We believe Indian markets today stand at one such inflection point. The reversal of market anomaly over FY21 to Sep '24 is now well in motion – leading to accentuated risks and creation of new opportunities. Howard Marks (HM) in his famous book "The Most Important Thing Illuminated" has covered investment risk most comprehensively across three chapters devoted to Understanding Risk, Recognizing Risk and Controlling Risk. In this newsletter, we cover a few key insights from HM's all-time classic book and what dangers and opportunities we see at Ambit Asset Management.

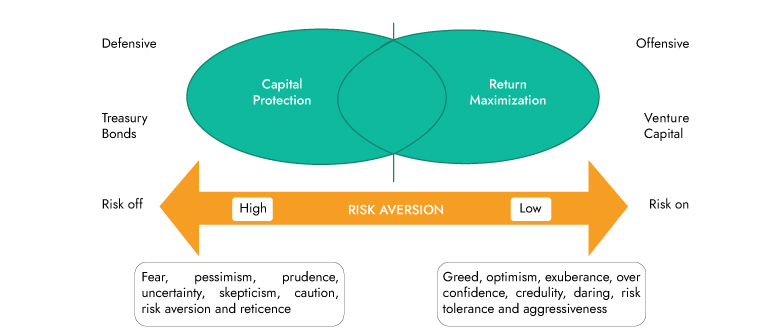

1) Investor Conundrum – Return Maximization or Capital Protection?

The key investor conundrum is balancing between return expectations and avoiding losses. As per HM, "An investor needs to ask themselves what they care about more, making money or avoiding losses?" Invariably the answer is both. The problem with this choice is that one cannot simultaneously go all out for profit making and loss avoidance. Investors must take a position regarding these two goals, which usually requires striking a reasonable balance between the two." What positioning an investor chooses in this risk tolerance spectrum depends on the investors goal. If one is aiming for Longevity (magic of compounding) leaning will be more towards defensiveness and conservativeness. Similarly, if aim is for rapid speed (glory like a shooting star) then leaning will be more towards high risk tolerance and aggressiveness. Historically, most of the accidents in the financial history has come from the second bucket.

The famous saying sums it up - "There are old investors, and there are bold investors, but there are no old bold investors." Hence, an investor needs to be both defensive and offensive.

Exhibit 1: Investing Conundrum

Source: Ambit Asset Management

Investing consists of precisely one thing: dealing with the future. And because we cannot know the future with certainty, risk is inescapable. In a bull market, it is not hard to find multiple winners. However, one is unlikely to succeed for long unless one has explicitly dealt with the risk aspect well. When you boil it all down, the investor must intelligently bear the risk for profit. Risk is the ultimate test of investment skill.

As per HM, the road to long-term investment success runs through risk control more than through aggressiveness. Over an entire career, most investors' results will be determined more by how many losers they have and how bad they are than the greatness of their winners. Skilful risk control is the mark of the superior investor. This is the reason Warren Buffett's dictum has been "Rule No. 1: Never lose money. Rule No. 2: Never forget Rule No. 1."

HM draws an analogy with sports for investing and suggests just like sports; investing also involves both offense and defense. Offense is easy to define. It is the adoption of aggressive tactics and elevated risk in the pursuit of above-average gains. But what is defense? Rather than doing the right thing, the defensive investors’ main emphasis is not doing the wrong thing. Is there a difference between doing the right thing and avoiding doing the wrong thing? On the surface, they sound alike. But when you look deeper, there is a big difference between the mindset needed for one and the mindset necessary for the other, and the difference is in the tactics to which the two lead.

After a long period of low volatility over FY21 to Sep ’24, volatility has shot up in recent months and likely to stay elevated. Our view is that the current investment environment will severely test investment strategies which do not have adequate balance and defensiveness. Equity flow showed the first signs of serious moderation in February 2025. We believe it is worthwhile to again reflect on the aspect of the 'risk-taking behaviour of various participants' that we had raised in our Ambit June’2024 newsletter and its likely impact on the market in the medium term.

The behaviour of different investors varies significantly. Institutional money will often have more conservativeness, HNI/ Ultra HNI will be more risk-taking, and retail will often have the highest risk-taking nature. In 2009, Alok Kumar, a professor focused on behavioural finance, explored who owns Junk stocks in a paper aptly titled "Who Gambles in the Stock Market?" He found that "at the aggregate level, individual investors prefer stocks with lottery features, and like lottery demand, the demand for lottery-type stocks increases during economic downturns." Retail investors prefer stocks with a high skewness of returns, greater unexplained volatility, and smaller companies with lower share prices.

During FY21-Sep'24, the marginal buyer was the retail investors. Their investment style preference is reflected in corresponding asset returns and predominant investment style during this period (momentum).

Assessing investment performance

Risk should be an essential consideration in assessing investment performance. Returns alone tell only part of the story about performance. Performance must be viewed in risk-adjusted terms. The riskiness of an investment does not become apparent until the investment is tested: "It's only when the tide goes out that we find out who's been swimming naked" – Warren Buffett.

The key questions are:

- How much risk did the manager bear to get his return?

- Was it fair-weather portfolio? Was it tested for red flags and sharp practices?

- How would it have held up if the environment had turned hostile?

Unless, an investor assesses investment performance across these key ponderables it will be difficult to understand the inherent risk. Risk is capable of being borne intelligently.

