.jpg)

The strong earnings growth has come in an environment where crude prices had rallied by 40% during March 2026, with supply chain bottlenecks emerging amid the Iranian conflict. While earnings in 1QFY27 may see some impact from the full effect of elevated crude prices this quarter, the possibility of a strong correction in crude from hereon cannot be ruled out, given the elongated ceasefire periods and ongoing global pressure to end the conflict sooner.

For FY27, consensus estimates, as per Bloomberg, point to strong, broad-based double-digit earnings growth across all the aforementioned indices. After two years of underperformance versus emerging-market peers in FY25 and FY26, we believe the recovery is now underway —making this a good time to look at India.

Valuations, despite the recent run-up, continue to be attractive, with India's premium to emerging markets at only ~10% —last seen in 2014. Given ongoing supply chain disruptions and inflation across key commodities, we urge investors to focus on market-leading, quality franchises with strong balance sheets. Such companies are best positioned to navigate the current environment and emerge stronger —as peers with weak balance sheets tend to cede market share during periods of stress.

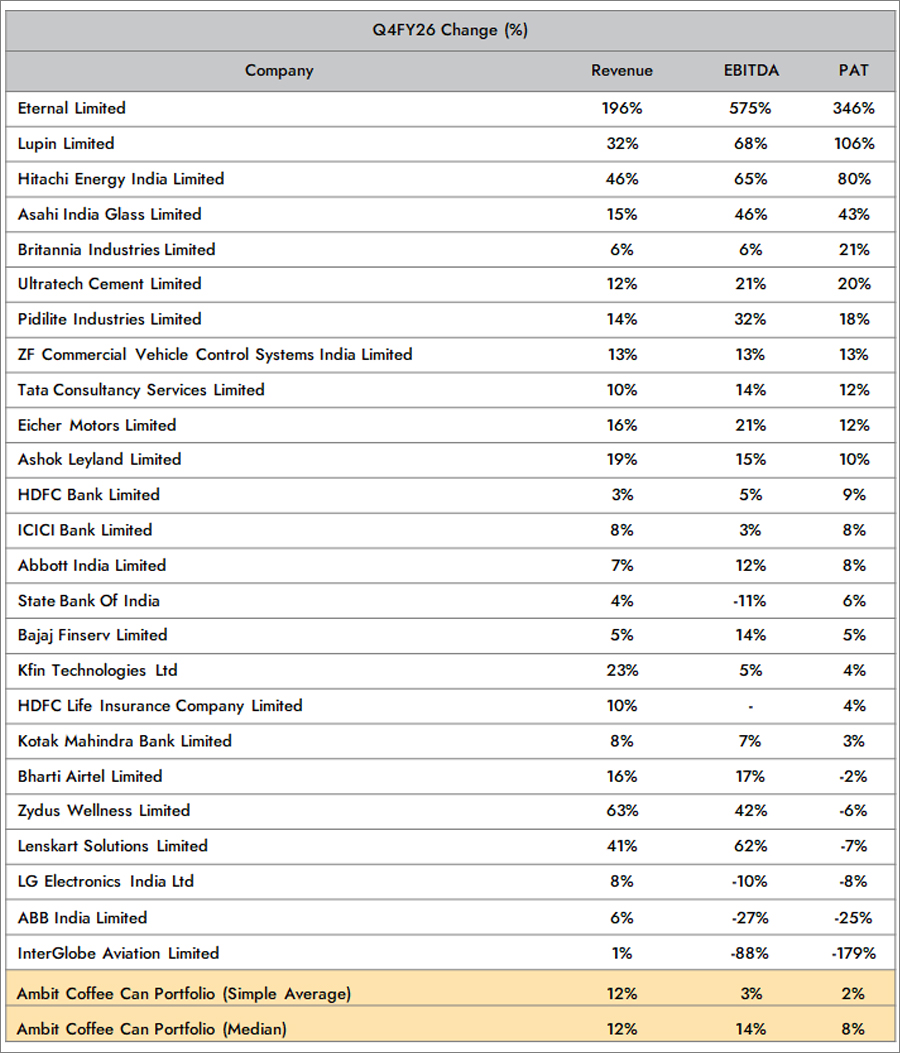

Ambit Coffee Can Portfolio

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has an unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced with disruptions at regular intervals. As the industry evolves or is faced with disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

- Ambit Coffee Can Portfolio delivered revenue/EBITDA/PAT growth of 12%/3%/2% YoY in 4QFY26, vs 13%/1%/4% for Nifty 50 companies.

- Eternal Limited, Lupin Limited and Hitachi Energy India Limited led the earnings growth, delivering an impressive YoY PAT growth of 346%/106%/80% respectively.

- The detractors to the portfolio were LG Electronics Limited/ABB India Limited and InterGlobe Aviation Limited delivering YoY PAT growth of -8%/-25%/-179% respectively.

