Such a vigorous commitment to CAPEX signals a strong, forward-looking economy dedicated to fostering prosperity and continued advancement.

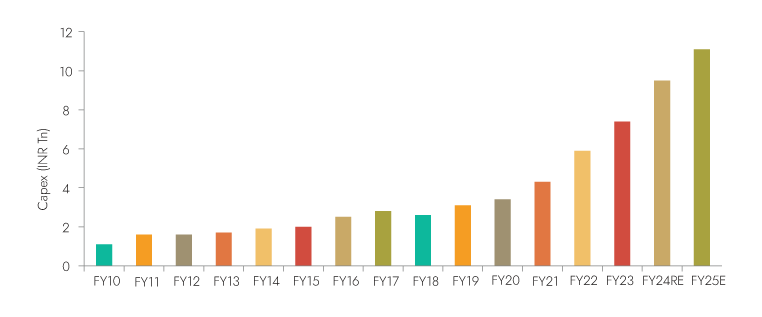

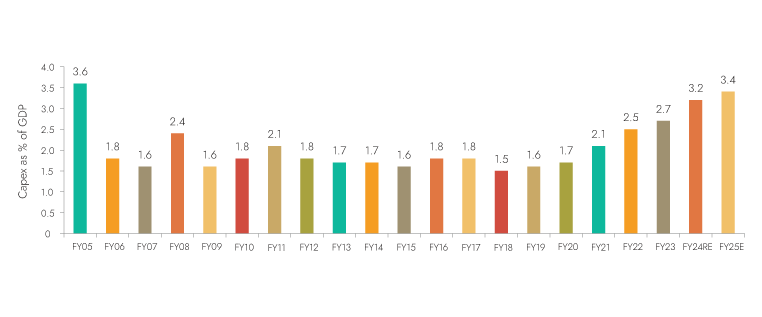

Since the onset of the COVID-19 pandemic, the Indian government has significantly ramped up its capital expenditure. From FY21 onwards, CAPEX spending surged from 4.3 trillion INR to 11.1 trillion INR in FY25BE. In contrast, between FY15 and FY20, CAPEX grew at a more modest pace, rising from 2.0 trillion INR to 3.4 trillion INR by FY20. This sharp increase underscores a strategic shift towards heightened investment in infrastructure and development post-pandemic. As a result, CAPEX as a percentage of GDP went up to 3.4% in FY25BE from 2.1% in FY21.

In fact, such a high figure was last witnessed in FY05.

Exhibit 1: Sharp increases in capex spends

Source: Ambit Asset Management

Exhibit 2: …translates to a sharply increasing govt capex as % of GDP from 2.1% to 3.4% in FY25BE

Source: Ambit Asset Management

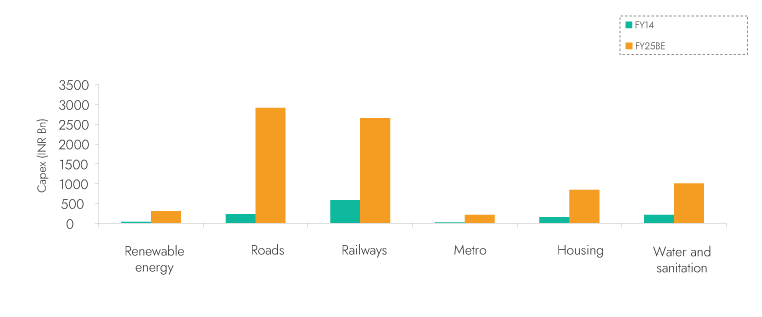

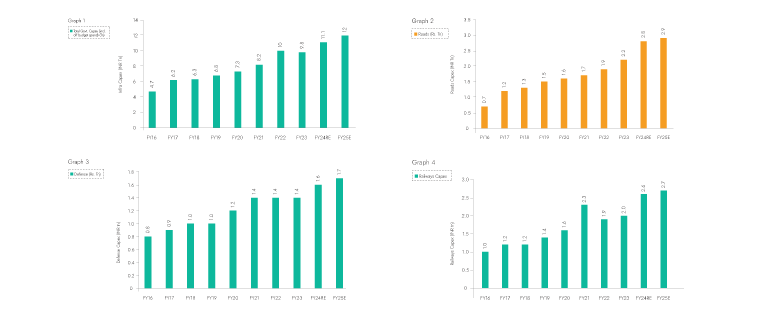

Exhibit 3: There has been a strong CAPEX push in sectors like roads and railways since FY14

