Remarkably, several companies that had struggled to make money in the last 10 years preceding FY22 —primarily due to weak fundamentals—turned out to be multi-baggers across sectors like Capital Goods, Power, Infrastructure, Iron & Steel, Realty, and Crude Oil. This rally was driven by renewed optimism regarding the government's commitment to capex following the COVID-19 pandemic. (27% CAGR over FY22 -24). However, in FY25, especially after the outcome of the Union elections on June 4th 2024, many of these stocks have reversed most of their gains as the focus now seems to be shifting from numbers vs narratives. Our investment philosophy does not permit us to invest just based on narratives and hence, post June until December, all our portfolios delivered superior returns relative to benchmarks. Whilst since Jan’25 markets have been in correction mode, led by severe correction across small and mid-caps, we believe the same will moderate once earnings growth starts improving from 1QFY26 onwards.Notably, our large, mid, and small cap continue to report superior earnings, which implies that as and when the market bounces back, our strategies should lead the bounce back on the pretext that the market continues to reward numbers over narratives.

Easy money was made during FY22 -24

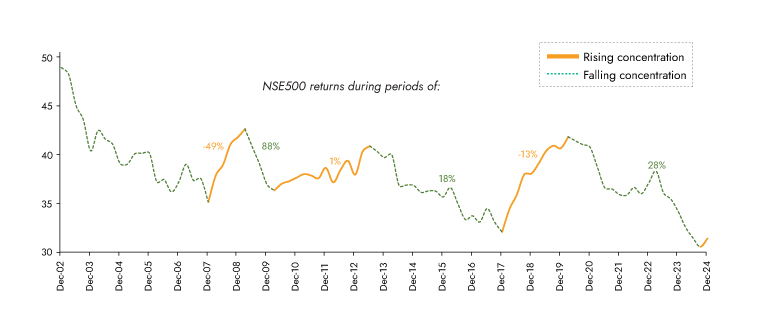

FY22 -24 was a notable aberration in the market landscape, characterized by strong performances from several companies. However, these gains were largely driven by thematic trends, occurring during a time when market concentration was on the decline. Typically, falling market concentration signals a broad-based rally, indicating a shift toward more inclusive growth across various sectors. Moreover, if we look at some of the top

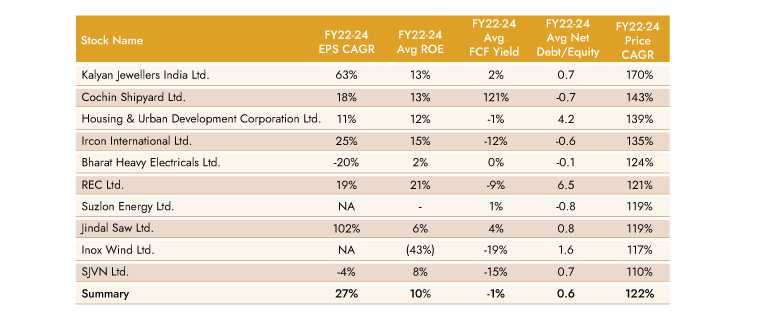

performers within BSE 500 over FY22 -24, we note mediocre return ratios and negative FCF yields; importantly, these names have not made much in the last 10 years prior to FY22 given mediocre EPS CAGR, ROE, FCF yield and leveraged balance sheet.

Exhibit 1: The FY22 -24 period saw a sharp fall in the market concentration of the NSE500 index

Source: Ambit Asset Management, Ambit Capital Research

Exhibit 2: Some of the top performers within BSE 500 had mediocre ROE, negative FCF yield and also leveraged balance sheet…

Source: Ambit Asset Management, Ace Equity

Exhibit 3:…and importantly, they have lost money in the last 10 years prior to FY22 given their weak fundamentals

1741339365266.jpg)

*For companies listed after FY12, returns have been taken as the yearly returns from the first financial year of listing until FY24

Source: Ambit Asset Management, Ace Equity

Government’s thrust on capex post-COVID ignited interest in several of the names highlighted above

With an intention to re-ignite animal spirits post-COVID-19 outbreak in FY20, the government announced aggressive capex spends. We note that central government capex outlay saw 24% CAGR during FY21 -25 vs. 7.3% CAGR over the last 4 years preceding this period. A host of sub-segments like Capital Goods, Power, Infrastructure, Iron & Steel, Realty, and Crude Oil saw investor interest in the hope that these sectors will see re-rating on fundamentals (more narrative at that point in time than numbers).