Note: PAT is calculated excluding exceptional items

Calculation is as per the simple average of absolute Revenue/EBITDA/PAT for all companies.

Source: Ambit Asset Management

Source: Ambit Asset Management

Note: PAT is calculated excluding exceptional items

Eternal Limited

- Eternal reported a strong Q4FY26 performance, with net revenue rising 6% QoQ and 196% YoY to INR 172bn. Consolidated EBITDA stood at INR 4.9bn, translating into an EBITDA margin of 2.8%, compared to 2.3% in the previous quarter. The FD business delivered steady growth, with revenue increasing 2% QoQ and 33% YoY, while Blinkit (QC) revenue grew 8% QoQ.

- Blinkit maintained a healthy contribution margin of 5.4% and reported an Adj EBITDA margin of 0.3%, ahead of expectations of -0.2%. The key highlight of the quarter was Blinkit's transition to positive EBITDA, which significantly supported consolidated profitability and drove Eternal's stronger than expected PAT performance. Pre-IND AS EBITDA jumped ~3.4x YoY to INR 2.65bn, with margin expanding ~680 bp YoY to 11.5% (+40 bp QoQ).

Lupin Limited

- Lupin delivered an exceptionally strong Q4FY26, led by robust traction in the US business driven by niche and FTF launches and continued momentum in India branded formulations. Margins expanded sharply on improved product mix, operating leverage, and cost optimization, driving earnings ahead of expectations.

- Incremental tailwinds included Tolvaptan's sole-generic status, full-year Mirabegron contribution, and Risperdal Consta exclusivity on the US side; chronic mix improvement and field force-led outperformance across Cardiology, Respiratory, and GI supporting India margins; EU crossing $200m reinforcing developed market momentum; a strong EM surprise with Brazil surging 113%.

Hitachi Energy India Limited

- Strong execution across the industries and data centre segments drove the results. EBITDA margin expanded to 16.4% from 12.5% a year ago, supported by higher operating leverage and improved project execution. A massive INR 29,555 crore order backlog - up 54% YoY - provided strong revenue visibility. The company also commissioned India's first HVDC city-centre infeed project in Mumbai.

- Data centres emerged as the largest segment contributor to Q4 order inflows, followed by rail and metro, with exports accounting for 37% of orders -reflecting broad-based demand across geographies including the US, Europe, and APAC. The board also approved an additional INR 2,000 crore capex for a greenfield large power transformer facility in Gujarat, taking cumulative investment commitment to INR 4,000 crore - underscoring management's confidence in sustaining the growth trajectory.

Source: Ambit Asset Management

Note: PAT is calculated excluding exceptional items

LG Electronics Limited

- Commodity inflation and rupee depreciation weighed on Q4 FY26 margins. EBIT margin in Q4 FY26 was also impacted by increased marketing and promotional investments made to capitalise on Cricket World Cup demand. On the positive side, the revenue performance was driven by broad-based demand recovery across categories and continued premiumization momentum.

- LGE India delivered its highest-ever quarterly revenue of INR 80.54 billion, up 8.1% YoY, with the H&A segment growing 5.7% YoY led by French-door refrigerators, fully automatic washing machines, and 5-star-rated ACs driving higher ASPs, while dishwashers emerged as an incremental growth category.

- The HE segment posted a strong 19.6% YoY revenue growth, supported by Cricket World Cup-driven demand for large-screen TVs and robust B2B Information Display order inflows. On the B2B front, LGE India's HVAC solutions — now installed at Seva Teerth, the PM's office building - reflect a deepening institutional presence. Post mid-April heatwave conditions also drove a strong rebound in compressor-based product demand, partially offsetting the earlier rainfall disruptions.

ABB India Limited

- Pressures included higher raw material costs, adverse currency movements, intensifying competition, and slower execution, with EBITDA margin narrowing sharply to 12.82% from 18.59% a year earlier.

- Selective delivery deferrals in metals, cement, and parts of infrastructure reflected rescheduled expansion timelines. Orders grew a robust 25% YoY and the order backlog stood at INR 11,094 crore (+17% YoY), suggesting the growth pipeline remains intact.

- Reported profit was boosted to INR 1,784 crore by a one-time gain from the divestment of the Robotics division.

InterGlobe Aviation Limited

- The rupee depreciated sharply by around 5% against the US dollar during Q4, resulting in a foreign exchange loss of about INR 4,820 crore. These are largely mark-to-market losses linked to aircraft lease and maintenance liabilities.

- The bottom line was also impacted by elevated aviation turbine fuel (ATF) prices and flight cancellations due to the conflict in West Asia. Stripping out forex and exceptional items, IndiGo reported an underlying net profit of INR 1,921 crore for Q4.