You can bear risk prudently and profitably if it is:

- Risk you are aware of

- Risk that can be analyzed

- Risk that can be diversified Risk you are well paid to bear

Skilled investors assemble portfolios that will produce good returns if things go well and resist decline if things go poorly. This asymmetry is the critical element – of superior investing. Assembling a portfolio that incorporates risk control and the potential for gains is a great accomplishment. But it is a hidden accomplishment most of the time since risk only turns into loss occasionally . . . when the tide goes out.

2) What is Risk?

Peter Bernstein defines risk as: "Because of the existence of risk, things will be different from what we expect from time to time. How well are we prepared to deal when it is different?"

HM broadly divides risk into these three groups:

1) Risk is the probability of losing money (Absolute) This is what most people mean when they say "risk." This is what people demand compensation for if they are to bear it

2) Risk is the probability of missing out (Relative) Opportunities forgone represent a serious performance shortcoming. Thus, the risk of missing opportunities is another important risk.

3) Risk is the likelihood of being forced out at the bottom (Behavioral) Many investors claim to be long-term oriented and thus immune to fluctuations. But bad enough declines can make them sell ‒ because they lose confidence, ‒ because they receive margin calls or ‒ because they need to fund real-world cash requirements. Some of the greatest pain in 2008 was felt by investors who had overestimated their ability to withstand volatility. Selling at the bottom - turning a downward fluctuation into a permanent loss and missing out on the subsequent rebound – is the cardinal sin in investing.

Some of the other common risks are:

I. Falling short of one's Goal

Investors have different needs, and failure to meet those needs poses a risk for each investor. A pensioner may need steady returns to meet his bills, while a young executive may be OK with volatile but high returns to reach a medium-term financial goal. Hence, a given alpha-focused investment strategy may be a high risk for one and an acceptable risk for the other.

II. Underperformance

A manager could try eliminating that benchmark risk by moving closer to the index. In the other extreme, in crazy (high beta rallies) times, a manager can only keep ahead of the market by doing even crazier things (market periods like FY1999-01; FY03-07 or FY21-1HFY25). History shows that in crazy times, disciplined investors willingly accept the risk of not taking risks to keep up example, Warren Buffett/ Julian Robertson in 1999.

III. Career Risk

This is extreme underperformance risk: the risk that arises when the people who manage money and the people whose money it is are different. In such cases, a manager with little incentive on the upside may not care much for gains, but could be afraid of losses that could cost him his job. The implication – risk that could jeopardize return to an agent's firing point is rarely worth taking.

IV. Unconventionality

Risk of being different. Stewards of other people's money can be more comfortable turning in average performance, regardless of where it stands in absolute terms than with the possibility that unconventional actions will prove unsuccessful and get them fired. Concern over this risk keeps many from superior results.

V. Illiquidity

If an investor needs money for urgency in three months or a year, an investment which cannot be counted on for liquidity that meets the schedule. Thus, for this investor, the risk is not losing money, volatility, or any of the above. It is a personal risk of being unable to turn an investment into cash at a reasonable price.

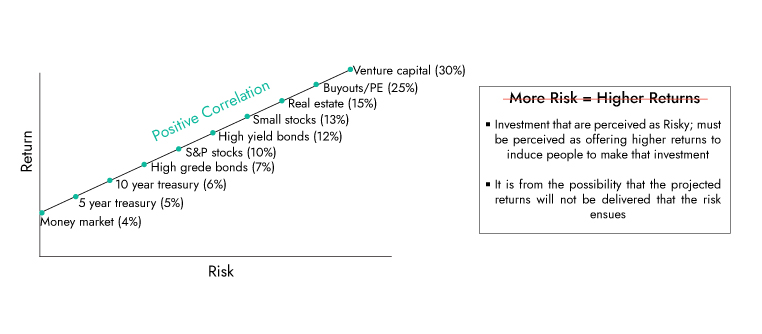

3) Most investors assume a linear relationship between Risk and Returns

Market participants believe that there is a linear relationship between risk and return. They believe "riskier assets produce higher returns" or "the way to make more money is to take more risk." These are traps into which most investors fall, especially in times when things are going well and risk-taking is being rewarded. If risky investments could be counted on to produce high returns, they would not be risky. Instead, it makes sense that investments that seem riskier must appear to offer higher returns to attract capital. But they do not actually deliver. Recently, we have witnessed a proliferation of the same in the form of i) Investing in obscure IPOs, SMEs etc. and ii) Investing in unlisted new age stocks

Exhibit 2: Most investors assume a linear relationship between Risk and Returns

Source: The Most Important Thing Illuminated – Howard Marks; Ambit Asset Management

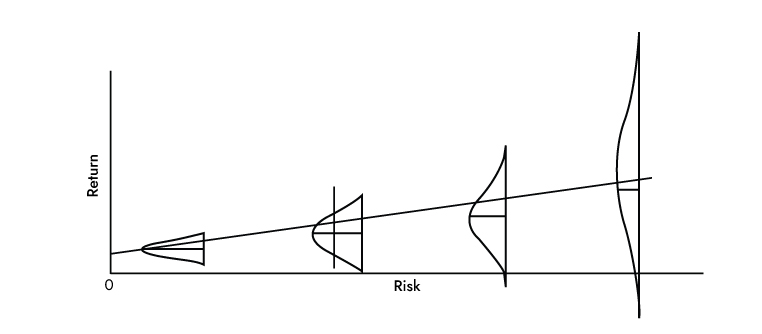

As risk increases ‒ the expected return rises ‒ the range of possible outcomes becomes wider, and ‒ the worst outcome worsens and ultimately becomes negative. This is the right way to think about the risk/return relationship. "Essentially risk says we do not know what is going to happen. We walk every moment into the unknown. There is a range of outcomes, and we do not know where [the actual outcome is] going to fall within the range. Often, we do not know what the range is."– Peter Bernstein

Exhibit 3: As risk increases, the range of outcomes becomes wider

Source: The Most Important Thing Illuminated – Howard Marks; Ambit Asset Management

4) Risks show up in a lumpy manner

Investors generally overestimate their ability to gauge risk and understand mechanisms they have never seen in operation. Even if it contains construction flaws, a house will stand until an earthquake happens. Equally, an investment can be risky and still not show losses as long as the environment remains salutary. The fact that an investment is susceptible to a serious risk that will occur only infrequently – the "improbable disaster" or "black swan" – can make it appear safer than it is.

