India - Better placed than peers

“India deserves to be called a bright spot on this otherwise dark horizon because it has been a fast-growing economy, even during these difficult times, but most importantly; this growth is underpinned by structural reforms”

– Kristalina Georgieva, IMF MD (Oct 14, 2022)

As nations around the world grapple with high inflation, the fulcrum of central banks has moved towards taming inflation, even if it’s at the cost of growth. Expectations for growth have been trimmed in all regions and almost three quarters of respondents (surveys organized by the WEF’s Centre for the New Economy and Society) now consider a global recession to be at least somewhat likely (Refer to Exhibit: 1). However, recession is unlikely to hit India due to its 'not so coupled' nature with global economy.

Exhibit 1: Global recession outlook – Likelihood of recession in 2023?

Source: Chief Economists Survey, August 2022; Ambit Asset Management. Note: The number in the graphs may not add up to 100% because figures have been rounded up/down

Tightening fiscal and monetary policies can, however, address inflation only from the demand side. Simultaneously, from the supply side, trade disruptions, export bans and the resulting surge in global commodity prices will continue to stoke inflation if Russia-Ukraine conflict persists, and global supply chains remain un-repaired. The world is looking at a distinct possibility of widespread stagflation. For now, there has been an exception: India, where the risk is lower for India than other countries.

Compared to other nations, even among the advanced economies, India is relatively better prepared to handle external shocks that could be created by the tightening of the monetary policy stance. In its policy meeting in Aug, The Reserve Bank of India (RBI) kept the growth forecast at 7% for FY23 despite disruptions due to geo-political tensions. (Refer to Exhibit: 2)

Exhibit 2: India expected to witness positive growth momentum with moderate inflation risk

Source: Sept. 2022 CPI - Monthly Economic Review; World Economic Outlook, Oct 2022; Ambit Asset Management

In this newsletter we look at what explains this sudden optimism for an economy that was seeing a major slowdown in growth even before the Covid-19 pandemic hit and why the “sweet/bright spot” terminology has been embraced by many.

Macro-economy looks stronger

Notwithstanding the pandemic’s severe shock, India's macro economy looks stronger as compared to those of other emerging markets and during that of Quantitative Easing of 2013. (1) India’s low external debt, which has insulated it from extreme external volatility. (2) India’s foreign exchange reserve could cover imports for 8.4 months. (Refer to Exhibit: 3,4)

Exhibit 3: External debt to GDP came down to 19.3 % in March 22 from 21.2% during March 2021

Source: Department of Economic Affairs; Ambit Asset Management

Exhibit 4: India’s reserve cover of ~8.4 months of imports is much higher than ~6.5months during the taper tantrum in 2013

|

Rank |

Country |

Forex Reserves (US$ bn) |

Import cover |

|

1 |

China |

3,194 |

13 |

|

2 |

Japan |

1,238 |

16.3 |

|

6 |

India* |

528 |

8.4 |

|

12 |

Germany^ |

281 |

0.3 |

|

14 |

United States |

229 |

0.1 |

|

19 |

United Kingdom |

178 |

2.7 |

Source: Ambit Asset Management, World Bank. Note: *October and the rest is Sept; ^August 22;

Majorly, India is an inward-looking economy in terms of demand because a significant component of the GDP is essentially addressed to the domestic economy. So, from that point of view, global recession will have an impact but it won't be as pronounced as perhaps (it will be on) other economies which are more coupled with the globe. (Refer to Exhibit: 5)

Exhibit 5: India aims to raise its exports share to 3 per cent by 2027, and to 10 per cent by 2047

Source: Ambit Asset Management

Most global banks and agencies have downgraded their growth outlook for India to below 7%. ‘A weaker-than-expected outturn in the period of April to June, and more subdued external demand’ have prompted a reduction in India’s FY23 GDP estimate. As per the IMF, the world as a whole will slow down from 6.0% in 2021 to 3.2% in 2022 and 2.7% in 2023. Despite the cut in estimates, excluding Saudi Arabia, as per the IMF, India is the only economy that is likely to witness a GDP growth rate of over 6% (higher than major advanced and emerging market economies). (Refer to Exhibit: 6, 7).

Exhibit 6: Most global banks and agencies have downgraded their growth outlook for India to < 7 %

Source: Ambit Asset Management, News articles.