- On the operational side, total expenses for FY26 rose 17.2% YoY, driven by higher maintenance costs, depreciation, and forex losses, compressing EBITDAR margin sharply to 17.8% from 26.3% in FY25.

- The company also took on exceptional charges related to new labour codes during the year, further weighing on the reported bottom line.

Note: PAT is calculated excluding exceptional items

Calculation is as per the simple average of absolute revenue/EBITDA/PAT for all companies.

Source: Ambit Asset Management

We expect the strategy's earnings growth to pick up as discretionary businesses recover. Steady compounders and proven franchises will continue to demonstrate resilience despite inflationary pressures in FY27.

On valuations, the portfolio is attractively valued at 34x FY27 PE despite a 22% EPS CAGR over FY25-27 and an ROE of 22% in FY27. Relative to the Nifty, the portfolio trades at a 75% premium given superior earnings growth and ROE.

Portfolio - Performance

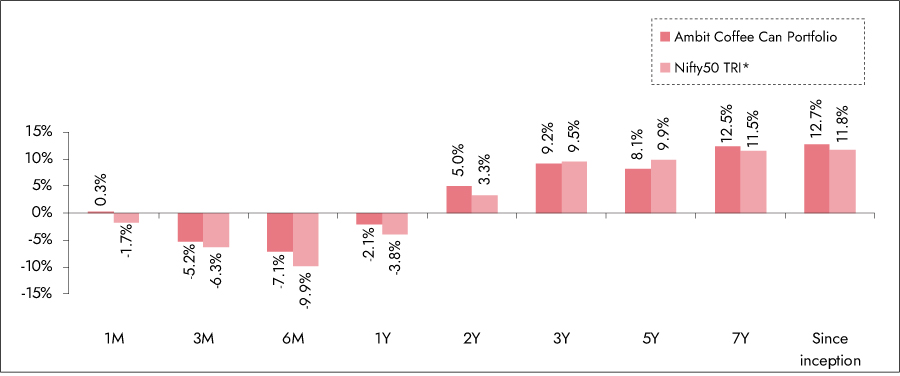

Exhibit 1: Ambit Coffee Can Portfolio point-to-point performance

Source: Ambit Coffee Can Portfolio inception date is Jun 20, 2017;

1M Return: 1st - 31st May'26; 3M Return: 1st Mar'26 – 31st May'26; 6M Return: 1st Dec'25 – 31st May'26; 1Y Return: 1st Jun'25 – 31st May'26

*Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The performance related information provided herein is not verified by SEBI.

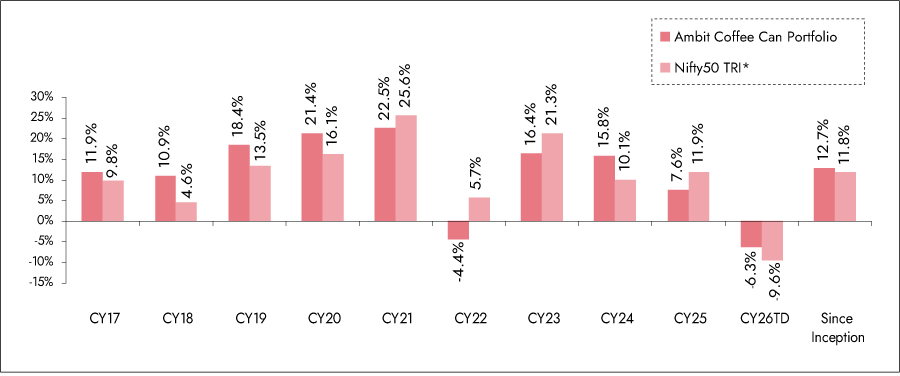

Exhibit 2: Ambit Coffee Can Portfolio calendar year performance

Source: Ambit Coffee Can Portfolio inception date is June 20, 2017;

*Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The performance related information provided herein is not verified by SEBI.