Amos Tversky summarized this best "It's frightening to think that you might not know something, but more frightening to know that, by and large, the world is run by people who have faith that they know exactly what's going on." Imprudent investors who overlook human limitations act in a manner that ensures outcomes are knowable and controllable; they underestimate the risk present in the things they are doing.

Investors who view the future as knowable act more offensively when investing, while investors who acknowledge the future as unknowable will invariably invest more defensively to accommodate the black swan risks. Overestimating what one can know or do can be extremely dangerous – in brain surgery, trans-ocean racing or investing. Acknowledging the boundaries of what one can learn and working within those limits rather than venturing beyond can give a great advantage. During bull markets, the kind we have witnessed during FY21-Sep'24, such overconfidence was at its peak. However, no matter how good the fundamentals maybe, humans exercising their greed and propensity to err can screw things up. "For a bullish phase…to hold sway. The environment must be characterized by greed, optimism, exuberance, confidence, credulity, daring, risk tolerance and aggressiveness. But these traits will not govern a market forever. Eventually, they will give way to fear, pessimism, prudence, uncertainty, skepticism, caution, risk aversion and reticence. Busts are the products of booms, and I am convinced it usually more correct to attribute a bust to the excesses of the preceding boom than to the specific event that sets off the correction."

– Howard Marks One of Taleb's most memorable parables in his book Antifragile goes like this. Suppose you are a turkey whose job is to create projections for future quality of life for your flock based on historical data. Every day since you started your record, you and the other turkeys are well-fed and given ample room to wander at leisure. As time passes, you become increasingly confident in your projections that tomorrow will be similarly favourable, the next day, and the day after that. But what you and the other turkeys do not know is that Thanksgiving is right around the corner. In a nutshell, Taleb's story illustrates the "black swan" predicament — those unexpected events that happen when we rely on using past events to predict the future. As Taleb notes, "Just because you never died before doesn't make you immortal,"

Exhibit 4: Taleb's parable of Turkey Problem

Source: The Black Swan – Nassim Taleb, Ambit Asset Management

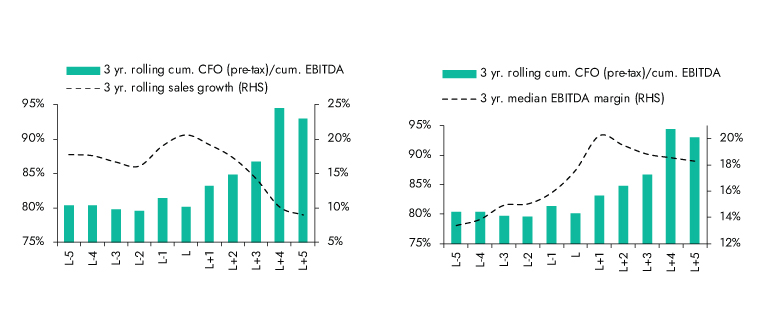

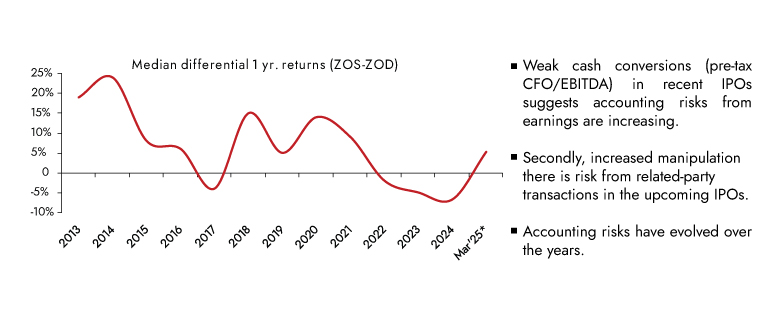

This construct is important to remember, as historically in all past bull rallies, as the rally subsidies, cockroaches start tumbling out from predictable pockets such as companies falling in Zone of Darkness (ZOD), low quality illiquid SMID segment and poor-quality recent IPO’s etc. Ambit Capital Research, have highlighted that weak cash conversions (pre-tax CFO/EBITDA) in recent IPOs suggests accounting risks from earnings manipulation are increasing. Secondly, there is increased risk from related-party transactions in the upcoming IPOs.