Exhibit 7: IMF cuts India’s FY 2022-23 growth forecast to 6.8%

|

Countries / Regions |

CY 22 (revised est.) |

CY 22 (previous est.) |

Change in est. |

CY 23 |

|||

|---|---|---|---|---|---|---|---|

|

World |

3.2 |

3.2 |

0% |

2.7 |

|||

|

Advanced Economies |

2.4 |

2.5 |

-4% |

1.1 |

|||

|

USA |

1.6 |

2.3 |

-30% |

1 |

|||

|

Euro Area |

3.1 |

2.6 |

19% |

0.5 |

|||

|

Japan |

1.7 |

1.7 |

0% |

1.6 |

|||

|

Emerging Markets |

3.7 |

3.6 |

3% |

3.7 |

|||

|

China |

3.2 |

3.3 |

-3% |

4.4 |

|||

|

India |

6.8 |

7.4 |

-8% |

6.1 |

|||

|

Russia |

-3.4 |

-6 |

-43% |

-2.3 |

|||

|

Brazil |

2.8 |

1.7 |

65% |

1 |

|||

|

Mexico |

2.1 |

2.4 |

-13% |

1.2 |

|||

|

South Africa |

2.1 |

2.1 |

0% |

1.1 |

|||

Source: Ambit Asset Management, IMF World Economic Outlook, Oct 2022

Consumption – keeping Indian brands bullish

Domestic consumption – traditionally one of the main drivers of India's economic growth – is making a strong comeback; Pent up domestic demand and significant deleveraging across sectors has aided recovery to a large extent. Simply put, when consumers spend more, businesses have more capital to invest.

According to a confidence survey conducted for Indian corporates, >60% were very optimistic about the demand outlook while ~35% have responded with a stable demand outlook for the next year. High frequency economic indicators for India corroborate this with higher e-commerce, auto sales, and discretionary consumption along with demand traction visible in the bank credit growth.

- E-commerce companies such as Wal-Mart - owned Flipkart and Amazon have sold $4.1 billion (Rs 29,000 crore) worth of goods during the October 15-21 period, up from $2.7 billion year ago

- Retail businesses across India reported a 21% jump in sales in September 2022 compared to September 2019 or pre-pandemic levels according to the Retailers Association of India.

- India's vehicle retail sales rose 57% during the Navratri festival this year, recording sales of nearly 5.4 lakh units. (Refer to Exhibit: 8).

Exhibit 8: Navratri sales show that customers are back in showrooms after a gap of three years

|

Category |

Navratri '22 |

Navratri '21 |

Navratri '20 |

YoY% (2021) |

YoY% (2020) |

Navratri'19 |

YoY% (2019) |

|

2w |

369,020 |

242,213 |

307,903 |

52% |

20% |

355,851 |

4% |

|

3w |

19,809 |

9,203 |

5,952 |

115% |

233% |

15,082 |

31% |

|

CV |

22,437 |

15,135 |

11,142 |

48% |

101% |

16,365 |

37% |

|

PV |

110,521 |

64,850 |

86,380 |

70% |

28% |

69,657 |

59% |

|

Tractor |

17,440 |

11,062 |

14,387 |

58% |

21% |

9,177 |

90% |

|

Total |

539,227 |

342,459 |

425,761 |

57% |

27% |

466,128 |

16% |

Source: FADA; Ambit Asset Management

Global CEO’s of more than half a dozen large consumer-facing companies such as Apple, Coca-Cola, Visa, Whirlpool, Skechers and Levi Strauss have highlighted in their recent earning calls that their companies’ India business has grown at double digit pace in the September quarter and that they will continue to invest strongly.

However, rural demand has taken a knock since the pandemic and has not participated in the recovery till now. This year’s Diwali was the country’s first season of celebration since the pandemic began, with no virus-related restrictions and with the rural market seeing good rain, consumption could bounce back in the 2nd half of the year. This would lead to recovery in the ailing rural sector as well.