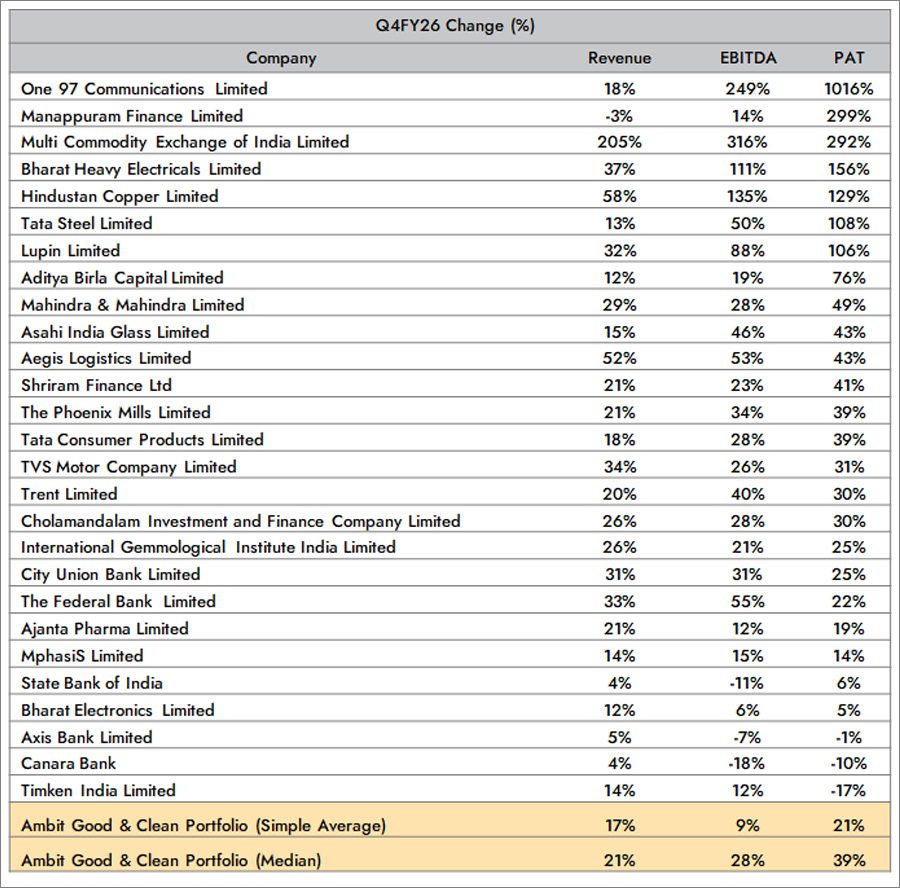

Ambit Good & Clean Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

- Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of around 25 companies at any time.

- Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longer with annual churn around 35% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with these compounding earnings acting as the primary driver of investment returns over long periods.

- Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

On the earnings front, the strategy delivered Revenue/EBITDA/PAT growth of 17%/9%/21% on a YoY basis in 4QFY26 vs 14%/12%/ 31% for the Nifty Midcap 150 Index.

The earnings growth was led by One97 Communications Limited, Manappuram Finance Limited and Multi Commodity Exchange of India Limited delivering an impressive YoY PAT growth of 1016%, 299%, and 292%, respectively.

The detractors to the portfolio were Axis Bank Limited, Canara Bank Limited and Timken India with the companies delivering YoY PAT growth of -1%, -10%, and -17% respectively.

Note: PAT is calculated excluding exceptional items

Calculation is as per the simple average of absolute Revenue/EBITDA/PAT for all companies.

Source: Ambit Asset Management

Top 3 and Bottom 3 Performers:

Source: Ambit Asset Management

Note: PAT is calculated excluding exceptional items

Ambit Good & Clean Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

- Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of around 25 companies at any time.

- Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longer with annual churn around 35% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with these compounding earnings acting as the primary driver of investment returns over long periods.

- Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

One 97 Communications Ltd

- Paytm reported better than expected revenue growth of 18% YoY to INR 22.6bn, driven by healthy GMV growth of 27% YoY to INR 6.5tn and continued market share gains in payments.

- Financial services revenue remained strong, growing 38% YoY, supported by merchant lending partnerships, while adjusted PAT came in at INR 1.6bn, reflecting sustained profitability. Payment processing margins remained healthy at >4bps, underpinned by product improvements, pricing discipline, and rising credit instrument usage on UPI.

- Merchant lending penetration reached 7% of subscription devices, up 1% YoY, with both online and offline merchant businesses performing well following onboarding-related challenges last year.

- Lending momentum remained strong, particularly in personal loans, with earlier headwinds gradually turning into tailwinds. On costs, indirect expenses rose QoQ due to annual appraisals, though incremental investments are being directed toward AI -focused on merchant experience, marketing monetization, and reducing customer churn - with capex intensity expected to remain below revenue growth.

Manappuram Finance Limited

- Strong growth momentum continued with AUM growing 48% YoY, led by nearly 100% YoY growth in the gold loan portfolio, reflecting healthy demand and market share gains.

- Normalization in the MFI segment, despite margin pressures from competitive gold loan pricing and a softer NII performance.

- Asset quality improved meaningfully with both gold loan and MFI businesses reporting lower NPAs, while improving collection efficiencies and lower credit costs supported earnings.

Multi Commodity Exchange of India Limited

- MCX contributed positively as Q4FY26 PAT surged 291% YoY to INR 5.3bn, driven by strong growth in Futures ADTO (+230% YoY) and Options Premium ADTO (+233% YoY). Retail participation remained robust, with trading clients rising 60% YoY to 2.1mn, while bullion volumes expanded sharply and reduced energy's revenue contribution to 52% from 73% a year ago.

- Management commentary on sustained volume growth, potential FPI participation in bullion contracts, and upcoming product launches across metals and indices was strong.