Exhibit 4: Central government capex saw 24% CAGR over FY21 to FY25…

Source: Ambit Asset Management, Avendus Spark

Exhibit 5: …led by Infra, Railways, Roads, Defense, Water and Housing

Source: Ambit Asset Management, Avendus Spark

Exhibit 6: Government capex as % of GDP exceeded 2.5% during FY21-24 vs <2 long term average

Source: Ambit Asset Management, Avendus Spark

Exhibit 7: Several of our top 100 performers within BSE 500 were from cyclical sectors like Power, Infra, Metals, Crude oil and Capital goods

Source: Ambit Asset Management, Avendus Spark

Exhibit 8: Notably, Capital goods, Power, Infra, Metals, Realty gave >40% CAGR during FY22 -24

1741325702333.jpg)

Source: Ambit Asset Management, Yahoo Finance

Post-Union elections up until Dec’24 market mood has changed towards more numbers over narratives

There is a noticeable change in the sector allocation post the results of the Union elections on 4th June 2024 until 31st December’24. Sectors with good return ratio, strong balance sheet and consistent earnings growth delivery started seeing more interest. Moreover, cyclical stocks which were more narrative based and which did well during FY22-24 saw significant draw-downs as BJP Government did not get enough seats to form Government by itself. The draw-downs were led by socialist behavior taking precedence over capex given several state elections at stake This change in sector allocation helped Ambit funds outperform broader markets given our style of fundamental investing.

Exhibit 9: 6 out of 10 BSE500 top-performing stocks during FY22 -24 showed negative performance post-elections till Dec 31 vs BSE 500 reporting positive performance ….

Source: Ambit Asset Management, Avendus Spark

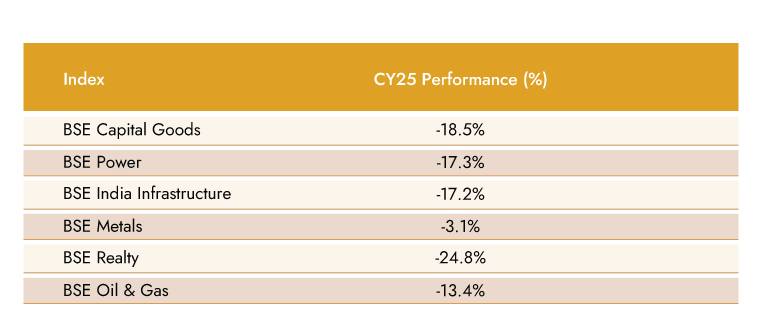

Exhibit 10: …likewise, key capex oriented sector indices also fell during this period…

1741325710188.jpg)

Source: Ambit Asset Management, Yahoo Finance

Exhibit 11: … which was complemented by relative outperformance of sectors that reported good numbers

Source: Ambit Asset Management, Yahoo Finance

Exhibit 12: Resultantly, Ambit portfolios started doing very well as companies continued to report superior performance

Source: Ambit Asset Management, Yahoo Finance

Market mayhem since January has been severely punishing both numbers as well as narratives (despite them having corrected since June’24)

Since Jan’25, there has been significant market correction led by a confluence of economic indicators, significant INR depreciation vs USD, subdued corporate earnings reports alongside earnings downgrades, and uncertainty with regard to trade tariffs and geopolitical developments. Nifty 50 index has retreated approximately 14% from its peak, underperforming global emerging market peers. Corporate profit growth for Nifty 50 companies stood at a modest 5% for the October- December quarter, marking the third consecutive quarter of single-digit expansion. Further, the Nifty Smallcap 250 and Nifty Midcap 150 indices have shed 22% and 15% from their peak respectively.