Source: Ambit Asset Management

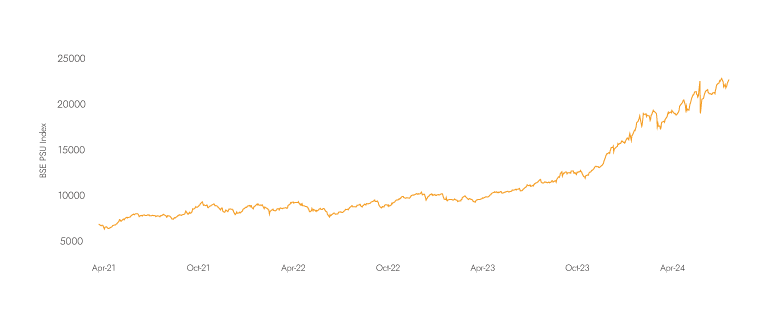

Exhibit 4: Sharp CAPEX has been complemented by a run-up in PSU stocks since FY21

Source: Ambit Asset Management

Is the CAPEX story fading out?

While CAPEX has been robust in the aftermath of COVID-19, recent indicators suggest that these spending levels may be approaching their peak. For FY25BE, total infrastructure expenditure is projected to increase by 8.1%, marking a notable deceleration from the 13% growth recorded in FY24RE. Additionally, CAPEX allocations across various sectors have grown at a rate below the nominal growth of the Indian economy, reflecting a potential reduction in sector-specific investments. Although part of this slowdown can be attributed to base effects, the overall deceleration in growth rates suggests a shift towards more measured investment strategies moving forward.

Exhibit 5: Capex across key segments has been moderating in FY25

Source: Ambit Asset Management

Fiscal consolidation stands out as a central theme in the government’s latest budget. This is reflected in the restrained allocation to capex, especially when compared to the interim budget. The recent revenue infusion from the RBI has been strategically directed to reduce the fiscal deficit from 5.1% to 4.9% of GDP.

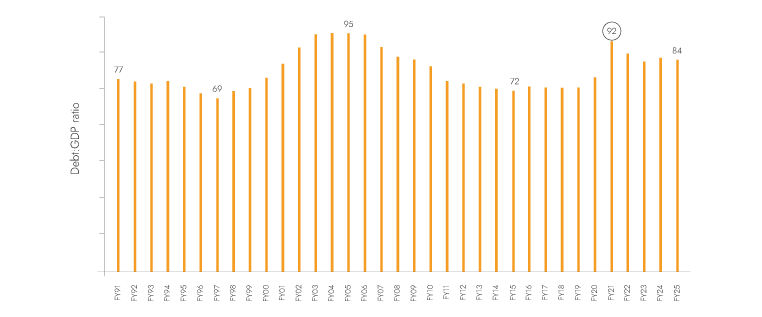

Additionally, while the government has managed to decrease the debt-to-GDP ratio from 91% in FY21 to 85% in FY24, it remains above the targeted 80%. This emphasis on fiscal consolidation underscores the government’s commitment to enhancing economic stability and managing public debt more effectively.

Exhibit 6: India’s debt: GDP ratio currently stands at 84% in FY25

Source: Ambit Asset Management

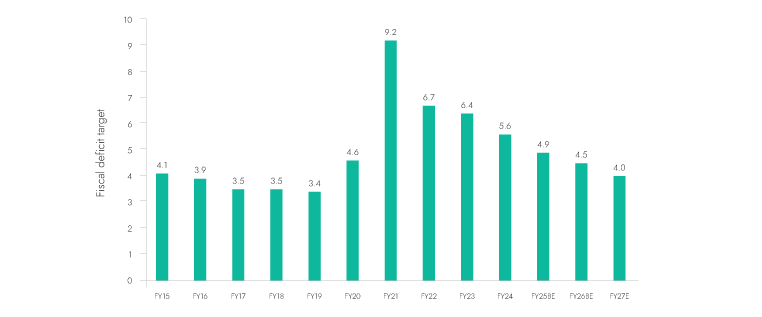

Exhibit 7: India’s fiscal deficit target has reduced from 9.2% in FY21 to 4% in FY27E

Source: Ambit Asset Management

Is Consumption the New Focus Point of the Government?