Source: Ambit Asset Management

Note: PAT is calculated excluding exceptional items

Axis Bank Limited

- Loan growth remained healthy at 18% YoY (+6% QoQ), led by strong corporate loan growth of 38% YoY, while management continued to prioritize growth based on risk-adjusted returns.NII grew 5% YoY, with NIM largely stable at 3.62% despite the rate-cut environment, and management reiterated its medium-term NIM guidance of ~3.8%.

- Asset quality trends improved, with slippages declining to 1.6% from 2.1% in the previous quarter, while core credit costs remained contained at 40bps despite higher reported provisioning.

Canara Bank Limited

- Core operating performance remained resilient with NII growing 4% YoY to INR 98.1bn and NIM improving 9bps QoQ to 2.54%, supported by a lower cost of deposits. Loan growth remained strong at 15% YoY, led by retail and gold loans, with gold loans growing 33% YoY to INR 2,450bn and now accounting for ~20% of the loan book.

- Asset quality continued to improve, with GNPA and NNPA declining to best-ever levels of 1.84% and 0.43%, respectively, while credit costs remained low at 0.59% despite higher MSME and agriculture slippages.

Timken India Limited

- Timken delivered 14% Revenue growth in Q4 driven by strong growth in Mobile, Process and Exports business segments. Gross Margin for the company expanded by 400 bps QoQ flowing down to EBITDA margin expansion of 880 bps QoQ.-EBITDA for the company grew by 12% YoY.

- PAT declined for the co. largely due to 40% growth in depreciation on a YoY basis (driven by capitalization of the CRB+SRB facility) and lower other income by 81% on a YoY basis and the company remains confident of CRB+SRB ramp-up in the coming quarters which will aid topline growth and margin expansion.

Note: PAT is calculated excluding exceptional items

Calculation is as per the simple average of absolute revenue/EBITDA/PAT for all companies.

Source: Ambit Asset Management

We expect the earnings growth of the strategy in FY27 to be led by higher growth in financials. New economy stocks, energy transition and commodity proxies will witness earnings acceleration as realizations and execution improve.

On valuations, the portfolio is attractively valued at 34x FY27 PE despite a 22% EPS CAGR over FY25-27 and an ROE of 22% in FY27. Relative to the Nifty Midcap 150 Index, the portfolio trades at a 75% premium given superior earnings growth and ROE.

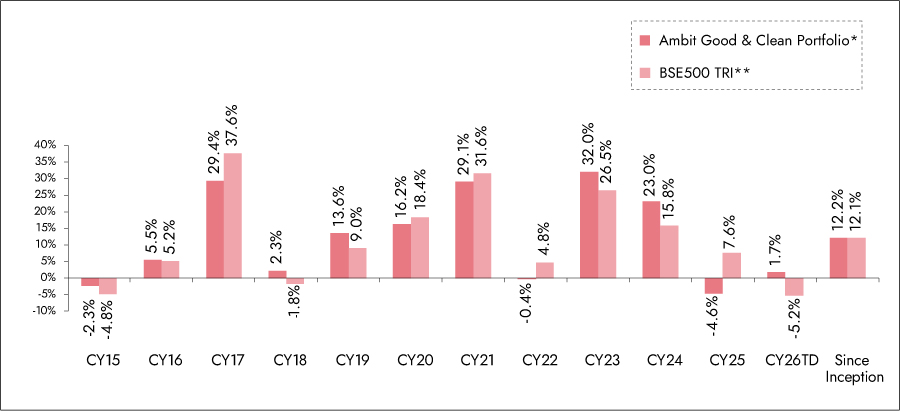

Portfolio - Performance

Exhibit 3: Ambit Good and Clean Portfolio point-to-point performance

Source: Ambit Good & Clean Portfolio inception date is March 12, 2015;

1M Return: 1st - 31st May'26; 3M Return: 1st Mar'26 – 31st May'26; 6M Return: 1st Dec'25 – 31st May'26; 1Y Return: 1st Jun'25 – 31st May'26

*The name of the investment approach has been changed from Ambit Good & Clean Midcap Portfolio to Ambit Good & Clean Portfolio with effect from June 02, 2026.

**BSE 500 TRI is the selected benchmark for the Ambit Good & Clean. The performance related information provided herein is not verified by SEBI.

Exhibit 4: Ambit Good and Clean Portfolio calendar year performance

Source: Ambit Good & Clean Portfolio inception date is March 12, 2015;

*The name of the investment approach has been changed from Ambit Good & Clean Midcap Portfolio to Ambit Good & Clean Portfolio with effect from June 02, 2026.

**BSE 500 TRI is the selected benchmark for the Ambit Good & Clean. The performance related information provided herein is not verified by SEBI.