Exhibit 13: Previously strong narrative themes have been punished since Jan ’25…

Source: Ambit Asset Management, Yahoo Finance

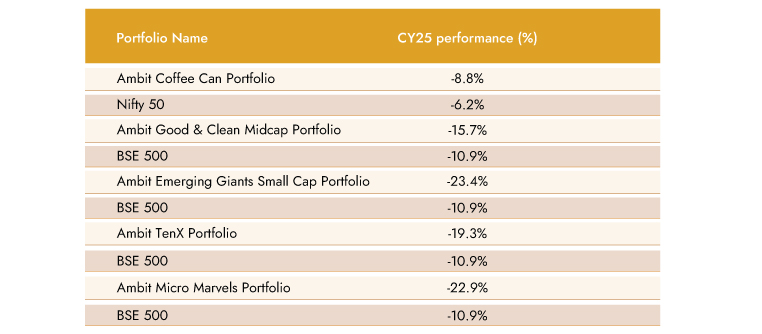

Exhibit 14:… as have fundamentally oriented Ambit AM portfolios

Source: Ambit Asset Management, Yahoo Finance

Exhibit 15: Earnings downgrades in Q3FY25 have been severe, inflating panic on the streets

1741325729666.jpg)

(Note: Large cap companies refer to the top 100 companies in BSE500 and SMID universe refers to 101 to 500 companies in BSE500)

Source: Ambit Asset Management, Bloomberg, Nuvama

FY26 should see earnings bounce back across caps; Ambit portfolios have strong earnings growth across schemes

FY26 we believe will see earnings growth recovering as compared to FY25 across all market cap buckets; Kotak Securities earnings estimates for Nifty 50/ BSE 500/BSE 250 Smallcap is 12.5%/14.6%/10.1% for FY25 and 14.3%/14.8%/25.3% for FY26. Hopefully this should act as a trigger for markets to bounce back. Secondly, if INR stabilizes against USD then it can act as a trigger for FIIs to make a re-entry given that the Shanghai index though relatively has done much better than India in the last 3 months has not made much absolute returns (up 1% since Jan’25) especially given the significant underperformance (down -6% over CY18-24 vs 127%/134% for Nifty/S&P 500).

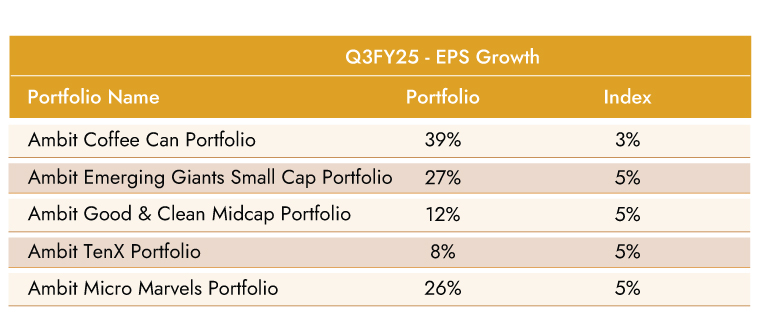

Ambit strategies continue to report strong earnings growth across portfolios in 3Q, as can be seen in the exhibit below. More importantly, our schemes have shown consistent fundamental performance across cycles, as seen from the exhibit below.

Exhibit 16: Strong Q3FY25 EPS growth witnessed across Ambit AM portfolios

Source: Ambit Asset Management

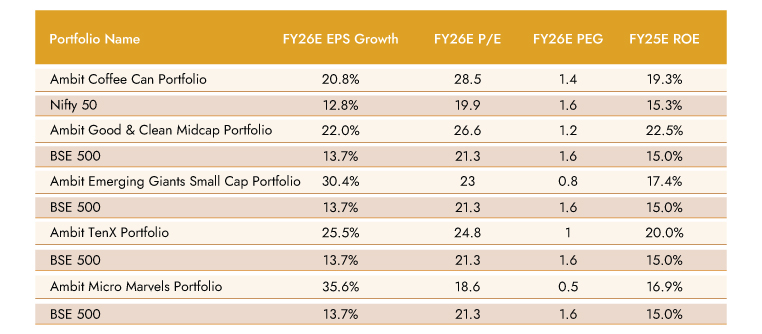

Whilst our schemes have also seen drawdowns YTD, we advise investors to use this as an opportunity to do top-ups, especially given that the earnings growth for all our schemes is likely to see strong growth in FY26 as well.