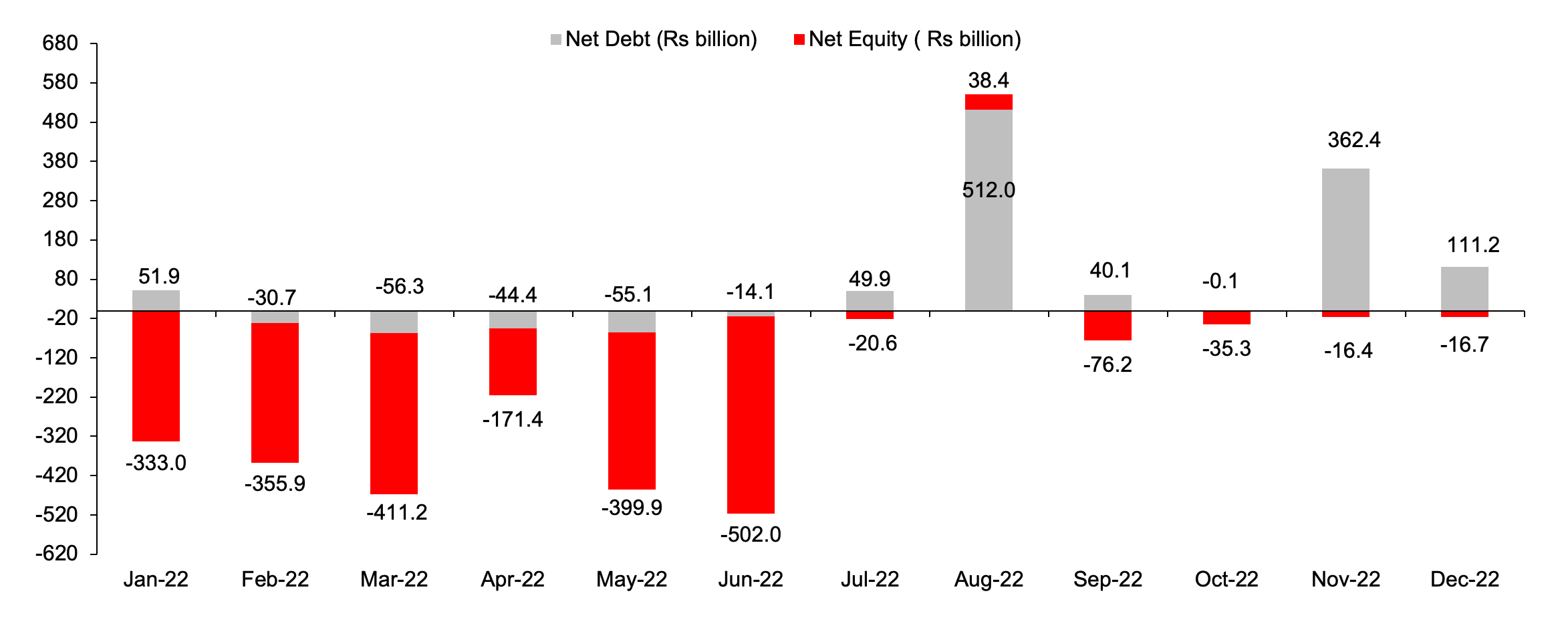

Import substitution and realignment of supply chain

China’s continued adherence to the zero-Covid strategy has prompted global capital to look elsewhere for investment opportunities (in addition to the efforts to diversify from China). With India appearing to weather the current “poly-crisis” better than many of its neighbours and peers, it is seen as an emerging manufacturing hub in global value chains.

71% of MNCs consider India as an important destination for their global expansion according to a report released by EY-CII. The report underscores that India has optimistic growth prospects for foreign investments with a potential to attract FDI flows of US$ 475 billion in just the next 5 years.

Exhibit 9: FDI in India has seen a consistent rise in the last decade, with FY2021-22 FDI inflow of US$ 84.8 billion

Source: Ambit Asset Management; Bloomberg.

Exhibit 10: Capital expenditure seeing an upward trend due to Govt sponsored schemes such as PLI etc.

Source: Ambit Asset Management; Note: Capacity utilization is taken for Q3FY22

All this has resulted in India gaining market share in electronics, chemicals, apparel, auto components. Thus, even though the global supply chain is under stress, the market share gains are helping India offset some of the impact in the near term. India’s export – from pre covid $27.65 billion (Feb 2020) has gone up to $61 billion (September 2022).

Exhibit 11: In Sept, 22, India mobile phone exports crossed $1bn (all time high) primarily due to Government’s PLI scheme

Source: Ambit Asset Management, Statista, CRISIL

Exhibit 12: Export value of mobile phones in India is likely to rise. The PLI scheme has the potential to add ~US$ 520 billion in the next five years.

|

Mobile trade dynamics |

Top world importers (% share) |

||||

|

USA |

Hong Kong |

Japan |

Germany |

UAE |

|

|

China |

79% |

86% |

89% |

67% |

63% |

|

Vietnam |

16% |

1% |

6% |

11% |

21% |

|

India |

0% |

0% |

1% |

3% |

9% |

|

Total global exports |

20% |

15% |

6% |

4% |

5% |

Source: Ambit Asset Management, CRISIL

Companies are rethinking their strategy of putting “all eggs in one basket”. India is generally considered an attractive destination because of its market size and also India being a possible hub for exports in the region. That's the reason a lot of interest is being shown by companies towards India.