Exhibit 5: Bull markets are known for thier excesses in IPOs

Source: Company, Ambit Capital Research; universe is all companies (ex. BFSI) which have come out with an IPO since CY13; L represent the year of listing whereas L-1 represents one year before listing, L-2 represents two years before listing and so on, Ambit Asset Management

Source: Company, Ambit Capital Research; universe is all companies (ex. BFSI) which have come out with an IPO since CY13; L represents the year of listing whereas L-1 represents one year before listing, L-2 represents two years before listing and so on, Ambit Asset Management

What we can learn from past Crisis:

The most dangerous investment condition generally stems from psychology that is too positive. For this reason, fundamentals do not have to deteriorate for losses to occur; a downgrading of investor opinion will suffice. High prices often collapse of their own weight. – Howard Marks

1. Too much capital availability makes money flow to wrong places

2. When capital goes where it should not, bad things happen

3. When capital is in oversupply, investors compete for deals by accepting low returns and a slender margin of error

4. Widespread disregard for Risk creates great Risk

5. Inadequate due diligence leads to investment losses

6. In heady times, capital is devoted to innovative investments, many of which fail the test of time

7. Hidden fault lines running through portfolios can make the prices of seemingly unrelated assets move in tandem

8. Psychological and technical factors can swamp fundamentals

9. Markets change, invalidating models

10. Leverage magnifies outcomes but does not add value

11. Excesses self-correct

Ambit Asset Management philosophy

- Ambit AMC focuses on capital protection – our first attempt is to understand the downside risk and then the upside. We are willing to forego potential returns in poor governance stocks and deep cyclical and fad stocks to limit our downside risk.

- We stay away from the venture capital style of investing.

- Avoiding leverage plays.

- We believe selling at the bottom – turning a downward fluctuation into a permanent loss and missing out on the subsequent rebound – is the cardinal sin in investing. While constructing the ACCP portfolio, we believe in being suitably defensive as we need to be prepared for a 'Black Swan Event' at all times as such events cannot be predicted; hence, one needs to be always prepared to deal with the same.

- We also do not take speculative market cash calls, based on macro or short-term market views - with the investor money.

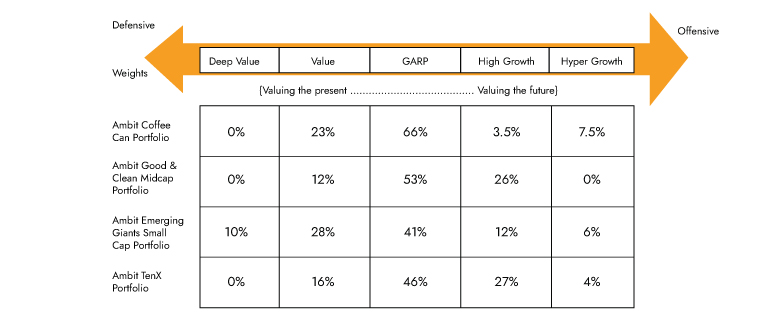

Exhibit 6: Valuation spectrum - Defensive vs Offensive

Source: lan Casle – Valuation Spectrum / Ambit Asset Management

Key risks we see in the market

We continue to see three key risks: 1) Valuations in the broader markets, except for large-cap, remain expensive (mainly SMIDs); 2) Weak companies drove recent rally FY21-Sep'2; and 3) Liquidity risk remains very high and still not much appreciated.

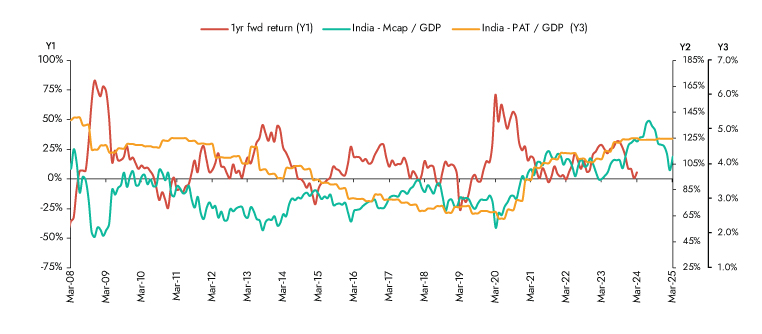

Exhibit 7: Valuations in the broader markets continue to remain expensive

Source: Ambit Capital Research, Bloomberg; Note: Universe is BSE500; PAT data is updated for December quarter for companies that have reported financials; GDP data is updated up to Dect’24 qtr. Latest data as of 23rd March’25, Ambit Asset Management

The recent rally FY21-Sep'2 was a Risk-on and High-beta rally

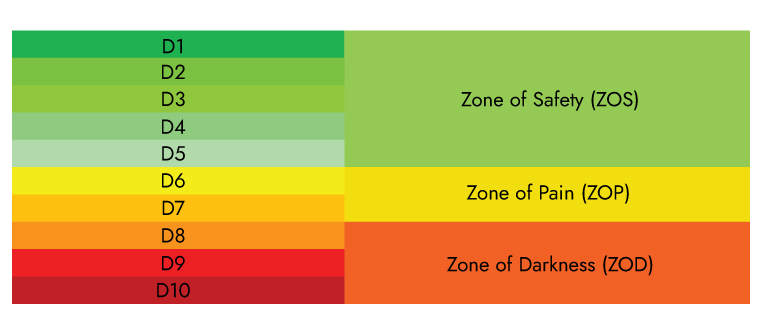

Ambit Capital Research has a proprietary forensic model, wherein they have 11 equally weighted accounting ratios where they do relative ranking for companies on each of them and basis the final score, and then divide the companies into deciles such that first five deciles (D1 to D5) are called 'Zone of Safety (best accounting quality companies), next two deciles (D6 and D7) are called 'Zone of Pain' (relatively weak accounting quality companies) and last three deciles (D8-D10) are called "Zone of Darkness" (worst accounting quality companies). They use 11 quantifiable ratios across four categories of accounting checks duly adjusted for 'RECENCY' and 'MATERIALITY'.