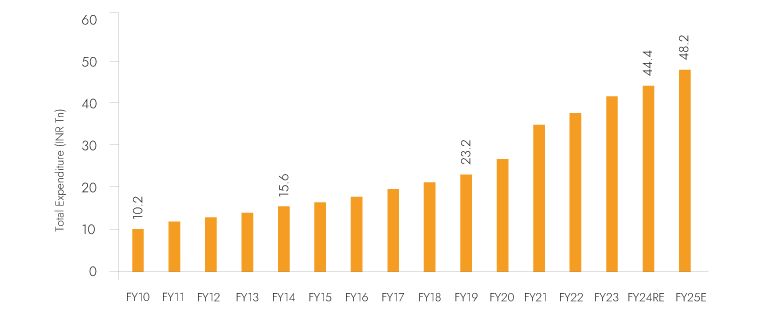

Exhibit 8: Total government expenditure increased from INR 44.4 tn in FY24RE to INR 48.2 tn in FY25E

Source: Ambit Asset Management

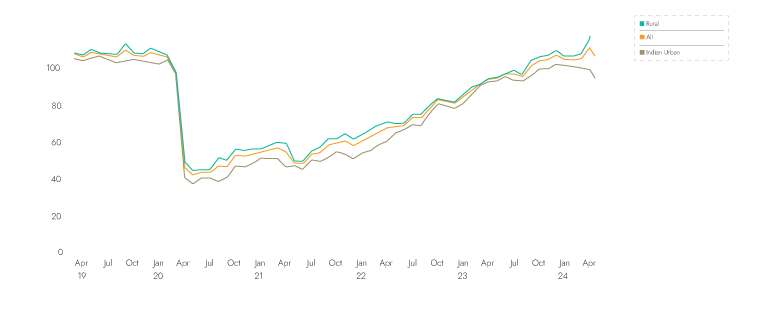

Exhibit 8 raises a crucial question: With the decline in spending on traditionally large segments such as CAPEX, where is this additional funding being allocated? Our analysis indicates that a portion of this surplus may be directed towards the government's consumption-related expenditures. The consumer sentiment index, which monitors sentiments nationwide encompassing both urban and rural areas, is also showing strong recoveries and has reached its pre-COVID level.

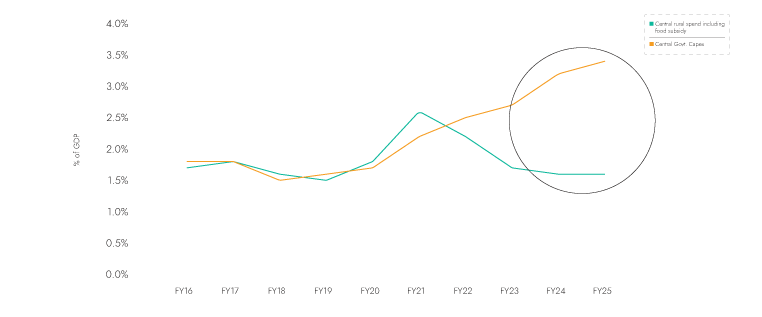

Over the past five years, government spending on rural and agricultural sectors has remained relatively stable at approximately INR 3.9 trillion, while CAPEX has surged from INR 3.6 trillion to INR 8.8 trillion. This shift has created a significant divergence between government CAPEX and rural spending. In FY21, rural expenditure was 400 basis points higher than CAPEX. By FY24, however, CAPEX spending had surpassed rural expenditure by 1600 basis points, highlighting a dramatic realignment in budget priorities.