- Foxconn is entering into a $19.5 billion joint venture with Vedanta Group to make semiconductors in the western state of Gujarat.

- TATA is in talks to become a contract manufacturer for Apple in the country

- Amazon has been making Fire TV devices in Chennai, India. Several years ago, all of these products were made in China.

- Samsung will move part of its smartphone production to India from Vietnam and other countries. The South Korean company is planning to produce devices worth over $40 billion or Rs 3 lakh crore in the country.

- Boston-based start-up Thrasio, a global leader in acquiring and scaling up third-party sellers on online marketplaces such as Amazon, will shift a significant chunk of its manufacturing.

- Apparel orders from neighbouring countries are shifting to India as it has proved to be the most stable country in the sub-continent region

Conclusion

India entered this decade and this conflict (Russia-Ukraine) with a fairly comfortable degree of macro-economic and policy stability. Recovery from both the first and second waves was faster than expected pointing towards the inherent strengths of the economy. Moreover, it has enough foreign exchange reserves to ride out the current volatility while ensuring interest rates are aligned to the domestic policy cycle. This gives India a lot of cushion to withstand the pressures it faced during taper tantrum of 2012-13. In the coming winter months, geopolitical tensions could climb amid a heightened international focus on energy security and that could test “India’s astute handling of its energy needs so far.” The current market volatility reinforces our confidence within our investible companies across the portfolio which has attributes of Consistency, Resilience & Margin of Safety.

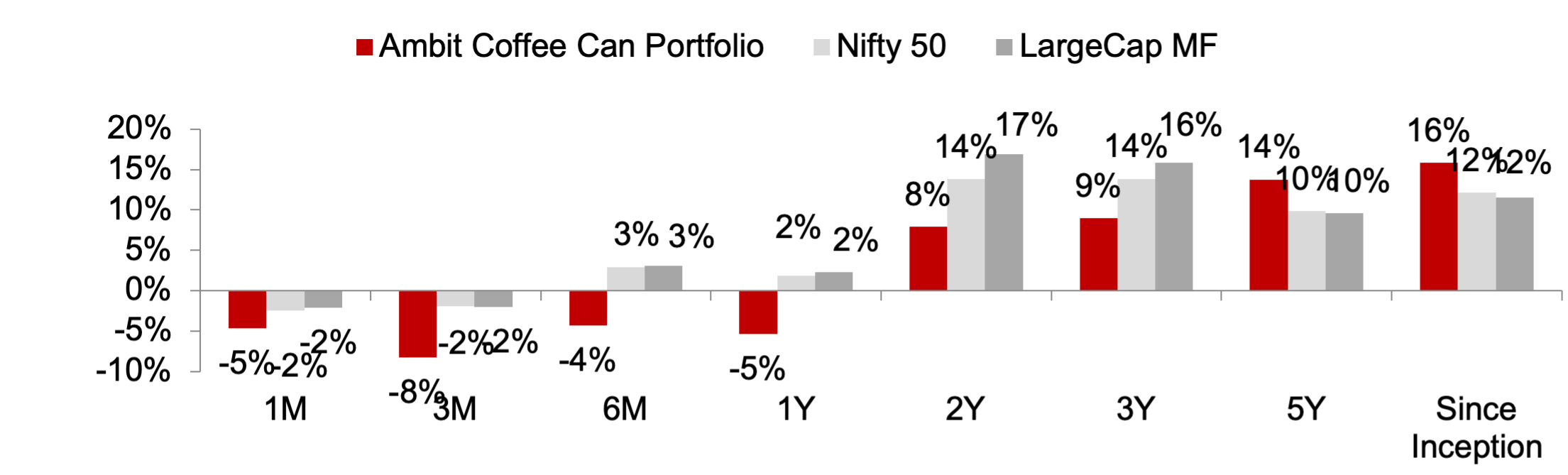

Ambit Coffee Can Portfolio

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced by disruptions at regular intervals. As the industry evolves or is faced by disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

Exhibit 12: Ambit’s Coffee Can Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of 31st Oct, 2022; All returns are post fees and expenses; Returns above 1-year are annualized; Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts.