Exhibit 8: Decile ratings based on accounting quality

Source: Ambit Capital Research, Ambit Asset Management

The exhibit below is differential returns calculated on a one-year forward basis; for instance, differential return in 2013 signifies the difference in median 1yr return of companies featured in the Zone of Safety and the Zone of Darkness in FY12. Returns are computed from 01 Jan to 31st Dec. The study highlights how the rally in CY22/CY23 was driven by companies in the 'Zone of Darkness', implying a risk on and a high beta rally.

Exhibit 9: During CY22-23 market was driven by companies in Zone of Darkness (ZOD)

Source: Company, Ambit Capital research, universe is BSE500 (ex. BFSI); differential returns are calculated on a 1 yr. forward basis, for instance, differential return in 2013 signifies difference in median 1 yr. return of companies which featured in Zone of Safety and Zone of Darkness in FY12; Returns are computed from 01 Jan to 31st Dec. *Returns are computed from 01 Oct 24 to 13 Mar 25 and than annualized

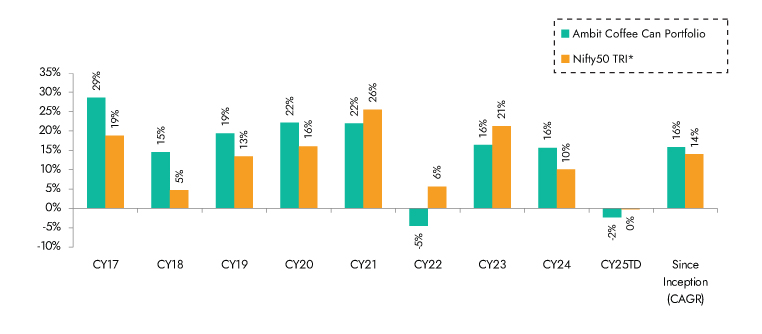

Ambit Coffee Can Portfolio performance in CY22/CY23 was negatively impacted as it remained true to label and abstained from participation in the high beta and risk on sectors falling in the 'Zone of Darkness'

Exhibit10 :Ambit Coffee Can Poerfolio's performance was impacted over CY22-23 as it abstained from such plays

Source: Ambit Coffee Can Portfolio inception date is Mar 06, 2017; *Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The same is reported to SEBI

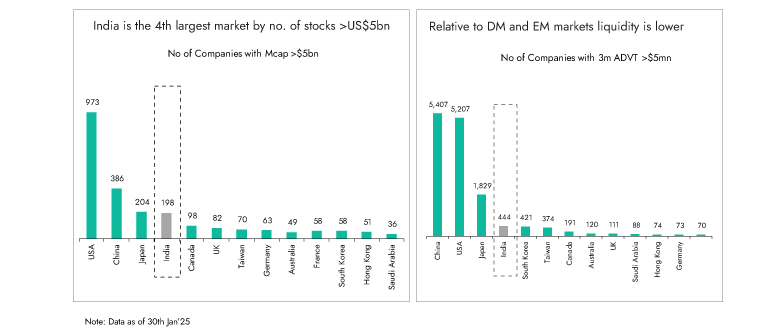

2) Liquidity is the key risk

Exhibit 11: India is the 4th largest market by no. of stocks >US$5bn Relative to DM and EM markets liquidity is lower

Source: : Bloomberg, Ambit Capital Research, Ambit Asset Management

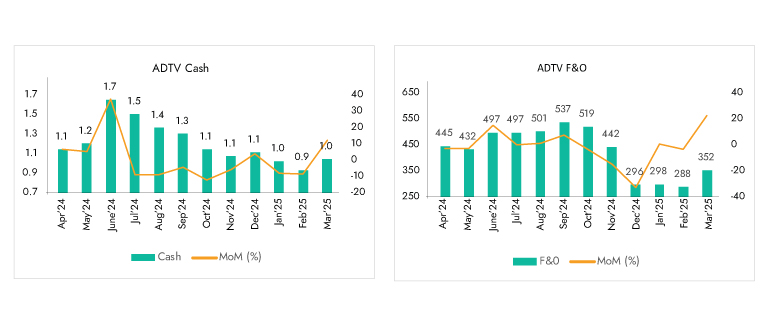

Exhibit 12: Trading Volumes across Cash and F&O under pressure

Source: NSE, BSE, Ambit Asset Management

Exhibit 13: Higher demand than supply has exerted pressure on Availability Factor (AF)

Source: Ambit Capital research, Ace Equity, Note: Analysis includes Top 500 companies by market capitalization every quarter! This Availability Factor analysis is based on stock-level classification by AMFI, Ambit Asset Management

Exhibit 14: Retail investor Flows can be unpredictable in the face of declining returns

Source: Bloomberg, Ace Equity, Ambit Capital Research, Ambit Asset Management

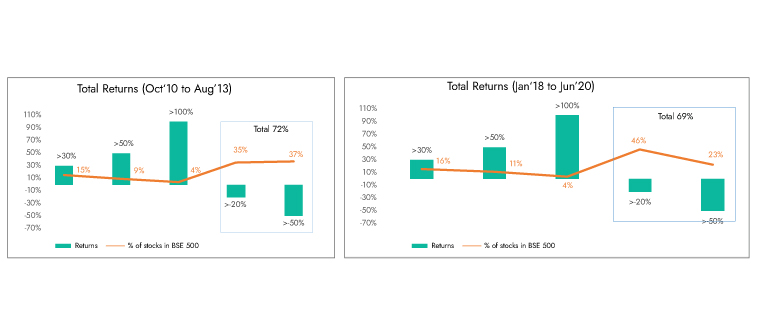

Exhibit 15 During the last two Polarization cycles (FY10-13 and FY19-21) almost ~84% NSE 500 stocks gave less than double digit returns per annum

Source:Bloomberg, Ambit Asset Management

Key opportunities

1) Increasing polarization – presents opportunities in large caps

- Market anomaly during FY21-Sep'24, has created opportunities in the large-cap segment (particularly the BFSI vertical).