Exhibit 9: CAPEX spending has far exceeded rural spending since FY21

Source: Ambit Asset Management

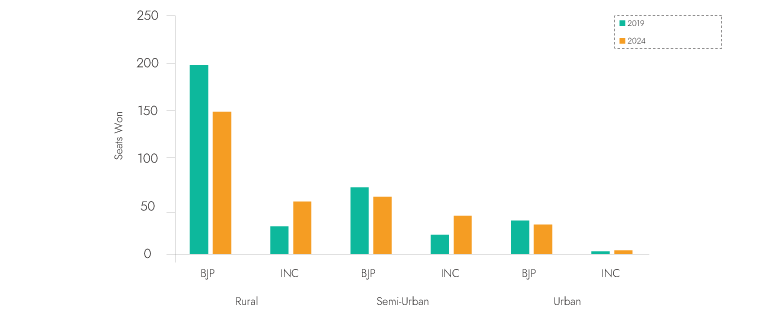

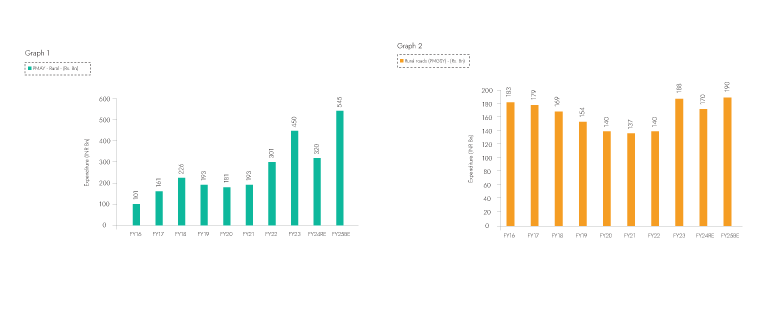

However, we now see a trend reversal whereby government is now trying to step up the focus on rural spending as reflected by s sharp increase in PMAY and rural road expenditure. We believe this is on the back of poor performance by the BJP in the recently concluded general elections in India’s hinterland.

Exhibit 10: BJP lost several votes across rural areas in the recently concluded general elections

Source: Ambit Asset Management

Exhibit 11: Sharp increases in segments like PMAY and rural roads are indicative of a reversing expenditure trend

Source: Ambit Asset Management

Exhibit 12: Consumer sentiment index indicates recovery in rural and urban segments

Source: CMIE, Ambit Asset Management

The Return of Quality

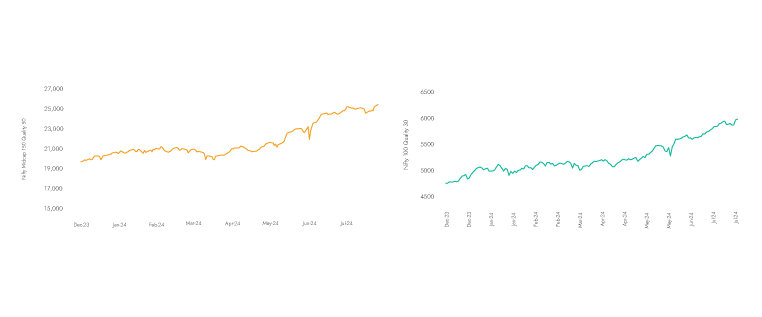

Since the election poll results were announced on 3rd June, quality indices have experienced a notable rebound in performance. Prior to the elections, these indices had shown relatively lacklustre results, overshadowed by a broad-based market rally. However, since the election outcome, indices such as the Nifty 100 Quality 30 and Nifty Midcap 150 Quality 50 have risen by 10.0% and 9.6% respectively. In contrast, over the six months# leading up to the elections, these indices had increased by 12.7% and 15.0%.

Conversely, the BSE PSU index had weak post-election performance of 0.7%. This can be compared with the strong 6-month performance of the index before the elections – which was 47%. This suggests that the PSU index has not benefitted from the election results – unlike the quality indices.

Exhibit 13: BSE PSU Index has risen 60% since Dec ‘23

Source: Ace Equity, Ambit Asset Management

Exhibit 14: Performance of Nifty Midcap 150 Quality 50 & Nifty 100 Quality 30

Source: Ace Equity, Ambit Asset Management

What does this mean for Ambit PMS funds?

Since the election results, Ambit’s long-only schemes have exhibited impressive performance, markedly outperforming our results from the preceding six months. Ambit’s 'Good and Clean Framework'—which focuses on investing in companies with strong capital allocation and transparent accounting practices—has been particularly effective. This proprietary framework is designed to provide robust downside protection during challenging economic environments and to capitalize on strong returns when quality stocks are in demand. In the current market, where quality stocks are experiencing a resurgence, Ambit’s disciplined approach has delivered significant gains, underscoring the effectiveness of our investment strategy.

In our February 2024 newsletter, we identified both qualitative and quantitative indicators that pointed to a forthcoming recovery in the rural segment. This was despite a prevailing market focus on sectors experiencing broad-based rallies.