Exhibit 17: Strong fundamentals of Ambit funds will likely drive strong performance driven by fundamentals and sound valuations

Source: Ambit Asset Management

Whilst our portfolios have also seen drawdowns YTD, we advise investors can use this as an opportunity to do top-ups, especially given that the earnings growth for all our poerfolios is likely to see strong growth in FY26 as well.

AMBIT COFFEE CAN PORTFOLIO

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has an unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced with disruptions at regular intervals. As the industry evolves or is faced with disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

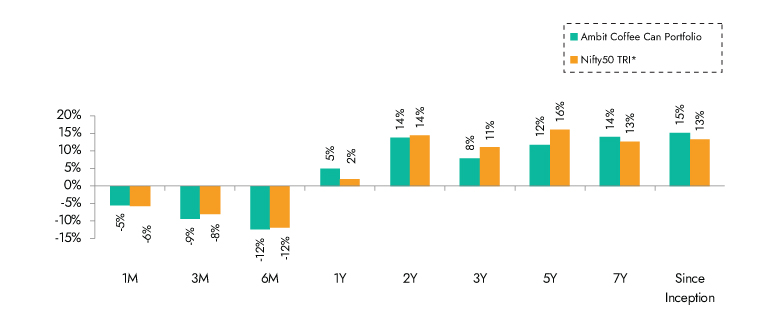

Exhibit 18: Ambit’s Coffee Can Portfolio point-to-point performance

Source: Ambit Coffee Can Portfolio inception date is Mar 06, 2017;**1M Return: 1st - 28th Feb'25; 3M Return: 1st Dec'24 – 28th Feb'25; 6M Return: 1st Sep'24 – 28th Feb'25; 1Y Return: 1st Mar'24 – 28th Feb'25

*Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The same is reported to SEBI.

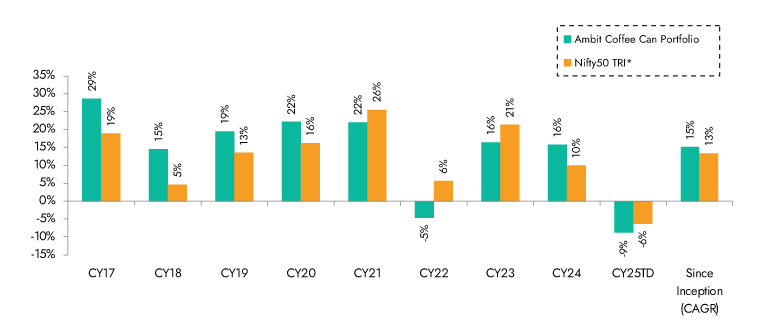

Exhibit 19: Ambit’s Coffee Can Portfolio calendar year performance

Ambit Coffee Can Portfolio inception date is Mar 06, 2017; *Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The same is reported to SEBI.

Ambit Good & Clean Midcap Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver superior risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

- Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

- Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longer with annual churn not exceeding 20-25% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with these compounding earnings acting as the primary driver of investment returns over long periods.

- Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

Exhibit 20: Ambit’s Good & Clean Midcap Portfolio point-to-point performance

Source: Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015;**1M Return: 1st - 28th Feb'25; 3M Return: 1st Dec'24 – 28th Feb'25; 6M Return: 1st Sep'24 – 28th Feb'25; 1Y Return: 1st Mar'24 – 28th Feb'25

*BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Mid cap. The same is reported to SEBI.

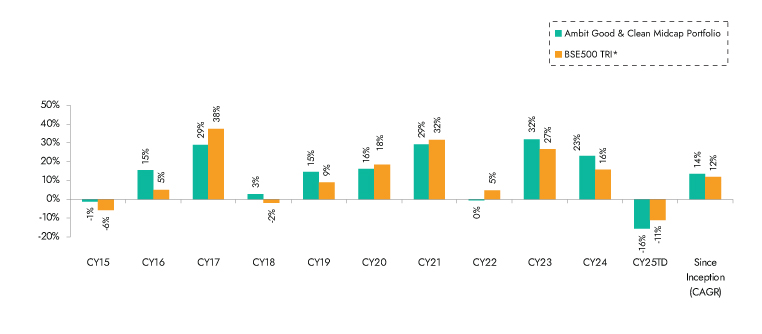

Exhibit 21: Ambit’s Good & Clean Midcap Portfolio calendar year performance

Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015; *BSE 500 50 TRI is the selected benchmark for the Ambit Good & Clean Mid cap. The same is reported to SEBI.