- Ambit Capital Research's proprietary model "Ambit Stock Market Concentration Index" is a quantitative measure of stock concentration. It is constructed like the HHI Index and gives a complete picture.

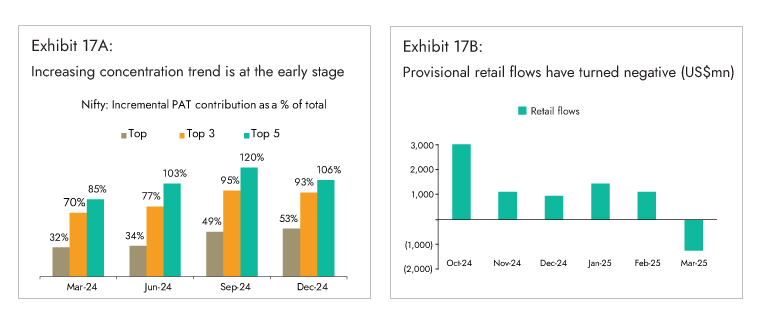

- Since the start of concentration in Sept-24, Nifty (-14%) corrected less than mid-caps (-20%) and small-caps (-25%). This is in line with empirical evidence, which suggests that mid-caps and small-caps underperform Nifty and vice-versa in periods of rising concentration.

Exhibit 16: Increasing concentration trend is at the early stage

Note: Latest data as on 24th Jan' 25

Source: Bloomberg, Ambit Capital Research, Ambit Asset Management

- Heavyweights are expected to lead smaller companies in Nifty in FY25/26 over top-line and bottom-line. Secondly, a select few companies drive incremental profits, especially in large-caps.

- Historically, large-cap EPS has been resilient compared to small and mid-caps.

Exhibit 17A: Increasing concentration trend is at the early stage

Source: Bloomberg, Ambit Capital Research, Ambit Asset Management Source: NSE, Bloomberg, Kotak Institutional Equity, Ambit Asset Management

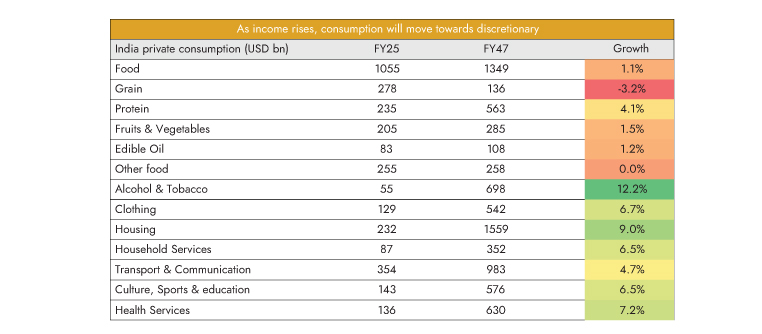

2) India provides structural long-term opportunities across several sectors

Indian market is unique in the sense it provides secular long-term bottom-up investing opportunities across several attractive and high growth sectors. Ambit AMC holdings are clustered around key sectors likely to witness structural long-term growth over the next few decades, driven by increasing per capita disposable income. The key sectors are BFSI, Discretionary Consumption, Pharma and Technology.

Exhibit 18: Secular opportunities across key sectors

Source: CEIC, MoSPI, Bloomberg, NHS, Ambit Capital research. We assume per capita GDP growth of 7.5% and Private consumption to maintain its ~60% share in GDP Ambit Asset management

Summary:

- HM broadly divides key risks into three groups: i) Risk is the probability of losing money (Absolute); ii) Risk is the probability of missing out (Relative); iii) Risk is the likelihood of being forced out at the bottom (Behavioral)

- As per HM, the road to long-term investment success runs through risk control more than through aggressiveness. Over an entire career, most investors' results will be determined more by how many losers they have and how bad they are than the greatness of their winners.

- Investing inherently involves dealing with an uncertain future, making risk an unavoidable factor and a key test of investment skill.

- What positioning an investor chooses in this risk tolerance spectrum depends on the investor’s goal. If one is aiming for Longevity (magic of compounding) leaning will be more towards defensiveness and conservativeness. Similarly, if aim is for rapid speed (glory like a shooting star) leaning will be more towards high risk tolerance and aggressiveness. Historically, most of the accidents in the financial history has come from the second bucket.

- We believe Indian markets today stand at an inflection point. The reversal of market anomaly over FY21 to Sep '24, is now well in motion – leading to an increase in risk and creation of new opportunities.

- Low liquidity, High-valuation and Concentrated low free float holdings, is the space from where black swan challenges could emerge.

- Past two market cycles show that in polarized environments, earnings predictability is rewarded, and excessive diversification may become a drawback. During the last two such polarization cycles, spanning FY11-13 and FY18-21, ~85% of NSE 500 stocks registered less than double digit returns per annum.

- Increasing polarization provides opportunities for large-caps, particularly in the BFSI vertical. India also offers structural bottom-up opportunities across several attractive sectors with longevity and growth.

- Ambit Asset Management portfolios are clustered around these opportunities. Ambit Asset Management prioritizes capital protection by first assessing downside risks and avoiding investments in poorly governed, cyclical, or trend-driven stocks.