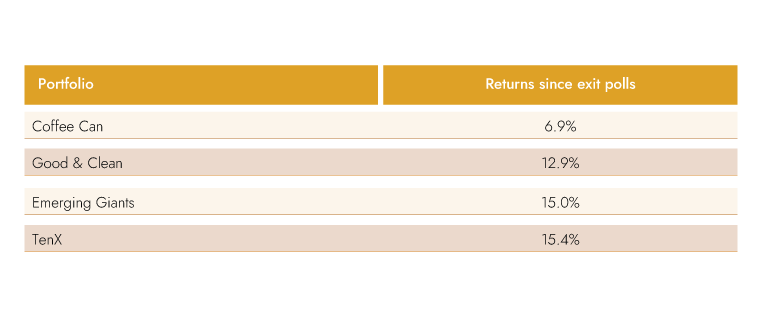

By analyzing company transcripts, macroeconomic trends, and industry market shares, we highlighted emerging themes such as mass apparel, mass retail, consumer durables, and mass footwear as areas poised for strong performance in the near future. Since then, the companies we spotlighted within these themes have demonstrated significant improvements, validating our earlier predictions and reflecting the robustness of the rural recovery we anticipated. Since exit polls until 31st July, FMCG Index has delivered 15% returns against BSE500 8%. Select consumer oriented businesses charted below have returned 30-45% during same period.

Exhibit 15: Strong performance of rural-oriented stocks since Feb ‘24

Source: Ace Equity, Ambit Asset Management

Conclusion:

The government's focus on shifting from capital expenditure (CAPEX) to consumption-oriented policies is set to significantly benefit businesses that thrive on consumer demand. This transition bodes well for consumption-oriented businesses, as it creates a favorable environment for growth, innovation, and customer engagement. We have picked companies such as Britannia, V-mart, Bector foods that have deep roots into the economy with proven execution.

With benefits of higher allocation taking effect, companies positioned to leverage increased consumer spending will likely see enhanced opportunities for expansion and profitability, driving a more resilient economy.

AMBIT COFFEE CAN PORTFOLIO

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has an unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced with disruptions at regular intervals. As the industry evolves or is faced with disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

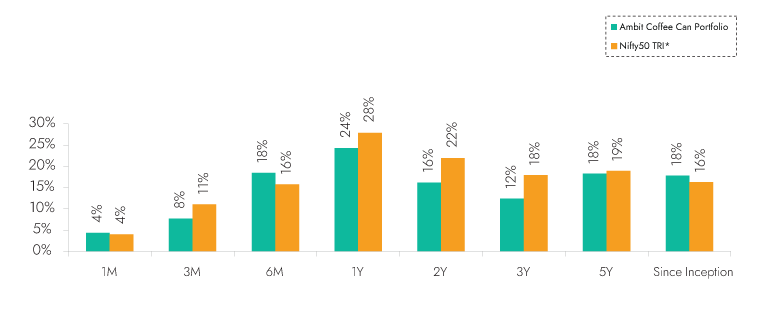

Exhibit 16: Ambit’s Coffee Can Portfolio point-to-point performance

Ambit Coffee Can Portfolio inception date is Mar 06, 2017;

**1M Return: 1st - 31st Jul'24; 3M Return: 1st May'24 – 31st Jul'24; 6M Return: 1st Feb'24 – 31st Jul'24; 1Y Return: 1st Aug'23 – 31st Jul'24 *Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The same is reported to SEBI. In addition to the same, we have included MSCI India for information purposes only. The same should not be relied upon for performance benchmarking in any manner.

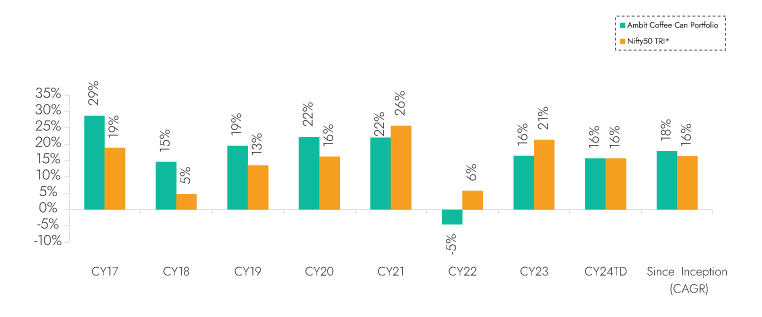

Exhibit 17: Ambit’s Coffee Can Portfolio calendar year performance

Ambit Coffee Can Portfolio inception date is Mar 06, 2017; *Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The same is reported to SEBI.