Ambit Emerging Giants Small Cap Portfolio

Small caps with secular growth, superior return ratios and no leverage are the essence of Ambit's Emerging Giants portfolio. The portfolio aims to invest in small-cap companies with market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than INR 10,000 cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt), and the ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence led us to a concentrated portfolio of 18-20 emerging giants.

Exhibit 22: Ambit Emerging Giants Portfolio point-to-point performance

Source: Ambit Emerging Giants Small cap Portfolio inception date is Dec 1, 2017;**1M Return: 1st - 28th Feb'25; 3M Return: 1st Dec'24 – 28th Feb'25; 6M Return: 1st Sep'24 – 28th Feb'25; 1Y Return: 1st Mar'24 – 28th Feb'25

*BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants Small cap. The same is reported to SEBI.

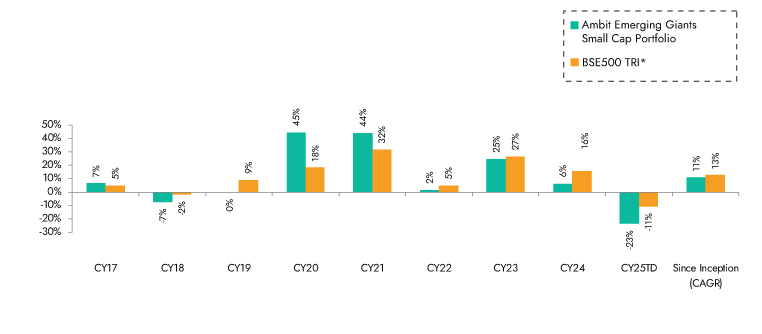

Exhibit 23: Ambit Emerging Giants Portfolio calendar year performance

Source: Ambit Emerging Giants Small cap Portfolio inception date is Dec 1, 2017; *BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants Small cap. The same is reported to SEBI.

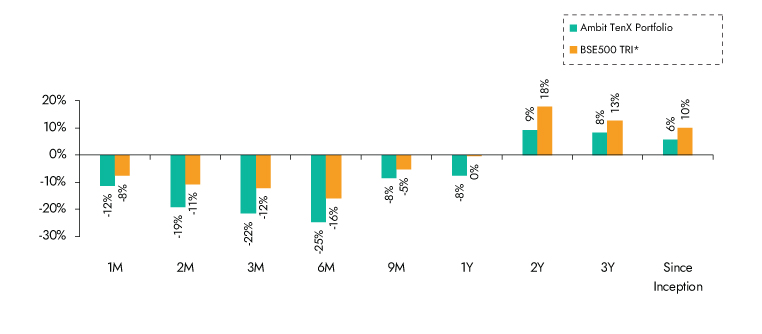

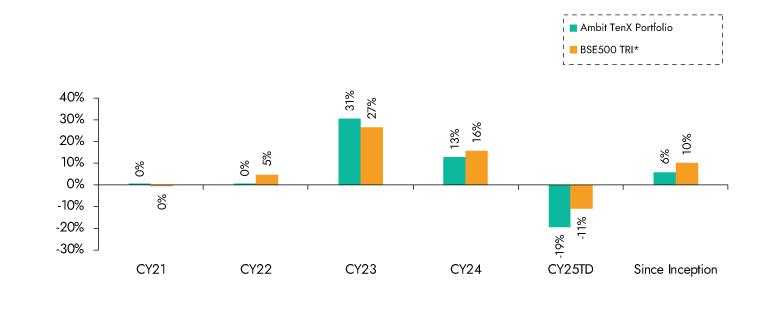

Ambit TenX Portfolio

Ambit TenX Portfolio allows investors to participate in the India growth story as the Indian GDP heads towards a US $10 tn mark over the next 12-15 years. Medium and smaller corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that can grow their earnings 10x over the same period implying 18-21% CAGR.