Ambit Micro Marvels Portfolio

We aim to create a portfolio that invests predominantly in micro-cap companies with the potential of delivering superior earnings growth and generating relatively better risk-adjusted performance over a long period of time.

Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts while our proprietary ‘greatness’ framework helps identify efficient capital allocators. The result is a concentrated portfolio of 20-25 stocks that draws down less than the market in corrections and has low churn.

Key Features of Portfolio Companies:

- High earnings growth companies with low leverage,

- Market leaders or challengers with strong moat around brand, distribution, technology, and innovation,

- Strong corporate governance coupled with apt capital allocation.

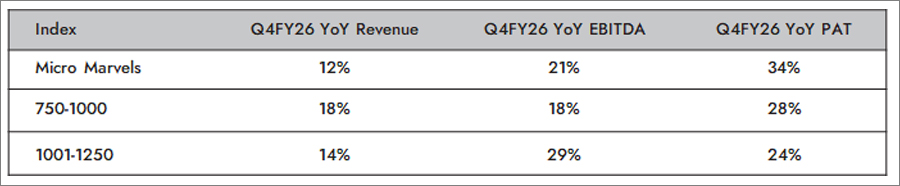

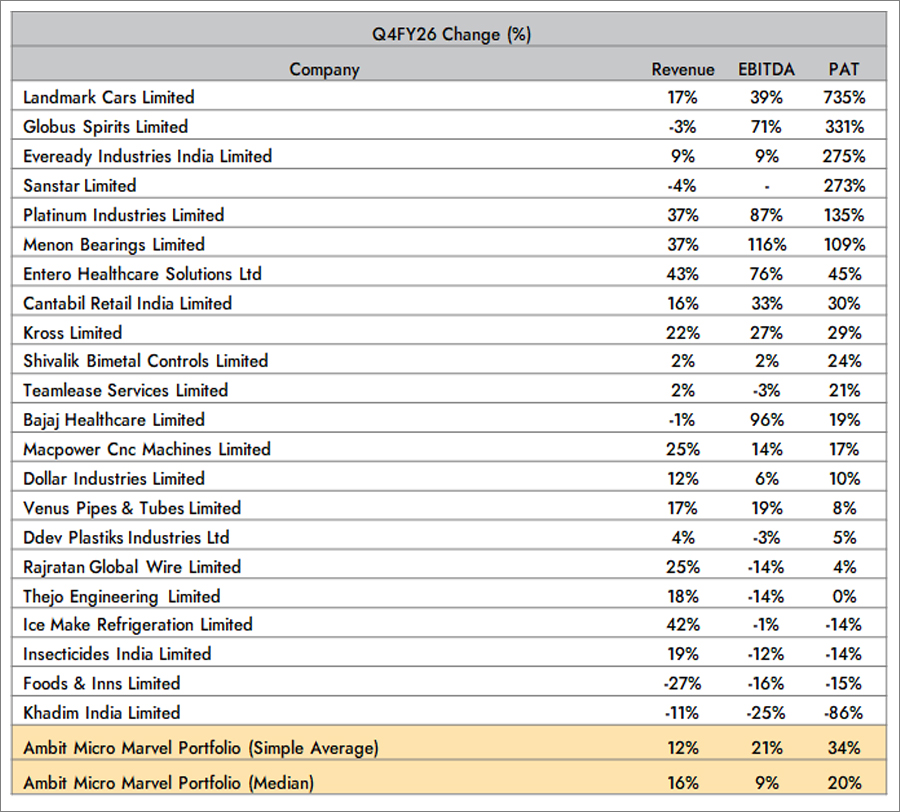

On the earnings front, the strategy delivered Revenue/EBITDA/PAT growth of 12%/21%/34% on a YoY basis in 4QFY26 vs 17%/25%/31% for benchmark companies.

The earnings growth was led by Landmark Cars Limited, Globus Spirits Limited, Eveready Industries India Limited which delivered impressive YoY PAT growth of 735%, 331%,

and 275%, respectively.

The detractors to the portfolio were Insecticides Limited, Foods & Inns Limited, Khadim India Limited with the companies delivering YoY PAT growth of -14%, -15%, and - 86%, respectively.

Micro Marvels’s earnings growth exceeded that of its peers in 4QFY26 on a YoY basis

Note: PAT is calculated excluding exceptional items

Calculation is as per the simple average of absolute Revenue/EBITDA/PAT for all companies.

Source: Ambit Asset Management

Top 3 and Bottom 3 Performers:

Source: Ambit Asset Management

Note: PAT is calculated excluding exceptional items

Landmark Cars Limited

- Revenue grew by ~17% YoY, supported by strong traction in recently added OEM partnerships such as M&M, MG, and Kia.

- The company also generated operating cash flows of over INR 2 billion during FY26, reflecting efficient working capital management and strong cash conversion.

- A key highlight was the after-market business crossing INR 10 billion in revenue during FY26, making Landmark the first automotive dealership group in India to achieve this milestone.