Ambit Good & Clean Midcap Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver superior risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

- Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

- Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longer with annual churn not exceeding 15-20% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with these compounding earnings acting as the primary driver of investment returns over long periods.

- Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

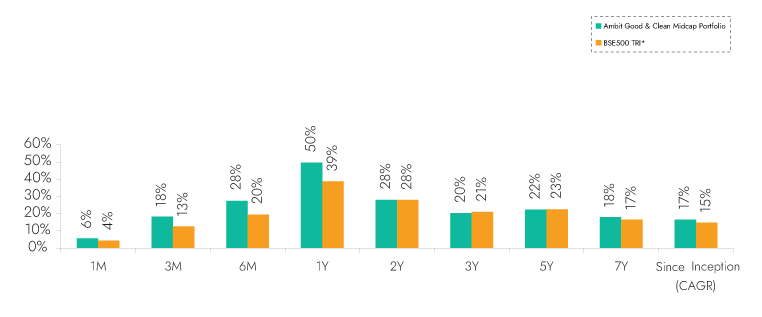

Exhibit 18: Ambit’s Good & Clean Midcap Portfolio point-to-point performance

Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015; **1M Return: 1st - 31st Jul'24; 3M Return: 1st May'24 – 31st Jul'24; 6M Return: 1st Feb'24 – 31st Jul'24; 1Y Return: 1st Aug'23 – 31st Jul'24 *BSE 500 50 TRI is the selected benchmark for the Ambit Good & Clean Mid cap. The same is reported to SEBI. In addition to the same, we have included MSCI Midcap for information purposes only. The same should not be relied upon for performance benchmarking in any manner.

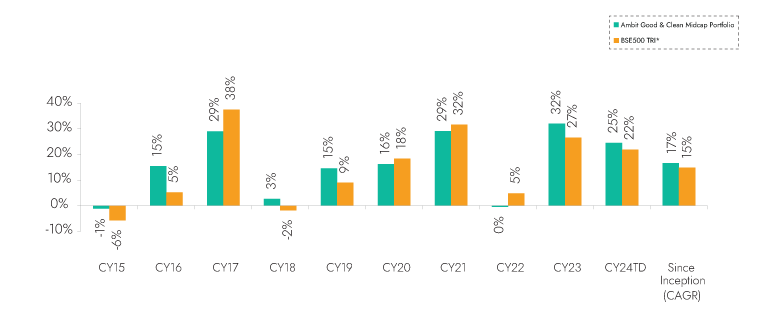

Exhibit 19: Ambit’s Good & Clean Midcap Portfolio calendar year performance

Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015; *BSE 500 50 TRI is the selected benchmark for the Ambit Good & Clean Mid cap. The same is reported to SEBI.

Ambit Emerging Giants Small Cap Portfolio

Small caps with secular growth, superior return ratios and no leverage are the essence of Ambit's Emerging Giants portfolio. The portfolio aims to invest in small-cap companies with market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than INR 4,000 cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt), and the ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence led us to a concentrated portfolio of 15-16 emerging giants.

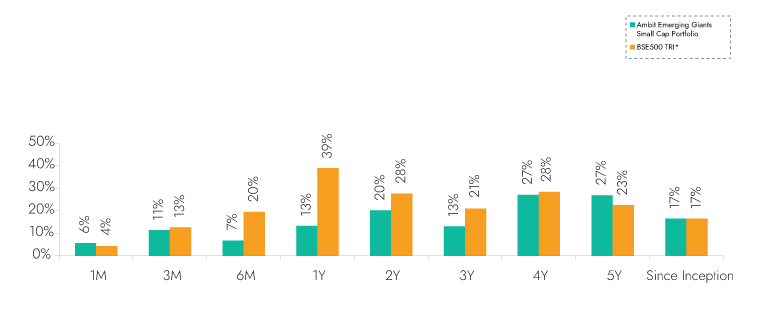

Exhibit 20: Ambit Emerging Giants Portfolio point-to-point performance

Ambit Emerging Giants Small cap Portfolio inception date is Dec 1, 2017; **1M Return: 1st - 31st Jul'24; 3M Return: 1st May'24 – 31st Jul'24; 6M Return: 1st Feb'24 – 31st Jul'24; 1Y Return: 1st Aug'23 – 31st Jul'24 *BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants Small cap. The same is reported to SEBI. In addition to the same, we have included MSCI Smallcap for information purposes only. The same should not be relied upon for performance benchmarking in any manner.