Key features of this portfolio would be as follows:

- Longer-term approach with a concentrated portfolio: Ideal investment duration of more than five years with 15-20 stocks.

- Key driving factors: Low penetration, strong leadership and light balance sheet

- Forward-looking approach: Relying less on historical performance and more on future potential while not deviating away from the Good & Clean philosophy.

Exhibit 24: Ambit TenX Portfolio point-to-point performance

Source: Ambit TenX Portfolio inception date is Dec 13, 2021;**1M Return: 1st - 28th Feb'25; 3M Return: 1st Dec'24 – 28th Feb'25; 6M Return: 1st Sep'24 – 28th Feb'25; 1Y Return: 1st Mar'24 – 28th Feb'25

*BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio. The same is reported to SEBI.

Exhibit 25: Ambit TenX Portfolio calendar year performance

Ambit TenX Portfolio inception date is Dec 13, 2021; *BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio. The same is reported to SEBI.

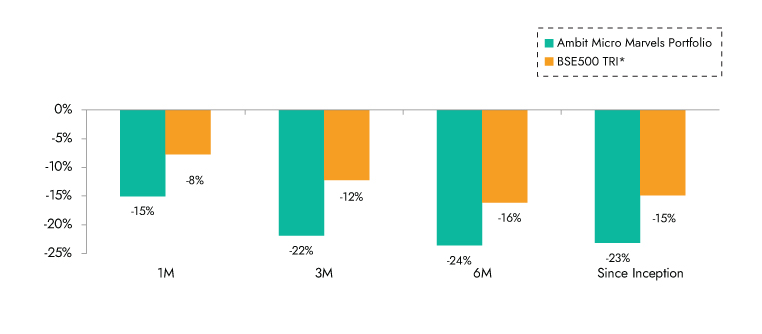

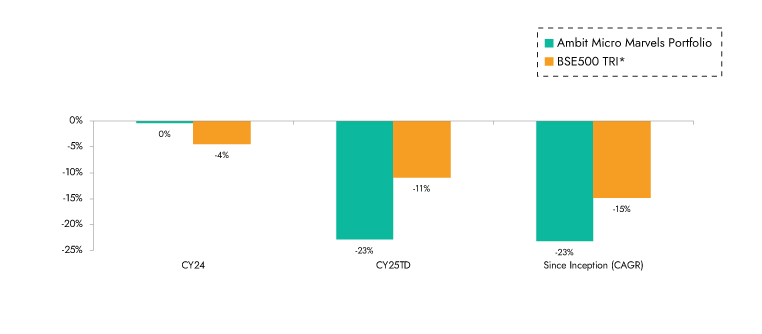

Ambit Micro Marvels Portfolio

We aim to create a portfolio that invests predominantly in micro-cap companies with the potential of delivering superior earnings growth and generating relatively better risk-adjusted performance over a long period of time.

Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts while our proprietary ‘greatness’ framework helps identify efficient capital allocators. The result is a concentrated portfolio of 20-25 stocks that draws down less than the market in corrections and has low churn.

Key Features of Portfolio Companies:

1. High earnings growth companies with low leverage,

2. Market leaders or challengers with strong moat around brand, distribution, technology, and innovation,

3. Strong corporate governance coupled with apt capital allocation.

Exhibit 26: Ambit Micro Marvels Portfolio point to point performance

Source: Ambit Micro Marvels Portfolio inception date is Jul 29, 2024;**1M Return: 1st - 31st Jan'25; 3M Return: 1st Nov'24 – 31st Jan'25; 6M Return: 1st Aug'24 – 31st Jan'25; 1Y Return: 1st Feb'24 – 31st Jan'25

*BSE 500 TRI is the selected benchmark for the Ambit Micro Marvels Portfolio. The same is reported to SEBI.

.

Exhibit 27: Ambit Micro Marvels Portfolio point to point performance

Source: Ambit Micro Marvels Portfolio inception date is Jul 29, 2024;

*BSE 500 TRI is the selected benchmark for the Ambit Micro Marvels Portfolio. The same is reported to SEBI.