AMBIT COFFEE CAN PORTFOLIO

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has an unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced with disruptions at regular intervals. As the industry evolves or is faced with disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

Exhibit 19: Ambit’s Coffee Can Portfolio point-to-point performance

Source:Ambit Coffee Can Portfolio inception date is Mar 06, 2017**1M Return: 1st - 31st Mar'25; 3M Return: 1st Jan'25 – 31st Mar'25; 6M Return: 1st Oct'24 – 31st Mar'25; 1Y Return: 1st Apr'24 – 31st Mar'25 *Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The same is reported to SEBI

Exhibit 20: Ambit’s Coffee Can Portfolio calendar year performance

Ambit Coffee Can Portfolio inception date is Mar 06, 2017; *Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio. The same is reported to SEBI.

Ambit Good & Clean Midcap Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver superior risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

- Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

- Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longer with annual churn not exceeding 20-25% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with these compounding earnings acting as the primary driver of investment returns over long periods.

- Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

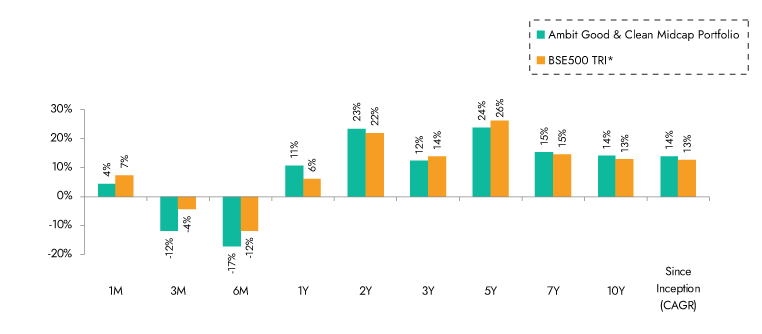

Exhibit 21: Ambit’s Good & Clean Midcap Portfolio point-to-point performance

Source: Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015**1M Return: 1st - 31st Mar'25; 3M Return: 1st Jan'25 – 31st Mar'25; 6M Return: 1st Oct'24 – 31st Mar'25; 1Y Return: 1st Apr'24 – 31st Mar'25 *BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Mid cap. The same is reported to SEBI.

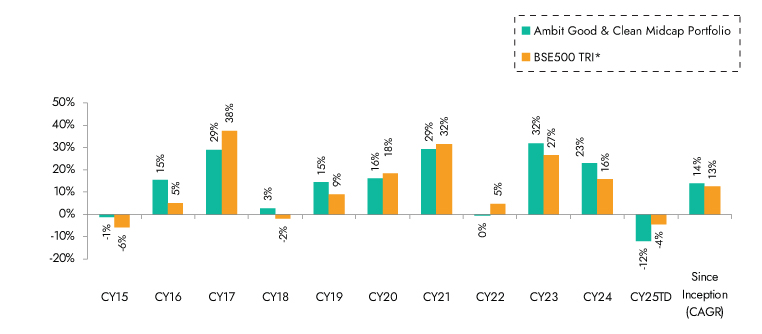

Exhibit 22: Ambit’s Good & Clean Midcap Portfolio calendar year performance

Ambit Good & Clean Mid cap Portfolio inception date is Mar 12, 2015; *BSE 500 50 TRI is the selected benchmark for the Ambit Good & Clean Mid cap. The same is reported to SEBI.

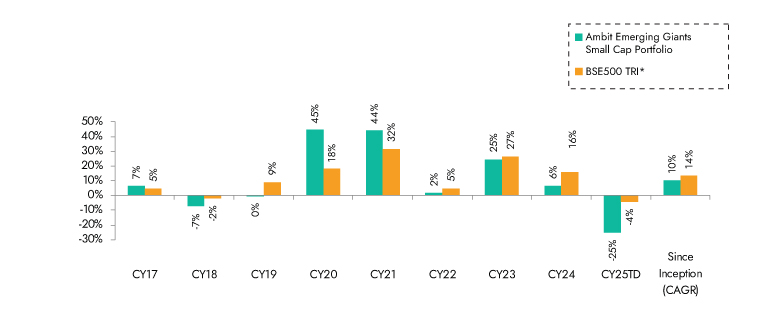

Ambit Emerging Giants Small Cap Portfolio

Small caps with secular growth, superior return ratios and no leverage are the essence of Ambit's Emerging Giants portfolio. The portfolio aims to invest in small-cap companies with market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than INR 10,000 cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt), and the ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence led us to a concentrated portfolio of 18-20 emerging giants.

Exhibit 23: Ambit Emerging Giants Portfolio point-to-point performance

Sorce: Ambit Emerging Giants Small cap Portfolio inception date is Dec 1, 2017;**1M Return: 1st - 31st Mar'25; 3M Return: 1st Jan'25 – 31st Mar'25; 6M Return: 1st Oct'24 – 31st Mar'25; 1Y Return: 1st Apr'24 – 31st Mar'25 *BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants Small cap. The same is reported to SEBI

Exhibit 24: Ambit Emerging Giants Portfolio calendar year performance

Source: Ambit Emerging Giants Small cap Portfolio inception date is Dec 1, 2017; *BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants Small cap. The same is reported to SEBI.