- The increasing contribution from this higher-margin and more stable revenue stream continues to support profitability and earnings quality.

Globus Spirits Limited

- EBITDA per litre in the manufacturing business increased from INR 7.5 to INR 8.3, reflecting better operating efficiencies and product mix.

- The R&O segment witnessed healthy growth in its core markets of Rajasthan and Uttar Pradesh, while the P&A segment continued to scale profitably, with four of its five mature markets reporting profitability. These trends indicate improving execution across the value chain and support the company's profitability outlook.

Eveready Industries India Limited

- During the quarter, the company commissioned its Jammu facility for alkaline battery production, with output expected to reach 200 million units in the first year against a total capacity of 650 million units.

- Eveready also entered into agreements to monetize two land parcels in Noida, resulting in an exceptional gain of INR 102 crore. In addition, improving rural consumption trends and a healthier demand environment supported growth across its core battery and lighting businesses.

Source: Ambit Asset Management

Note: PAT is calculated excluding exceptional items

Insecticides India Limited

- Gross margins declined following a sharp increase of over 10% in key raw material prices. While higher input costs weighed on near-term profitability, the company undertook several strategic initiatives that are expected to support long-term growth.

- The launch of ICF is a positive step towards increasing the adoption of branded products, which should improve product mix and pricing power over time.

- Additionally, the introduction of an ESOP program is expected to aid talent acquisition and retention, strengthening the company's ability to attract high-quality professionals and support future growth initiatives.

Foods and Inns Limited

- Volumes were impacted by disruptions arising from the war situation during March, which affected demand and shipment schedules during the quarter.

- Additionally, average realizations declined by ~25% YoY as the company sold inventory manufactured during the 2025 crop season, when raw material costs were substantially lower.

- Despite the pressure on revenue, the company expects volumes to grow by 18% in FY27 and has indicated that EBITDA per tonne will be maintained, reflecting the company's RM pass through model.

Khadim India Limited

- Profitability remained under pressure as gross margins were impacted by price reductions in products with ASPs below INR 500, undertaken to remain competitive in a weak demand environment.

- Despite these headwinds, the company maintained a strong focus on inventory optimization and working capital discipline throughout FY26, helping preserve balance sheet strength.

- Management intends to continue this measured approach in FY27, with a focus on efficient inventory management and prudent working capital allocation, positioning the company to benefit when demand conditions improve.

Note: PAT is calculated excluding exceptional items

Calculation is as per the simple average of absolute Revenue/EBITDA/PAT for all companies.

Source: Ambit Asset Management

The portfolio has delivered strong profit growth of 34%, yet valuations remain compelling at 20.6x FY27E P/E and 0.8x FY27E PEG, suggesting that the growth trajectory is still not fully reflected in prices.

We remain optimistic about performance in the coming quarters, supported by a confluence of favourable macro developments.

- Expectation of a peace agreement between Iran and the US, which will normalize oil prices and global supply chains

- The India–US trade agreement, which caps tariffs at 18%, is positive both for trade flows and investor sentiment.

- The announcement of the India–EU FTA provides structural, long-term tailwinds across sectors by enhancing export competitiveness and market access.

- Additionally, the GST rate cut announced on September 22nd 2025 is expected to stimulate consumption, with the benefits likely to be reflected more meaningfully in earnings over the next few quarters.

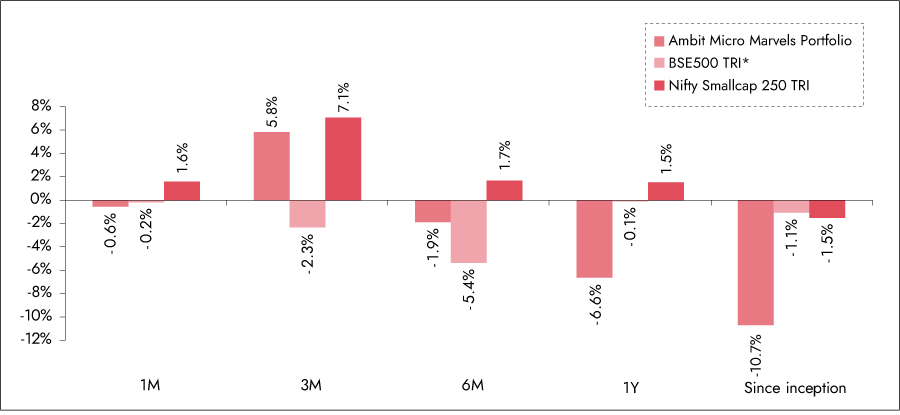

Portfolio - Performance

Exhibit 5: Ambit Micro Marvels Portfolio point-to-point performance

Source: Ambit Micro Marvels Portfolio inception date is Jul 29, 2024;

1M Return: 1st - 31st May'26; 3M Return: 1st Mar'26 – 31st May'26; 6M Return: 1st Dec'25 – 31st May'26; 1Y Return: 1st Jun'25 – 31st May'26

*BSE 500 TRI is the selected benchmark for the Ambit Micro Marvels Portfolio. The performance related information provided herein is not verified by SEBI.