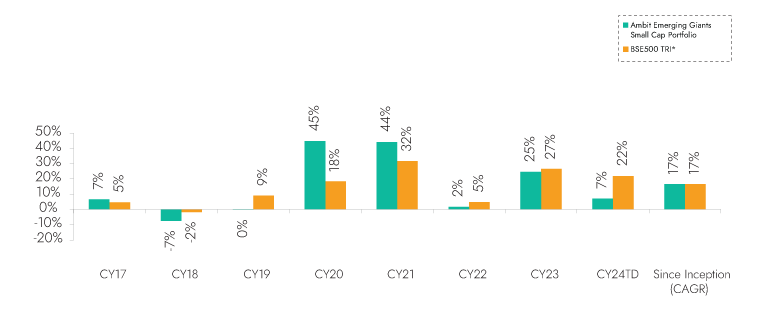

Exhibit 21: Ambit Emerging Giants Portfolio calendar year performance

Ambit Emerging Giants Small cap Portfolio inception date is Dec 1, 2017; *BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants Small cap. The same is reported to SEBI.

Ambit TenX Portfolio

Ambit TenX Portfolio allows investors to participate in the India growth story as the Indian GDP heads towards a US $10 tn mark over the next 12-15 years. Medium and smaller corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that can grow their earnings 10x over the same period implying 18-21% CAGR.

Key features of this portfolio would be as follows:

- Longer-term approach with a concentrated portfolio: Ideal investment duration of more than five years with 15-20 stocks.

- Key driving factors: Low penetration, strong leadership and light balance sheet

- Forward-looking approach: Relying less on historical performance and more on future potential while not deviating away from the Good & Clean philosophy.

- No Key-man risk: Process is the Fund Manager

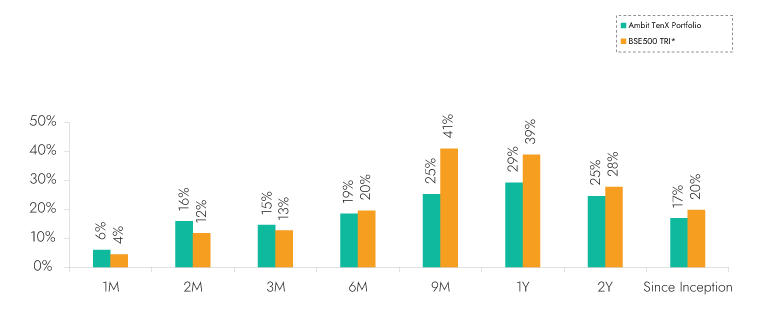

Exhibit 22: Ambit TenX Portfolio point-to-point performance

Ambit TenX Portfolio inception date is Dec 13, 2021; **1M Return: 1st - 31st Jul'24; 3M Return: 1st May'24 – 31st Jul'24; 6M Return: 1st Feb'24 – 31st Jul'24; 1Y Return: 1st Aug'23 – 31st Jul'24 *BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio. The same is reported to SEBI. In addition to the same, we have included MSCI Midcap for information purposes only. The same should not be relied upon for performance benchmarking in any manner.

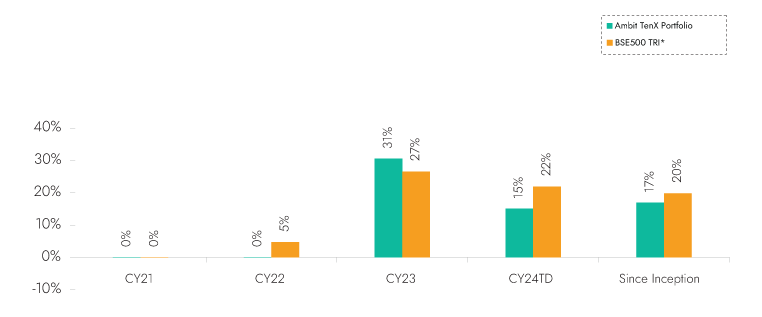

Exhibit 23: Ambit TenX Portfolio calendar year performance

Ambit TenX Portfolio inception date is Dec 13, 2021; *BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio. The same is reported to SEBI.