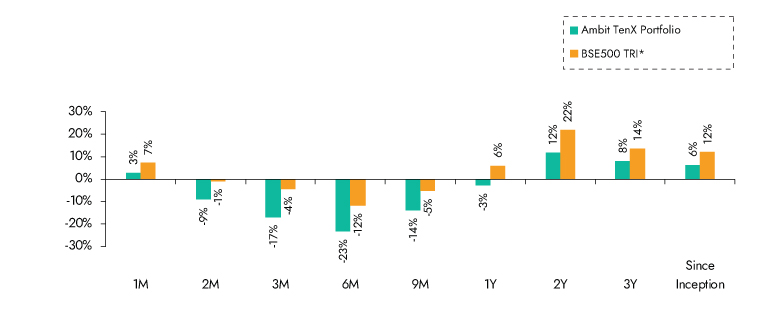

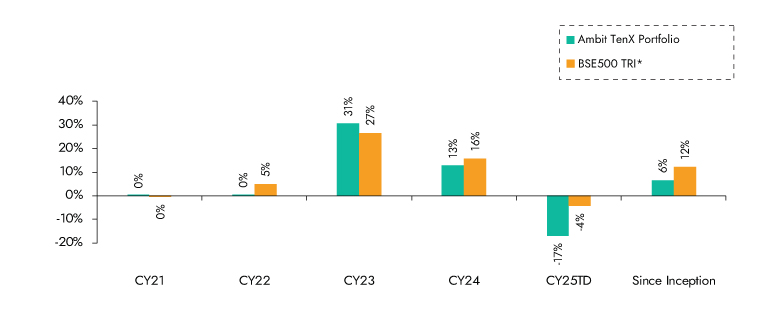

Ambit TenX Portfolio

Ambit TenX Portfolio allows investors to participate in the India growth story as the Indian GDP heads towards a US $10 tn mark over the next 12-15 years. Medium and smaller corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that can grow their earnings 10x over the same period implying 18-21% CAGR.

Key features of this portfolio would be as follows:

- Longer-term approach with a concentrated portfolio: Ideal investment duration of more than five years with 15-20 stocks.

- Key driving factors: Low penetration, strong leadership and light balance sheet

- Forward-looking approach: Relying less on historical performance and more on future potential while not deviating away from the Good & Clean philosophy.

Exhibit 25: Ambit TenX Portfolio point-to-point performance

Source:**1M Return: 1st - 31st Mar'25; 3M Return: 1st Jan'25 – 31st Mar'25; 6M Return: 1st Oct'24 – 31st Mar'25; 1Y Return: 1st Apr'24 – 31st Mar'25 *BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio. The same is reported to SEBI

Exhibit 26: Ambit TenX Portfolio calendar year performance

Source:Ambit TenX Portfolio inception date is Dec 13, 2021; *BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio. The same is reported to SEBI.

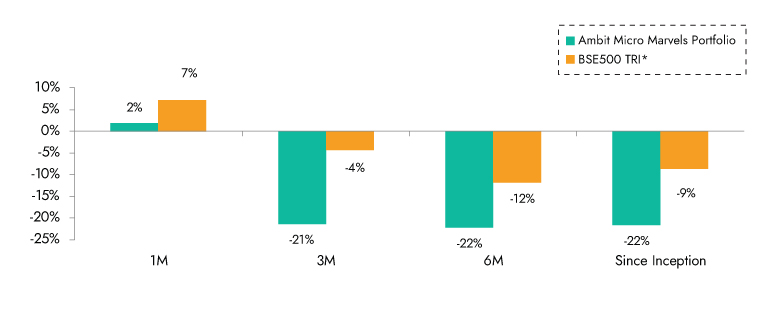

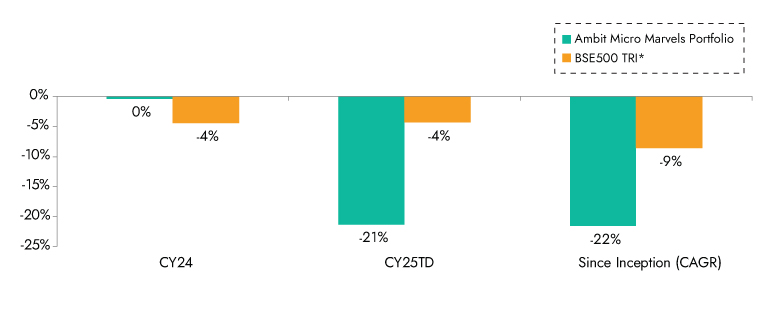

Ambit Micro Marvels Portfolio

We aim to create a portfolio that invests predominantly in micro-cap companies with the potential of delivering superior earnings growth and generating relatively better risk-adjusted performance over a long period of time.

Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts while our proprietary ‘greatness’ framework helps identify efficient capital allocators. The result is a concentrated portfolio of 20-25 stocks that draws down less than the market in corrections and has low churn.

Key Features of Portfolio Companies:

1. High earnings growth companies with low leverage,

2. Market leaders or challengers with strong moat around brand, distribution, technology, and innovation,

3. Strong corporate governance coupled with apt capital allocation.

Exhibit 27: Ambit Micro Marvels Portfolio point to point performance

Source: Ambit Micro Marvels Portfolio inception date is Jul 29, 2024;**1M Return: 1st - 31st Mar'25; 3M Return: 1st Jan'25 – 31st Mar'25; 6M Return: 1st Oct'24 – 31st Mar'25; 1Y Return: 1st Apr'24 – 31st Mar'25 *BSE 500 TRI is the selected benchmark for the Ambit Micro Marvels Portfolio. The same is reported to SEBI.

Exhibit 28: Ambit Micro Marvels Portfolio point to point performance

Source: Ambit Micro Marvels Portfolio inception date is Jul 29, 2024;

*BSE 500 TRI is the selected benchmark for the Ambit Micro Marvels Portfolio. The same is reported to SEBI.