Exhibit 13: Ambit’s Coffee Can Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of 31st Oct, 2022; All returns are post fees and expenses. Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts.

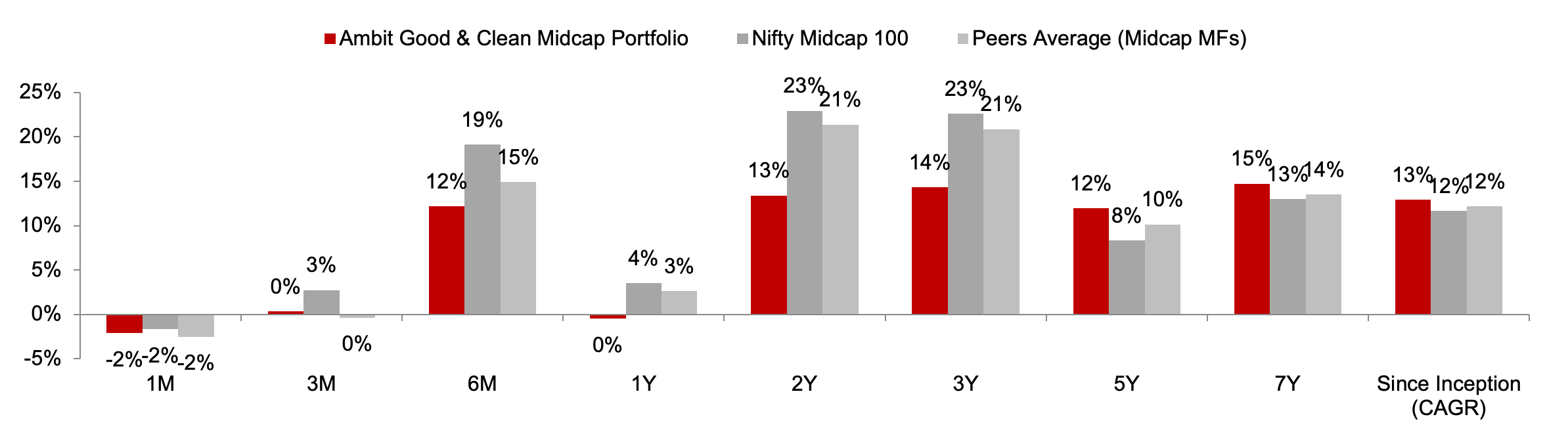

Ambit Good & Clean Midcap Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver superior risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

- Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

- Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longer with annual churn not exceeding 15-20% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with this compounding earnings acting as the primary driver of investment returns over long periods.

- Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

Exhibit 14: Ambit’s Good & Clean Midcap Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of 31st Oct, 2022; All returns above 1 year are annualized. Returns are net of all fees and expenses

Exhibit 15: Ambit’s Good & Clean Midcap Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of 31st Oct, 2022. Returns are net of all fees and expenses

Ambit Emerging Giants Portfolio

Small caps with secular growth, superior return ratios and no leverage –Ambit's Emerging Giants portfolio aims to invest in small-cap companies with market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than Rs4,000cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt) and ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence lead us to a concentrated portfolio of 15-16 emerging giants.

Exhibit 16: Ambit Emerging Giants Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of 31st Oct, 2022; All returns above 1 year are annualized. Returns are net of all fees and expenses

Exhibit 17: Ambit Emerging Giants Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of 31st Oct, 2022. Returns are net of all fees and expenses

Ambit TenX Portfolio

Ambit TenX Portfolio gives investors an opportunity to participate in the India growth story as the Indian GDP heads towards a US$10tn mark over the next 12-15 years. Mid and Small corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that can grow their earnings 10x over the same period implying 18-21% CAGR. Key features of this portfolio would be as follow:

- Longer-term approach with a concentrated portfolio: Ideal investment duration of >5 years with 15-20 stocks.

- Key driving factors: Low penetration, strong leadership, light balance sheet

- Forward-looking approach: Relying less on historical performance and more on future potential while not deviating away from the Good & Clean philosophy.

- No Key-man risk: Process is the Fund Manager

Exhibit 18: Ambit TenX Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of 31st Oct, 2022; Returns are net of all fees and expenses

Exhibit 19: Ambit TenX Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of 31stOct, 2022. Returns are net of all fees and expenses

For any queries, please contact:

Umang Shah- Phone: +91 22 6623 3281, Email - [email protected]

Ambit Investment Advisors Private Limited -

Ambit House, 449, Senapati Bapat Marg,

Lower Parel, Mumbai - 400 013

Risk Disclosure & Disclaimer

The performance of the Portfolio Manager has not been approved or recommended by SEBI nor SEBI certifies the accuracy or adequacy of the performance related information contained therein.