Nifty Smallcap 250 TRI is the secondary benchmark, being provided solely for additional reference and comparison. For details refer disclaimer clause.

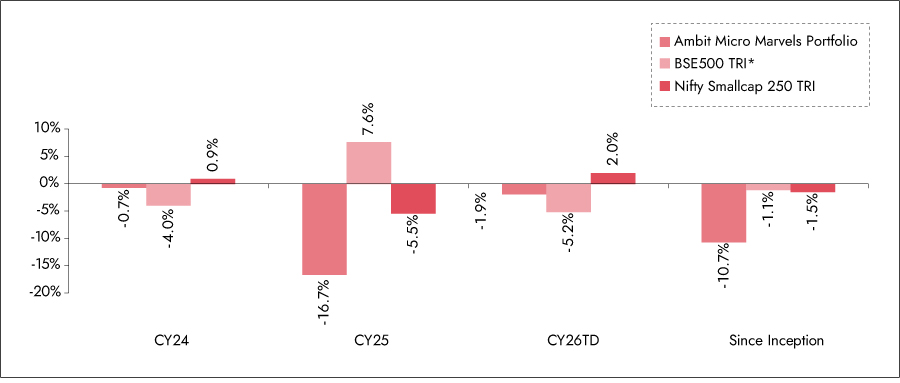

Exhibit 5: Ambit Micro Marvels Portfolio calendar year performance

Source: Ambit Micro Marvels Portfolio inception date is Jul 29, 2024;

*BSE 500 TRI is the selected benchmark for the Ambit Micro Marvels Portfolio. The performance related information provided herein is not verified by SEBI.

Nifty Smallcap 250 TRI is the secondary benchmark, being provided solely for additional reference and comparison. For details refer disclaimer clause

Conclusion:

We believe it is a good time to increase allocations to the Indian markets, given relative underperformance to its emerging markets peers in FY26 and significant recovery in earnings growth expected in FY27 across Nifty, NSE500, Nifty small cap and Nifty microcap indices.

Given the on-going supply chain issues and inflation across key commodities, we urge investors to invest in market leading quality franchises with strong balance sheets as this allows them to not only navigate this period of crisis but also emerge stronger post crisis as weak balance sheet companies lose on market share.

Ambit Pricing Prowess Fund

- Ambit Pricing Prowess Fund is an All-weather, Open-ended, Long-only, Category III, Flexi-cap AIF – a meticulously crafted opportunity for long-term investors seeking:

- Accelerated Portfolio Returns: The ability to raise selling prices faster than input costs (inflation) directly increases profit margins and accelerates Free Cash Flow (FCF) growth.

- Unrivaled Portfolio Resilience: Pricing Power acts as a structural defense mechanism, stabilizing margins even during periods of macro pressure, supply shocks, or weaker demand.

- Maximum Long-Term Value Creation: Pricing Power is a proxy for an irrefutable competitive advantage (deep moat).

In a market of highly varied valuations, Ambit Pricing Prowess Fund is not constrained by a single market segment. We are designed to seek the most attractive combination of

Quality and Price across the entire investment universe.

We can shift capital fluidly between Large, Mid, Small, and even a select number of carefully vetted unlisted businesses. This broad mandate allows us to find and capitalize on unique opportunities that align with our core framework.

Investing in businesses with Pricing Prowess offers compelling advantages, as below:

- Proven Inflation Hedge

- Maximized Profit Margins

- Stable, Quality Compounding (non-Glamorous)

- Formidable Entry Barriers

- Long-term Value Creation

Exhibit 7: Ambit Pricing Prowess Fund point-to-point performance

1781590099525.jpg)

1M Return: 1st - 31st May'26; 3M Return: 1st Mar'26 – 31st May'26; 6M Return: 1st Dec'25 – 31st May'26

Note: First close for Ambit Pricing Prowess Fund was done on 24th Sept 2025; Returns are computed at Fund level and are pre fees and on pre-tax basis. Returns of BSE 500

and Nifty 50 is being provided solely for additional reference and comparison. The performance related information provided herein is not verified by SEBI.

Exhibit 8: Ambit Pricing Prowess Fund calendar year performance

1781590106957.jpg)

Note: Data as on 31st May 2026; First close for Ambit Pricing Prowess Fund was done on 24th Sept 2025; Returns are computed at Fund level and are pre fees and on pre-tax

basis. Returns of BSE 500 and Nifty 50 is being provided solely for additional reference and comparison. The performance related information provided herein is not verified by SEBI.