Ambit Investment Advisors Private Limited (“Ambit”), is a registered Portfolio Manager with Securities and Exchange Board of India vide registration number INP000005059.

This presentation / newsletter / report is strictly for information and illustrative purposes only and should not be considered to be an offer, or solicitation of an offer, to buy or sell any securities or to enter into any Portfolio Management agreements. This presentation / newsletter / report is prepared by Ambit strictly for the specified audience and is not intended for distribution to public and is not to be disseminated or circulated to any other party outside of the intended purpose. This presentation / newsletter / report may contain confidential or proprietary information and no part of this presentation / newsletter / report may be reproduced in any form without its prior written consent to Ambit. All opinions, figures, charts/graphs, estimates and data included in this presentation / newsletter / report is subject to change without notice. This document is not for public distribution and if you receive a copy of this presentation / newsletter / report and you are not the intended recipient, you should destroy this immediately. Any dissemination, copying or circulation of this communication in any form is strictly prohibited. This material should not be circulated in countries where restrictions exist on soliciting business from potential clients residing in such countries. Recipients of this material should inform themselves about and observe any such restrictions. Recipients shall be solely liable for any liability incurred by them in this regard and will indemnify Ambit for any liability it may incur in this respect.

Neither Ambit nor any of their respective affiliates or representatives make any express or implied representation or warranty as to the adequacy or accuracy of the statistical data or factual statement concerning India or its economy or make any representation as to the accuracy, completeness, reasonableness or sufficiency of any of the information contained in the presentation / newsletter / report herein, or in the case of projections, as to their attainability or the accuracy or completeness of the assumptions from which they are derived, and it is expected each prospective investor will pursue its own independent due diligence. In preparing this presentation / newsletter / report, Ambit has relied upon and assumed, without independent verification, the accuracy and completeness of information available from public sources. Accordingly, neither Ambit nor any of its affiliates, shareholders, directors, employees, agents or advisors shall be liable for any loss or damage (direct or indirect) suffered as a result of reliance upon any statements contained in, or any omission from this presentation / newsletter / report and any such liability is expressly disclaimed. Further, the information contained in this presentation / newsletter / report has not been verified by SEBI.

You are expected to take into consideration all the risk factors including financial conditions, risk-return profile, tax consequences, etc. You understand that the past performance or name of the portfolio or any similar product do not in any manner indicate surety of performance of such product or portfolio in future. You further understand that all such products are subject to various market risks, settlement risks, economical risks, political risks, business risks, and financial risks etc. and there is no assurance or guarantee that the objectives of any of the strategies of such product or portfolio will be achieved. You are expected to thoroughly go through the terms of the arrangements / agreements and understand in detail the risk-return profile of any security or product of Ambit or any other service provider before making any investment. You should also take professional / legal /tax advice before making any decision of investing or disinvesting. The investment relating to any products of Ambit may not be suited to all categories of investors. Ambit or Ambit associates may have financial or other business interests that may adversely affect the objectivity of the views contained in this presentation / newsletter / report.

Ambit does not guarantee the future performance or any level of performance relating to any products of Ambit or any other third party service provider. Investment in any product including mutual fund or in the product of third party service provider does not provide any assurance or guarantee that the objectives of the product are specifically achieved. Ambit shall not be liable for any losses that you may suffer on account of any investment or disinvestment decision based on the communication or information or recommendation received from Ambit on any product. Further Ambit shall not be liable for any loss which may have arisen by wrong or misleading instructions given by you whether orally or in writing. The name of the product does not in any manner indicate their prospects or return.

The product ‘Ambit Coffee Can Portfolio’ has been migrated from Ambit Capital Private Limited to Ambit Investments Advisors Private Limited. Hence some of the information in this presentation may belong to the period when this product was managed by Ambit Capital Private Limited.

You may contact your Relationship Manager for any queries.

The performance data for coffee can product between 6th march 2017 - 19th June 2017 represents model portfolio returns. First client was onboarded on 20th June 2017. The performance data for G&C product between 1st June 2016 to 1st April 2018 also includes returns for funds managed for an advisory offshore client. Returns are calculated using TWRR method as prescribed under revised SEBI (Portfolio Managers) Regulations, 2020